Simon Property Group (SPG)

Let's get fancy.

In the same vein as what I have been discussing—bubbles popping and buying REITs—I want to introduce you to Simon Property Group (SPG) as something to put on your watchlist in the event of the spectacular demise of the overall stock market. SPG isn’t just any shopping center REIT; it is perhaps the premier shopping center REIT to own, with a truly impressive portfolio of properties. SPG deviates sharply from the lifestyle tenancy and town center business model I praised with SITC. Instead, SPG focuses on providing a luxury experience to its patrons as a means of combating eCommerce.

Perhaps a more user friendly list: Property List

Page 31-36 property list, some notable properties include:

King of Prussia Mall

South Coast Plaza

The Galleria

Sawgrass Mills

Aventura Mall

The Forum Shops at Caesars

The Shops at Crystals

Northgate Station

As usual, I use Google Maps to get a view of these properties, including inside the enclosed shopping malls.

Page 26 top tenants, here are a few notable ones:

LVMH

Tapestry

Nordstorm

Macy’s

Capri Holdings

Signet Jewelers

Again, this is a very different strategy from the town center or lifestyle tenancy approach. Once upon a time, the general consensus was that inline enclosed shopping malls were dead and gone. I always thought that was an overreaction, and that has largely been proven correct. The main priority for any shopping center is to fight back against online shopping. A shopping center can do this by filling itself with businesses that can’t be replicated online: hair salons, video game arcades, restaurants, tutoring centers, medical clinics, etc. My local mall even has a wrestling academy and a location for the public library. This embodies the town center strategy.

SPG is a completely different beast. They offer luxury. Need to buy a Rolex or a Gucci bag? That’s what you’ll find in an SPG shopping center. Even their outlet malls are geared toward luxury, featuring premium brands like Nike and Coach. SPG is the only REIT I know of that offers its own rewards American Express card.

https://www.cardless.com/cards/simon

SPG even allows you to shop their outlet malls online, making luxury shopping more accessible to everyone. While this may seem counter to encouraging in-person visits, it directly benefits SPG’s tenants and serves as its own strategy to combat the dominance of Amazon and other online retailers.

(While writing this, I found a great deal on a pair of Adidas shoes.)

This is just not your typical REIT.

Nothing about SPG is cheap or unattractive. This is, quite frankly, an excellent strategy to compete with online retailers. Yes, people can and do purchase luxury items online, which is why SPG maintains its own online presence. However, when someone plans to spend $10,000 or more on a high-end watch or $1,000 or more on a luxury handbag, they are often drawn into the store to ensure the item fits and looks perfect before making such a significant purchase. That is the key to a thriving shopping center in 2025: enticing people to visit in person.

If I have one regret in investing, it is not buying SPG stock at the bottom of the COVID stock market crash. SPG boasts a unique collection of properties and a solid business strategy. As of this writing, SPG is trading at a PE of 23, which is more than I am willing to pay for a REIT. For this reason, SPG remains on my watchlist. If there is ever another stock market crash, I would seize the opportunity to scoop up this stock.

Now, let’s dive into some of the charts:

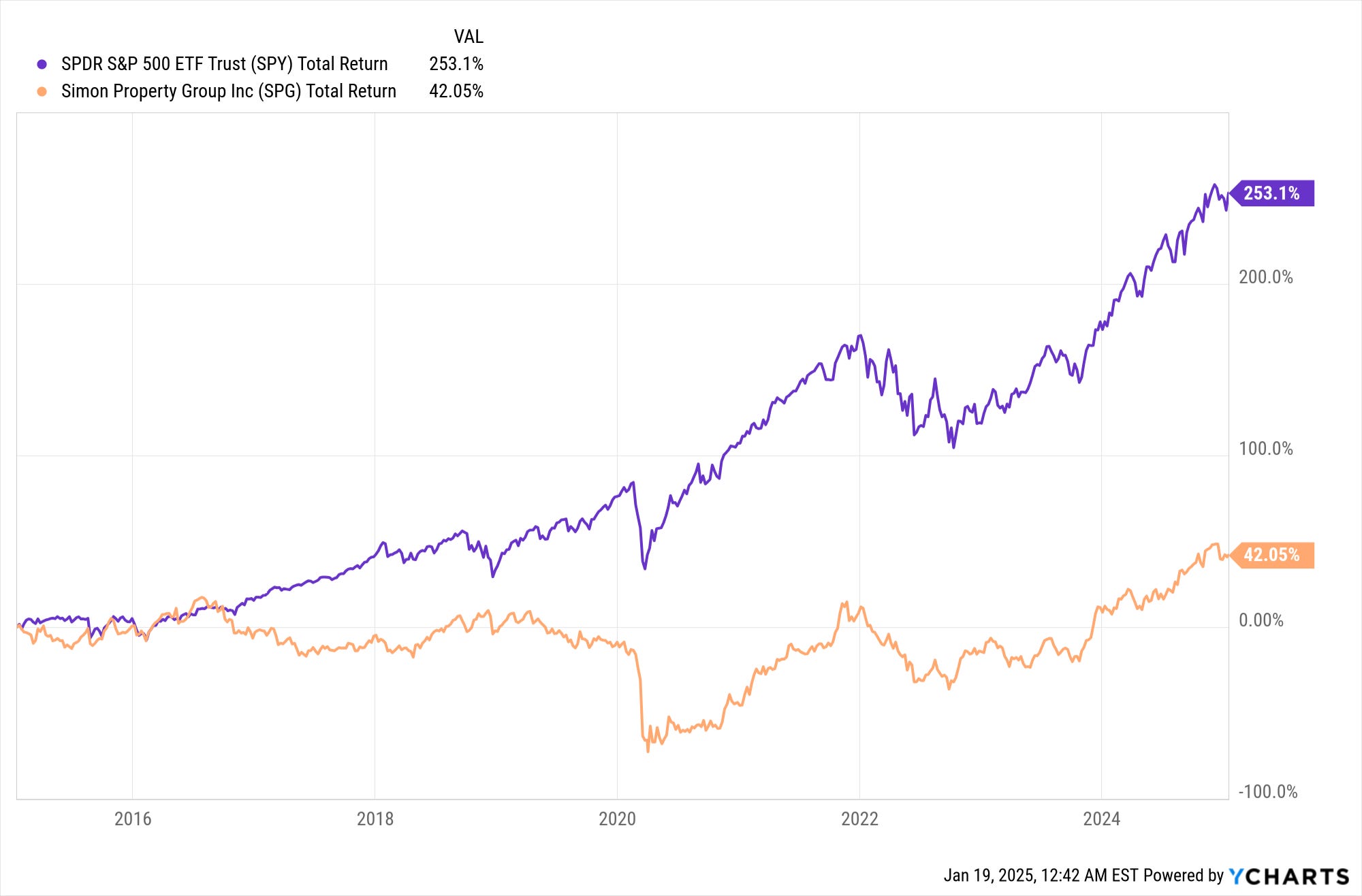

SPG vs. S&P 500 as far back as I have data:

SPG vs. S&P 500 over the last ten years:

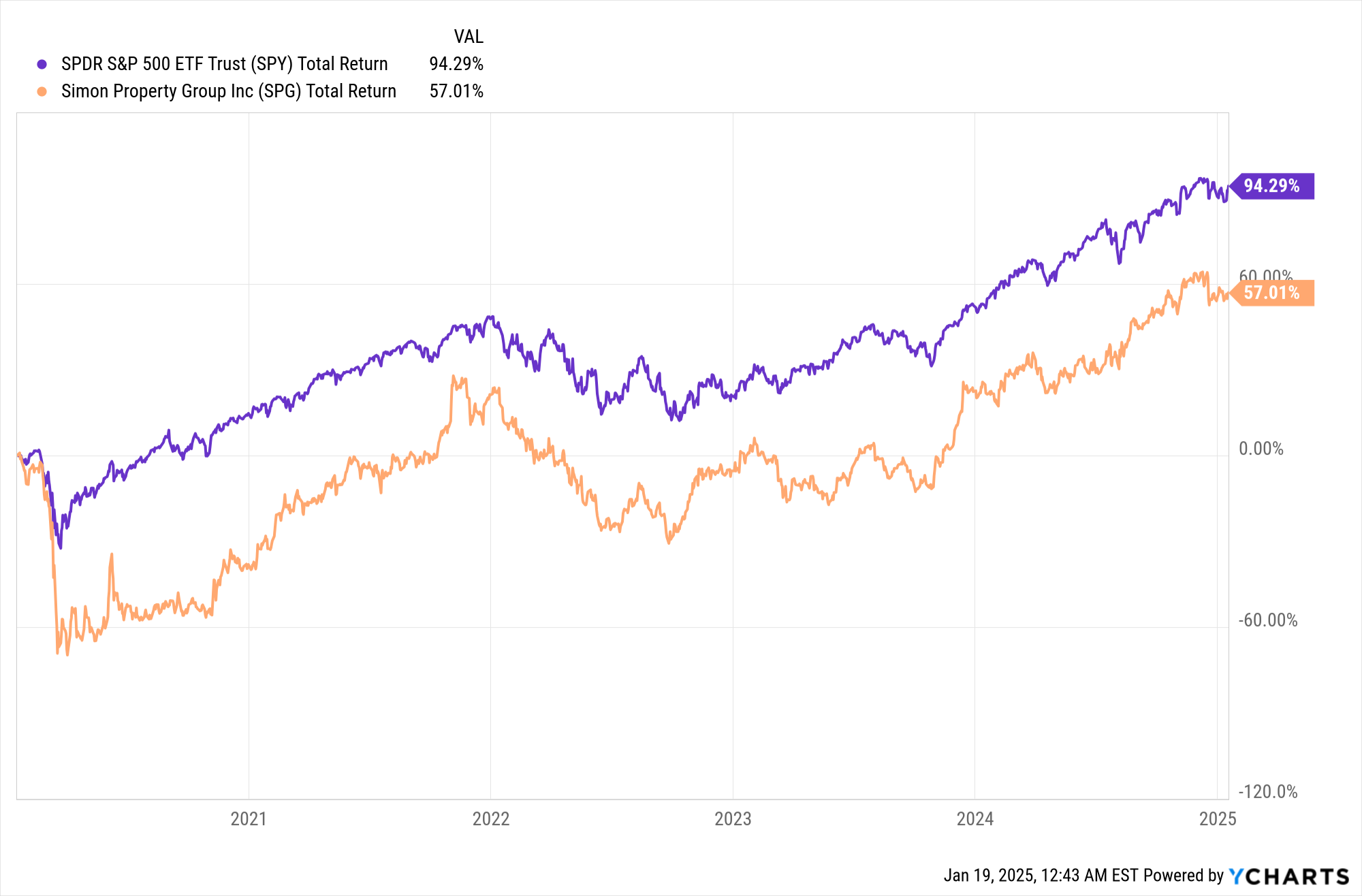

SPG vs. S&P 500 over the last five years:

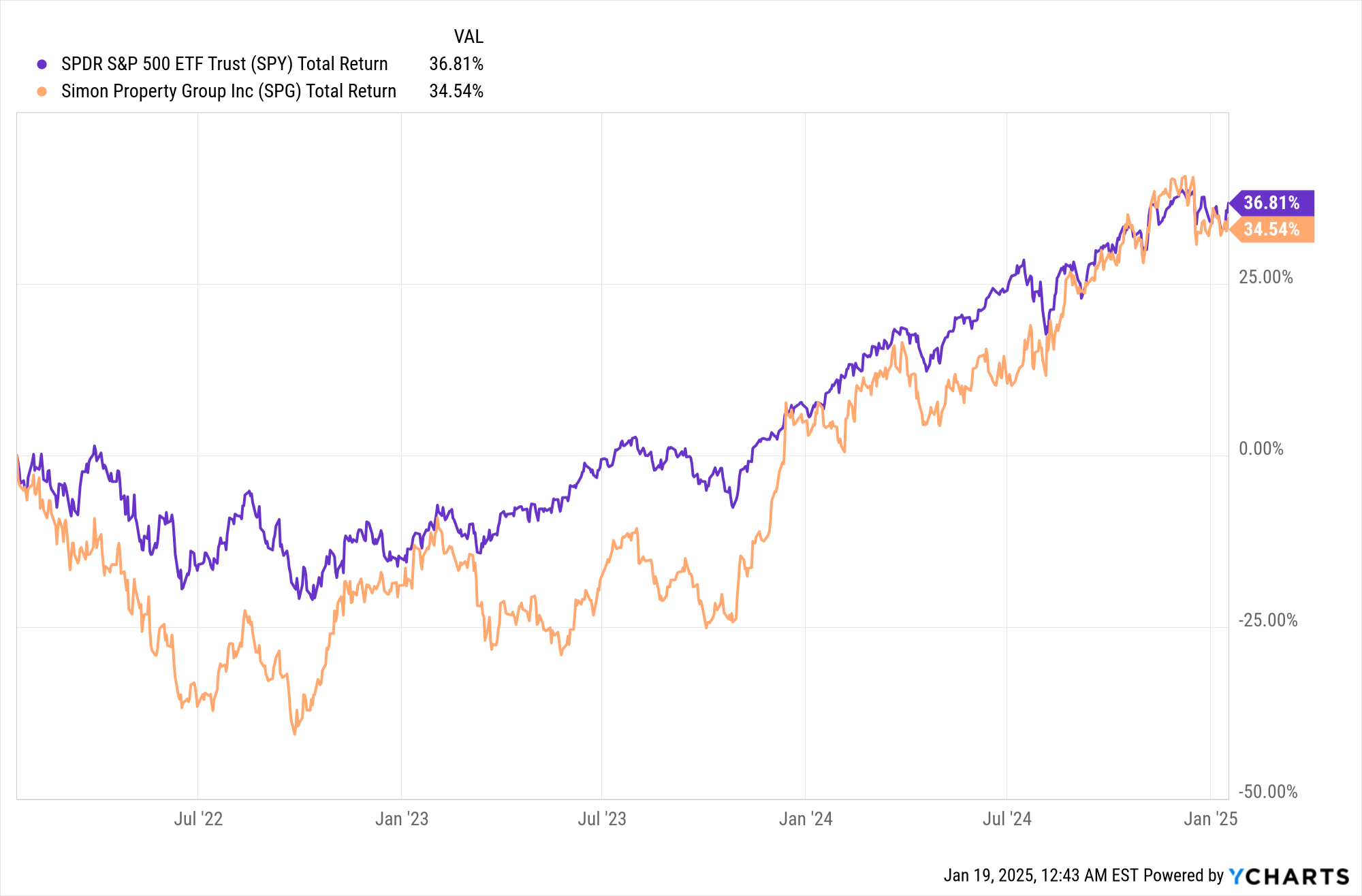

SPG vs. S&P 500 over the last three years:

SPG vs. S&P 500 over the last year:

SPG vs. S&P 500 from the bottom of the COVID crash:

As you can see, timing your investment plays a significant role in SPG's performance as an investment. Since I use total return and not just share price, the graphs account for the dividends investors have received.

I’m holding off on a deep dive into the 2023 10-K since the 2024 10-K will be released in early February. If I see a buying opportunity for SPG in the future, I’ll conduct a more thorough review of all their finances. Thankfully, YCharts conveniently scrapes data from all of SPG’s annual and quarterly statements, organizing the information year-over-year in a spreadsheet like format for me. At a surface glance, nothing seems abnormal. Cash and Short-Term Investments combined with Total Receivables roughly equal Payables and Accrued Expenses, which is reassuring. A business should always have the means to cover its short-term obligations.

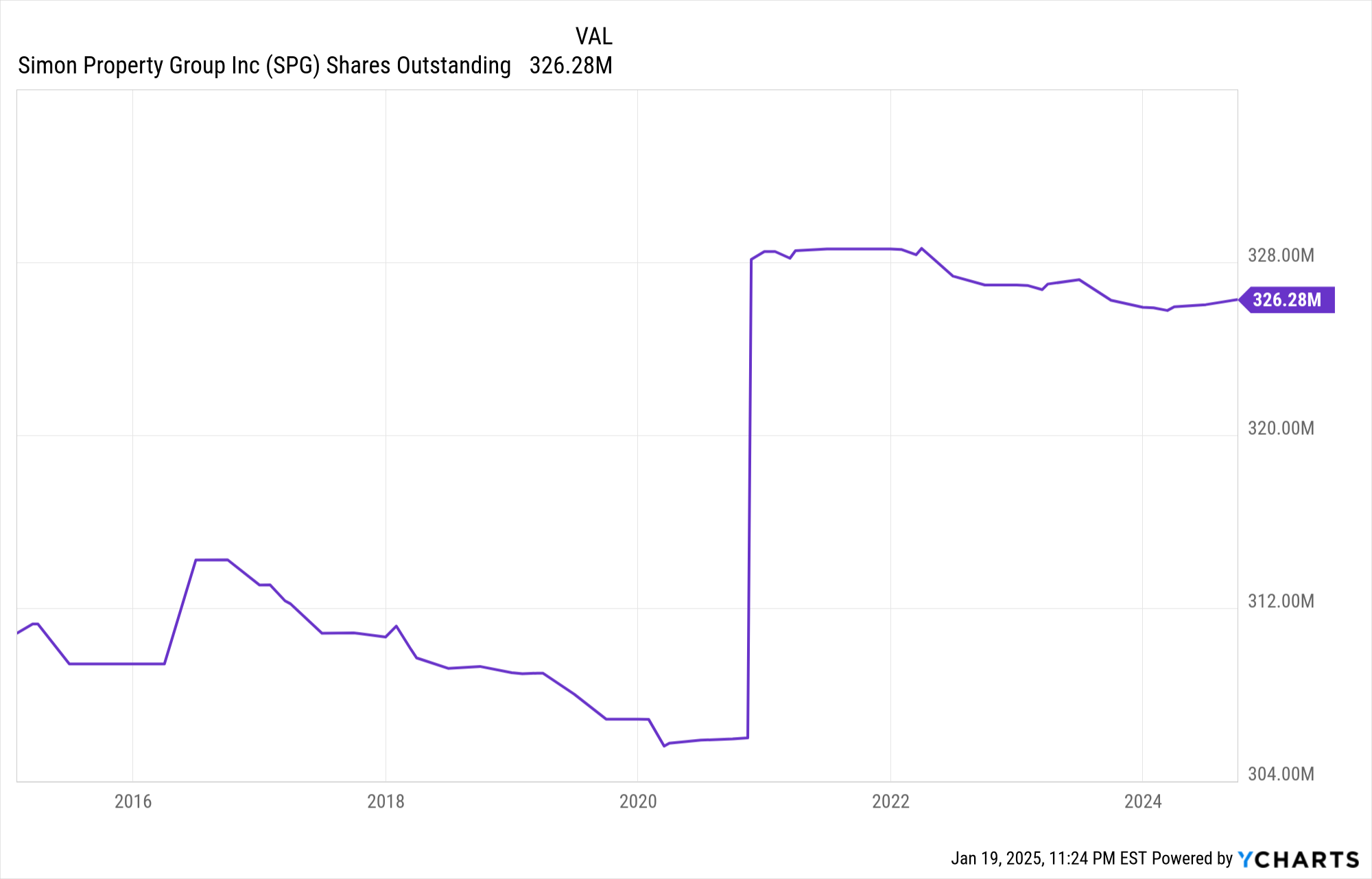

One detail that caught my attention is that in 2020, SPG issued $1.5 billion in new stock, followed by $338 million of new stock in 2021. They also took on $2.28 billion in new debt in 2020. At face value, this isn’t behavior I typically like to see from a corporation. However, in 2020, every shopping center in the United States was forcibly closed by the government. As you can imagine, this was a severe blow to a shopping center based REIT. These measures were necessary for SPG to hoard cash and survive. I can’t fault them for that; desperate times call for desperate measures. SPG’s revenue dropped by about 25% compared to the previous year in 2020. This is why investing in financially sound companies is crucial—so they have the flexibility to adapt when disaster strikes. It’s worth noting that SPG has since done right by shareholders, buying back some of the shares they issued.

Let’s take a look at some visual aids:

You’ll notice the drop isn’t very drastic, which is because SPG is a REIT. REITs are required by law to pay out 90% of their taxable income as dividends to shareholders. This limits a REIT’s ability to buy back its stock. However, we can see that SPG has engaged in stock buybacks in the past and continues to do so. This is behavior I appreciate from corporate management.

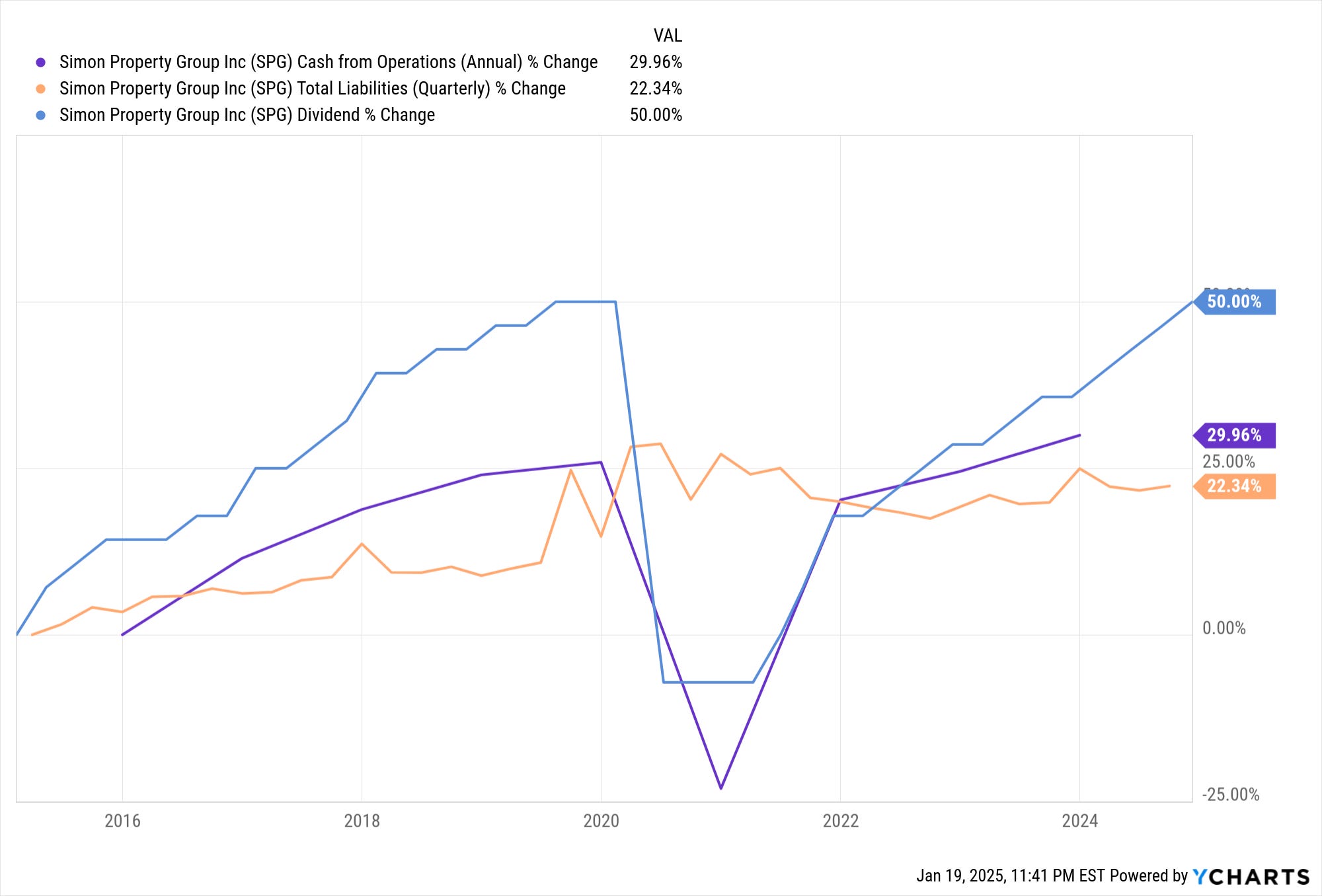

Debt is a different story with REITs. Generally, it always goes up and never down. This is because the more the REIT grows, the more mortgages they take on as they acquire more properties. Two things are more important to focus on: first, is cash flow increasing in tandem with the debt? Second, does this increase in debt mean the dividend is rising? If both of these factors are present, the debt is being used effectively.

That graph is a little chaotic to look at, but the most important part is that the debt is the lowest of the three lines. Cash flow is increasing faster than debt, which shows SPG has the ability to continue paying the mortgages on their properties. The top line represents the increase in the dividend, which has vastly outpaced the increase in debt. While SPG continues to grow in size and take on debt, it is paying off for shareholders and is being managed intelligently.

Overall, Simon Property Group (SPG) is an amazing business. It is always one that I have my eye on. This is why I think buying the S&P 500 index is for suckers. When bubbles pop, one would logically think only the extremely overvalued stocks would be affected. Not so. There is a huge amount of money in broad-based index funds and mutual funds. In a market decline, if these investors want to sell, they have to sell everything. Meanwhile, I happily stand on the other side of the transaction, buying the gems that are mixed in with all the panic selling. That is why I keep an eye on Simon Property Group (SPG).

My Portfolio:

FI, ADP, MCD, AFL, AXR, VLO, SITC, SHV

METC $17 Call 6/20/2025

FedEx Bond CUSIP: 313309AP1

JP Morgan Chase Bond CUSIP: 48130CVM4

*Disclaimer*

You can and will lose money in the stock market. You can lose all of your money. I can and will be wrong. I have been wrong in the past. I have lost money in the past. Investing in stocks is risky and should never be considered safe. Invest at your own risk.