Shell (SHEL)

They talk about climate change a lot for an energy company.

First, I have to say I love the amount of detailed information that Shell gives to its shareholders. They really drill down and give quality information on each segment. That being said, Shell sometimes comes off as self-hating with its fixation on reducing carbon emissions. It’s like a dairy farm trying to reduce its reliance on cows. It just doesn’t make a lot of sense. Reduction should only be the goal of the consumer, if at all, not the producer, who only serves to meet consumer demand.

I’m going to do this one out of order and cover Hamilton Helmer’s Seven Powers first. I think it is important to keep them in mind while digging into a business as vast as Shell.

Hamilton Helmer’s Seven Powers:

Scale Economies

For Shell, I don’t see a scale economy where size lowers cost. A gallon of gasoline is about the same price everywhere. It’s not like one gas station in the same area sells at $8 a gallon and another one sells at $2 a gallon. In terms of costs to the business, I don’t think size lowers costs; I think it increases them, which, in this case, is good, but that comes later. In short, I do not see a scale economy.

Network Economies

I don’t see a network economy present. A higher number of customers doesn’t increase the quality of Shell’s product in a direct manner.

Counter-Positioning

Counter-positioning usually refers to a business using a method that incumbents can’t match. That isn’t Shell.

Switching Costs

Nope, energy products are all basically interchangeable.

Branding

I believe branding is present for Shell. As you will see later on, Shell has a global presence. If a foreign government is looking for a company to develop its oil fields, having a strong reputation as a performer makes a difference. I also believe brand matters a bit to the retail consumer. You may notice unbranded gas stations that sell gasoline at a lower price. The reason they can do this is that they sell fuel that is worse for your engine and only meets the legal minimum standards set by the EPA, whereas the larger energy companies, like Shell, sell Top Tier gasoline with extra detergents that help keep your car running longer.

Cornered Resource

Cornered resource is a big maybe, in my opinion. Shell has a cornered resource in that it owns rights to oil and gas reserves worldwide. But it doesn’t have a cornered resource in the sense that many other people have the same thing. That being said, there are plenty of energy companies out there that do not. Valero and Marathon Petroleum are basically downstream companies and do not drill themselves. They are entirely dependent on outside companies for oil to refine. There is a risk there that Shell does not have.

Process Power

This is the big one for Shell. They are a classic integrated energy company. They locate and drill for oil both on land and underwater. They have their own oil rigs, tankers, and pipelines. They also have their own refineries and chemical production operations, ending at the gas station on the street corner. Shell has its hand in every single part of the production process. Now, it has competitors like Chevron, Exxon, and BP that do the same things. But this is a serious barrier to entry for any new competitor seeking to match their scale and expertise. Needless to say, learning how to identify oil reserves underwater, correctly place an oil rig, and drill underwater is not something any old small-cap energy company can quickly jump into doing.

Annual Report

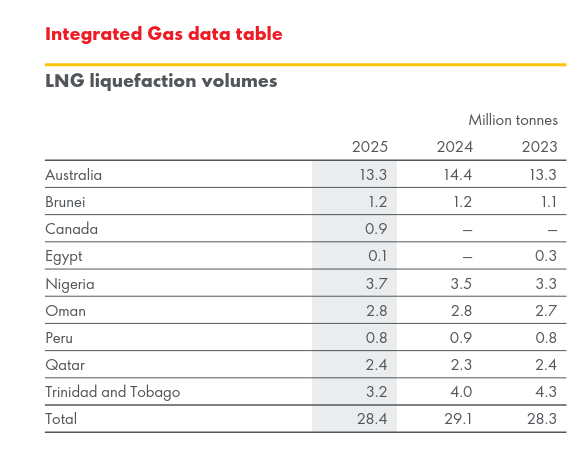

Integrated Gas - Page 28

$14.1 billion in cash from operations from LNG, out of $40.1 billion total.

This record was supported by the acquisition of Pavilion Energy which increased our access to third-party volumes. We also began production at LNG Canada and shipped the first cargoes from there, marking a significant milestone in our integrated gas strategy. LNG Canada, which holds a 40-year export licence, expands Shell’s global LNG portfolio, which is already one of the largest in the world.

There is a lot of focus on Canada for LNG and its dominance in that market, but at the end of the day, it is a small, growing, but for right now still small, portion of its LNG volume. Later on, I discuss a big acquisition that has stirred up even more excitement. I also think it’s interesting when a company that is making a bunch of noise about how great it is for making progress toward being environmentally friendly is doing business with countries where people don’t have rights. Probably the more serious and pressing concern is that Qatar, Oman, and Nigeria all have either literal slavery or de facto slavery present in their countries at high levels.

As I have said many times, I don’t really care about many of the moral quandaries that get other people upset when it comes to business. Shell isn’t using slave labor; it just gives money to governments that are okay with it. That’s enough for me not to care. I care about making money, and I have that in common with Shell; they only try to hide it behind climate change talk. I mention all of this, though, in case doing business with countries that have active and institutionalized slavery is a no-go for you. Writing that down, I’m guessing it will be a deal-breaker for some. That being said, it is my understanding that all the major energy companies do similar things.

Upstream - Page 35

$19.6 billion in cash from operations from LNG, out of $40.1 billion total.

The Upstream segment includes exploration and extraction of

crude oil, natural gas and natural gas liquids. It also markets and

transports oil and gas, and operates the infrastructure necessary

to deliver them to the market. Shell has activities in deep water

and conventional oil and gas.

Shell has drilling operations, or an interest in drilling operations, on every continent. If you want a full list, you will have to look it up yourself; it starts on page 37. It is way too much to copy here.

Delivering In The Gulf Of America - Page 41

In the Gulf of America (GoA), Shell is a leading producer and

operates 10 production hubs — making it a heartland for our deep-

water operations. With decades of experience, we are leveraging

our significant geological and technical expertise to deliver energy

profitably and at lower costs, while reducing emissions.

Their reserves are so immense that it is not a realistic concern anytime in the near- or mid-term future. Despite its name, this section covers a lot of information on reserves worldwide.

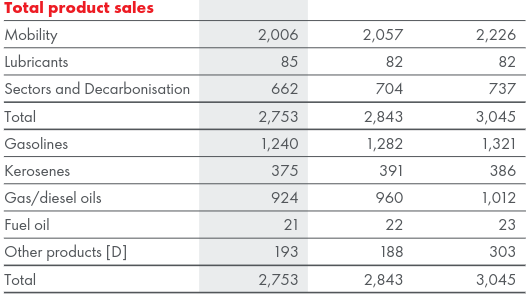

Marketing - Page 52

The Marketing segment comprises the Mobility, Lubricants,

and Sectors and Decarbonisation businesses. The Mobility

business operates Shell’s retail network including electric vehicle

charging services and the wholesale commercial fuels business,

which provides fuels for transport and industry. The Lubricants

business produces, markets and sells lubricants for road

transport, and machinery used in manufacturing, mining, power

generation, agriculture and construction. The Sectors and

Decarbonisation business sells fuels, speciality products and

services, including low-carbon energy solutions, to a broad

range of commercial customers including the aviation, marine

and agricultural sectors.

You see Shell tout EV charging, but by “retail network,” they are referring to gas stations.

When you see “mobility,” think gasoline sales at gas stations. Those numbers aren’t in dollars; they are in “thousand b/d” and reflect volume.

Chemicals and Products - Page 57

Chemicals and Products includes chemicals manufacturing plants

with their own marketing network and refineries which turn crude

oil and other feedstocks into a range of oil products, which are

moved and marketed around the world for domestic, industrial

and transport use. The segment also includes the pipeline

business, trading and optimization of crude oil, oil products

and petrochemicals.

and

Products – Refining and Trading

Refining

We have direct interests in seven refineries, with a total capacity

to process 1.4 million barrels of crude oil a day. The distribution

of our refining capacity is 64% in Europe, 32% in the Americas

and 4% in Asia.

and

Pipelines

We own and operate three tank farms across the USA through Shell

Pipeline Company LP (Shell interest 100%). It transports around 1.5

billion barrels of crude oil, refined products and chemicals a year

through around 5,400 kilometres of pipelines in the Gulf of America

and eight US states.

Our pipelines carry more than 40 types of crude oil and more than

20 grades of fuel including petrol, diesel and aviation fuel, and

chemicals including ethylene.

We own, operate, develop and acquire pipelines and other midstream

and logistics assets. Our assets include interests in entities that own

crude oil and refined products pipelines and terminals that serve as

key infrastructure to:

○ transport onshore and offshore crude oil production to US Gulf

Coast and Midwest refining markets; and

○ deliver refined products from those markets to major demand

centres.

Our assets also include interests in entities that own natural gas and

refinery gas pipelines that transport offshore natural gas to market

hubs and deliver refinery gas from refineries and plants to chemical

sites along the US Gulf Coast.

^^^That is all part of the Chemicals and Products segment. Again, the big thing to notice here is sheer scale. Shell is an incredibly vast and global corporation and is one of a very small number of energy companies that operate at this scale globally.

Renewables and Energy Solutions - page 64

This is running at a loss currently, so small it doesn’t matter but a loss none the less.

The Renewables and Energy Solutions segment includes

renewable power generation; the marketing, trading and

optimisation of power and pipeline gas; and carbon credits. The

segment also includes the production and marketing of hydrogen;

development of commercial carbon capture and storage hubs;

investment in nature-based projects that compensate for carbon

emissions; and Shell Ventures, which invests in or works with start-

ups and early-stage businesses to help them scale up and grow.

This climate bullshit from an energy company is annoying to me. It’s like Philip Morris getting into cancer research. Quit trying to act like the hero of the story and stay in your lane. The lane is providing the energy that runs all of human civilization and making a pile of money. Researching alternative forms of energy? Then show me the money. Hydrogen? Cool, how are we earning from this and when? I’m a patient person, I’ll wait years, but there needs to be a coherent plan articulated.

Also, notice that after talking about climate change every two seconds, they are doing nothing meaningful. I think it’s great; they aren’t wasting large sums of money on technologies that might never work. Having a clear vision is good, but talking such a big game while doing very little is obnoxious.

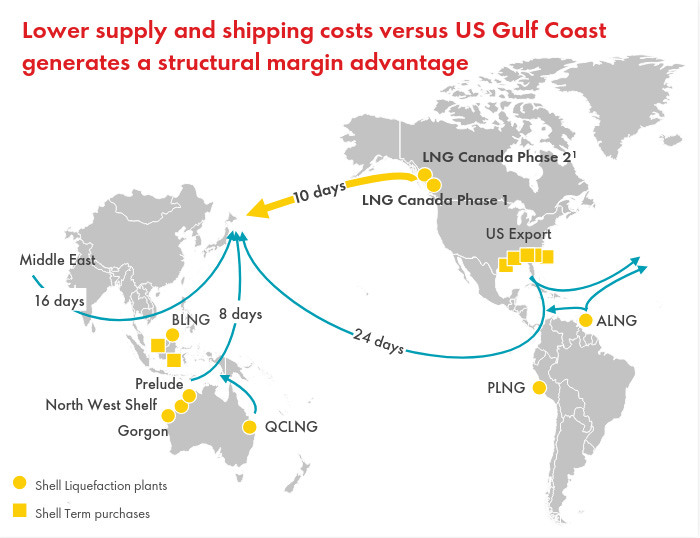

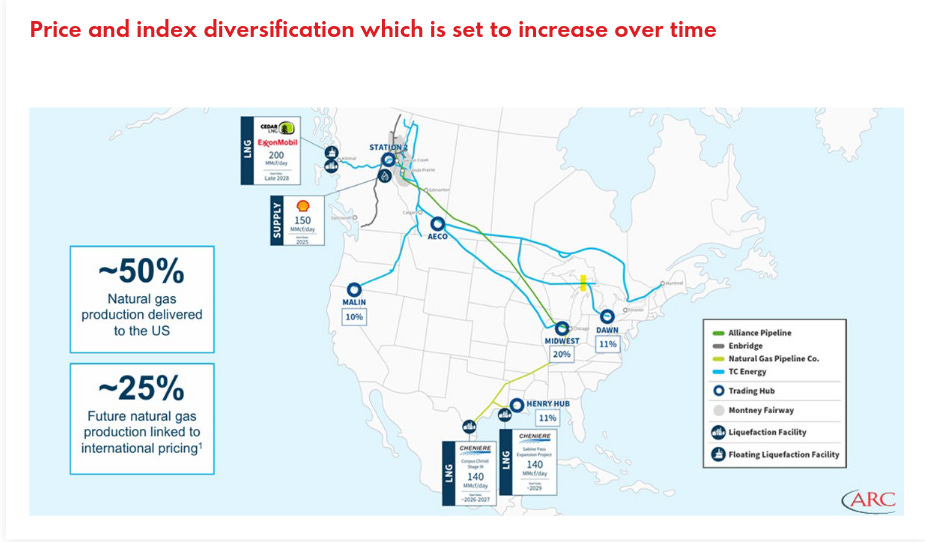

I sort of stuck this in here very awkwardly. Shell has been talking a lot about Canada. I have been seeing my Canadian energy stocks go gangbusters for reasons that are hard to discern. Then I see a major energy company making a large acquisition in Canada. Hmmm… interesting.

Shell bought out ARC Resources, a Canadian energy company. After the acquisition, Shell is the #1 LNG operator in Canada, and it puts Shell as the #3 shale operator in the Montney Basin.

This helps explain Shell’s Canada fixation:

I always want to encourage people to remember how freakishly internationally vertically integrated energy companies are. I can’t help but mention it again. In this diagram, Shell is demonstrating how its footprint in Canada accelerates its ability to get product from North America to East Asia by two weeks. Shell essentially could have looked at a map of the world and said, “Hmmm… wouldn’t it be nice to have a shipping terminal there?” and then just bought out a local energy company like a game of Risk. Frankly, it would be easier to name the places on earth where they aren’t doing business.

This is another example of the scale of the infrastructure that is at work. Shell’s footprint in Canada gives them a greater ability to target markets in East Asia, Canada, and the United States. It’s a very solid move. I have been puzzled by the jump in Canadian energy stocks, however much I do enjoy benefiting from them. Seeing this made me wonder if larger energy companies are moving into the market and if typically low-PE Canadian companies are starting to get fairly valued. A massive company like Shell moving into the area certainly drew attention.

Alright, Shell is turning out to be another boring, well-run company whose financial statements I don’t find very interesting. This usually means I’m about to make money, but this game of making money is boring and low-adrenaline. I think it is part of why some people are so horrible at investing; they think excitement = good. Also, sadly, boring doesn’t let me look smart…

Charts:

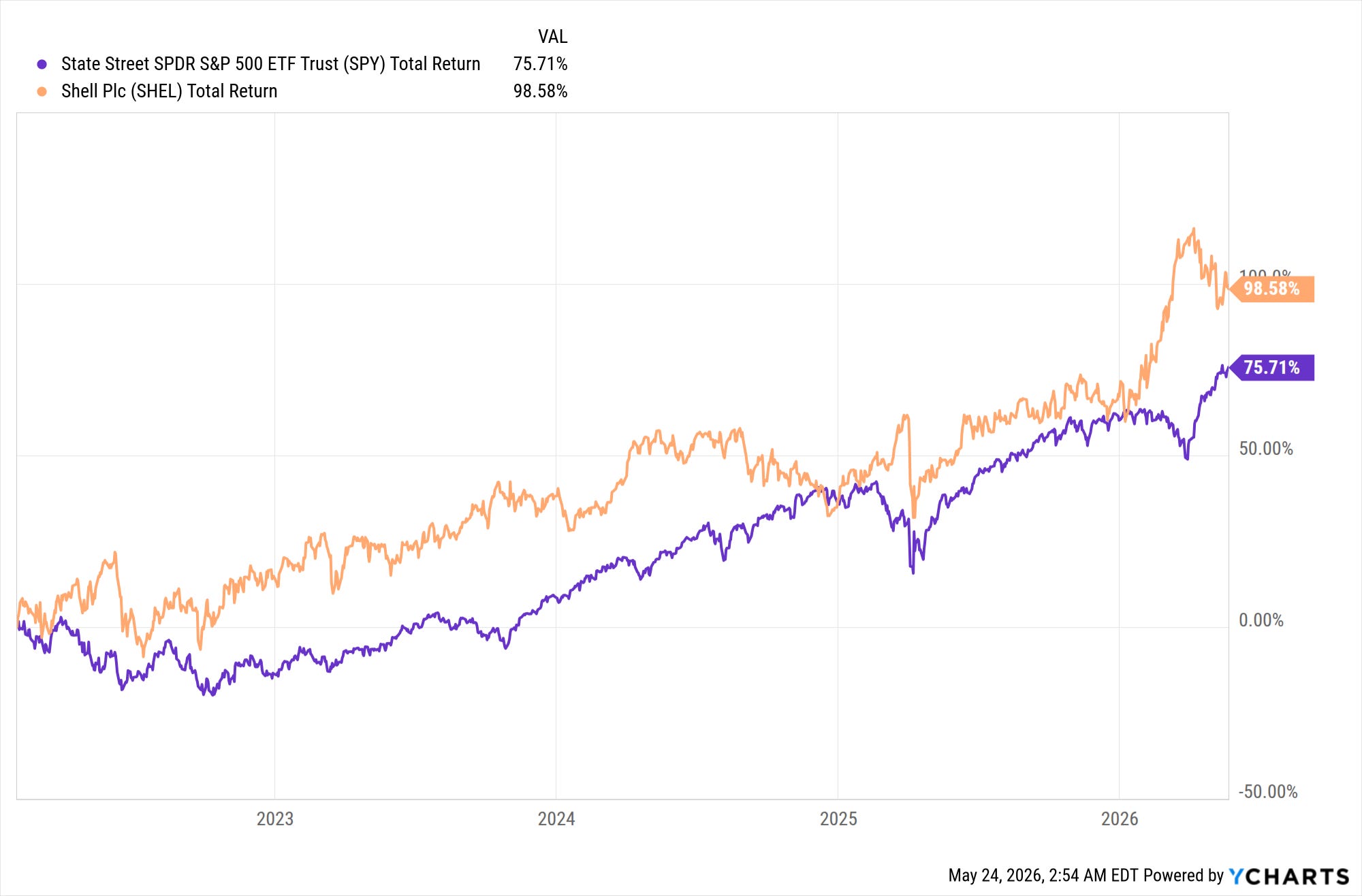

The price history is short because Shell changed its ticker a few years back. That being said, this is the best they have performed against the S&P in a long time. All the more impressive that it is happening during a tech bubble.

Interestingly, the charts only take me back to the last few years when it comes to total return…

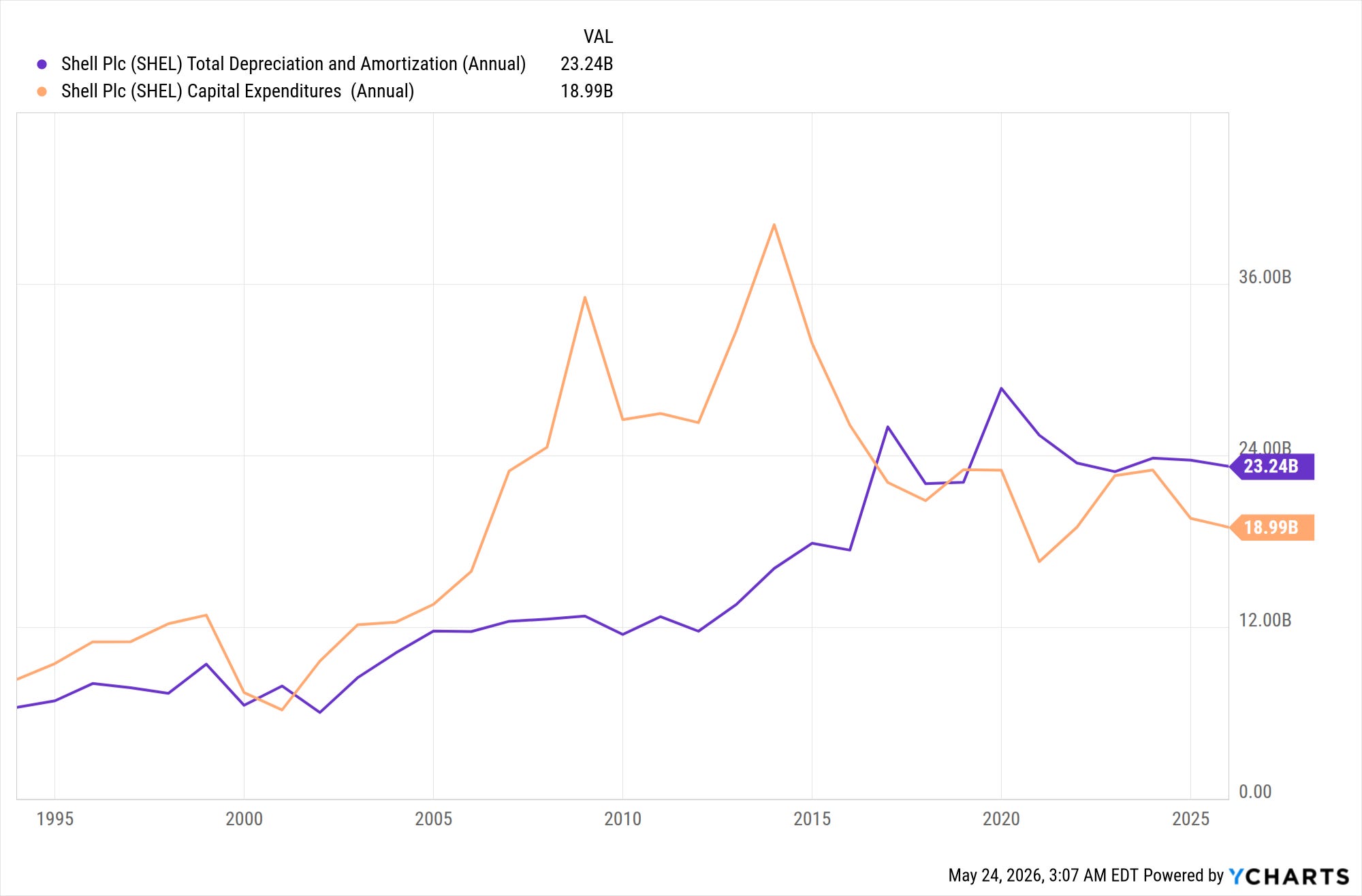

Depreciation to Capex

The idea here is to check if Shell is replacing what is getting old and fixing what is broken. Are they being fools and flinging money back at shareholders at the expense of the business? Fortunately, that does not appear to be the case.

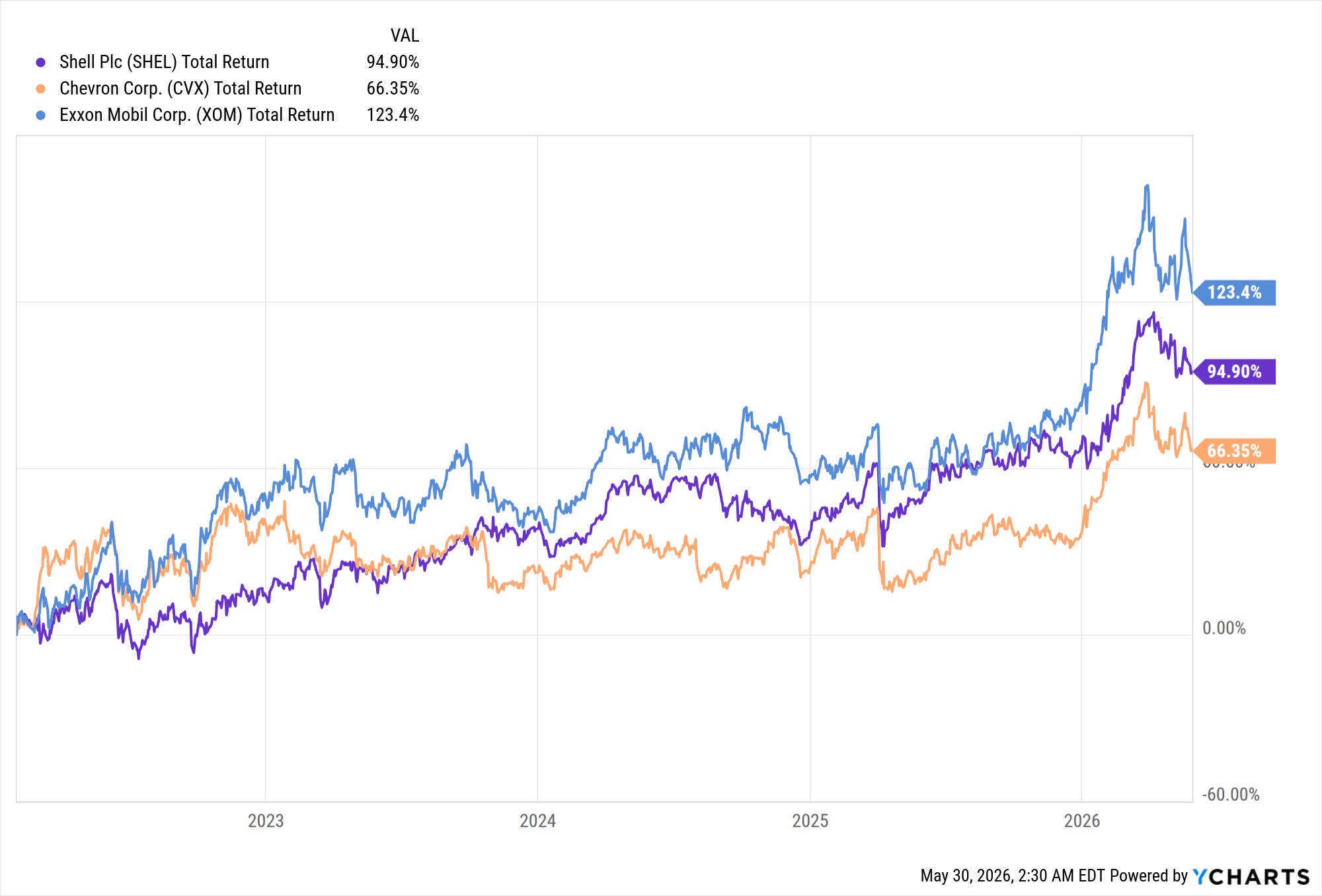

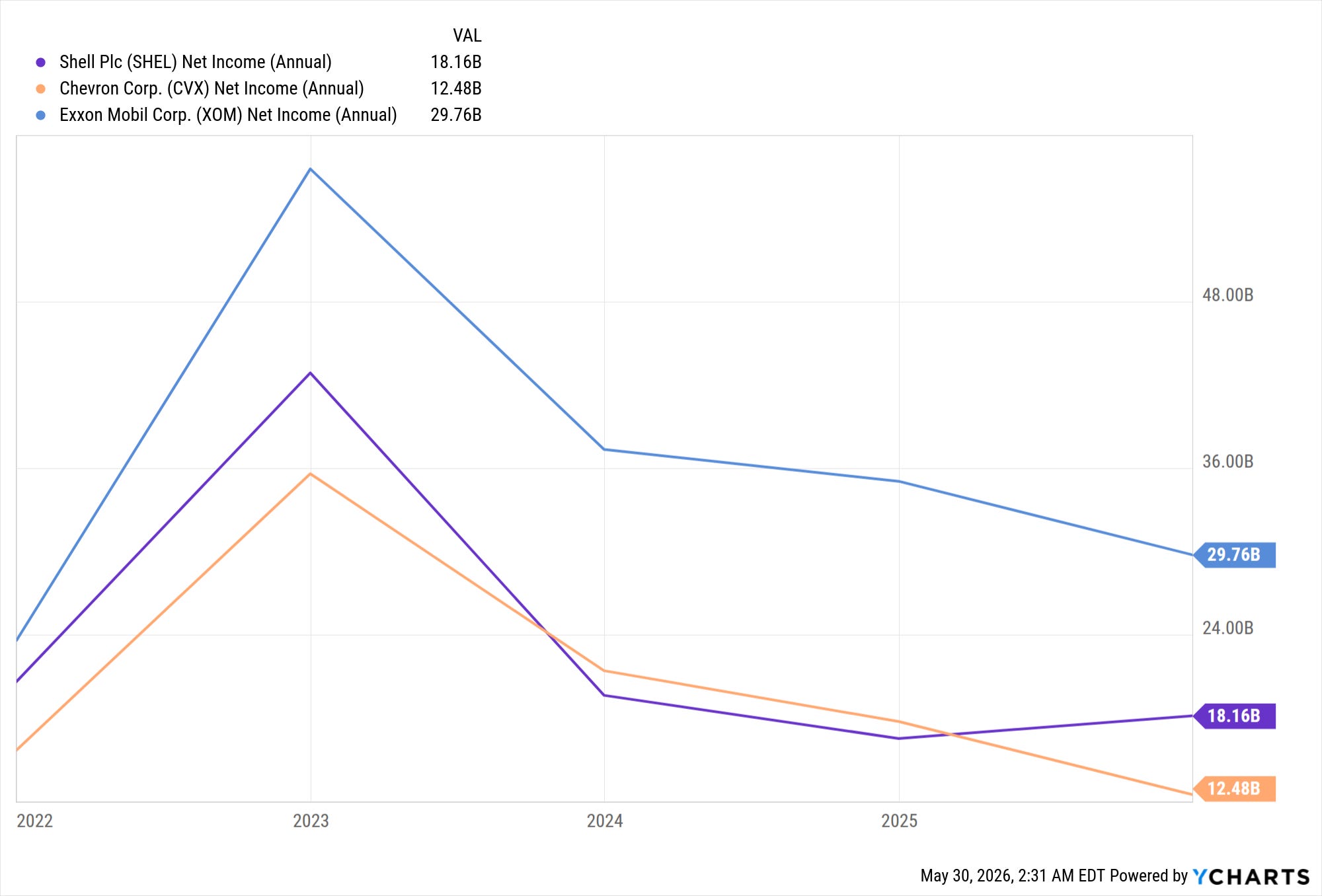

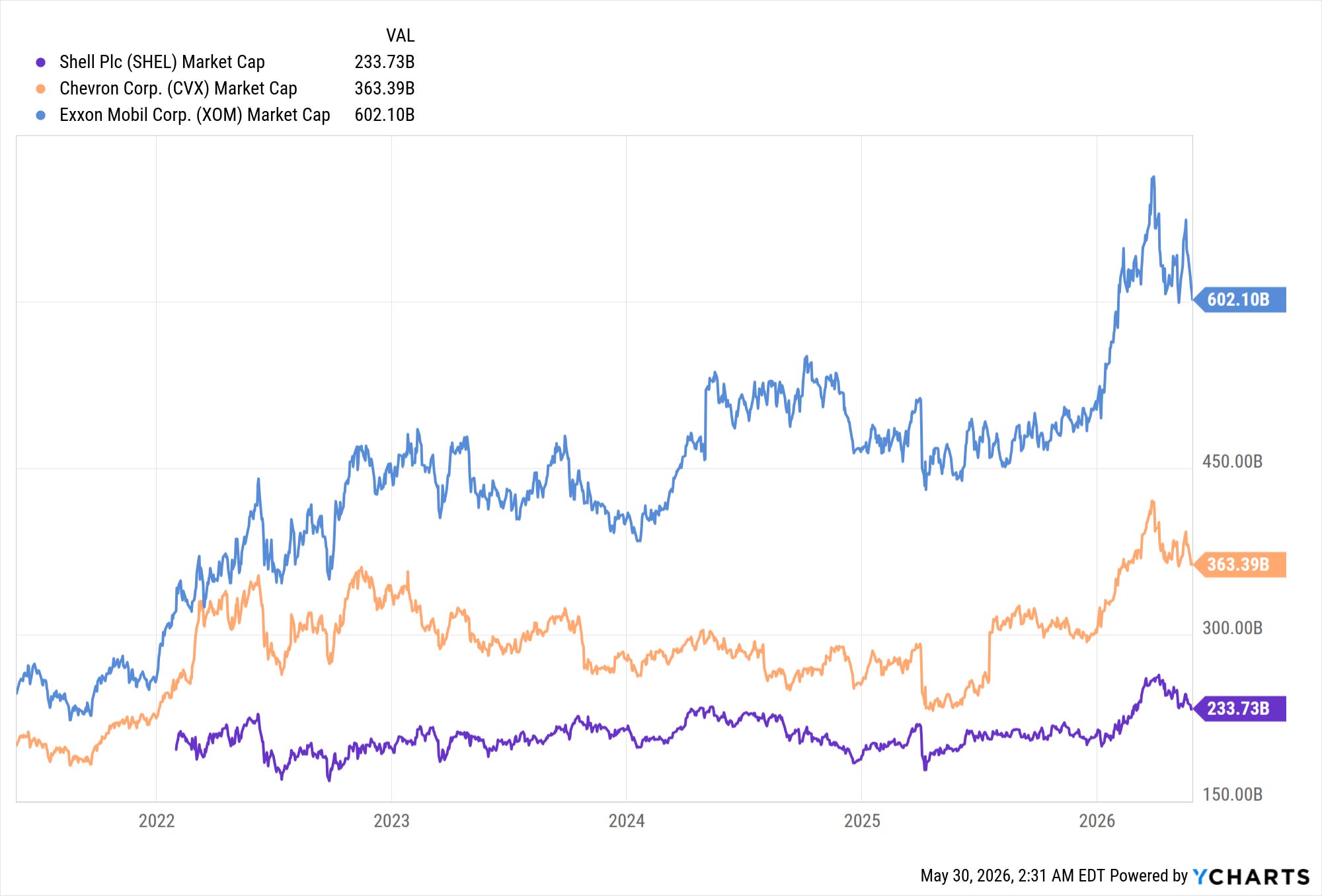

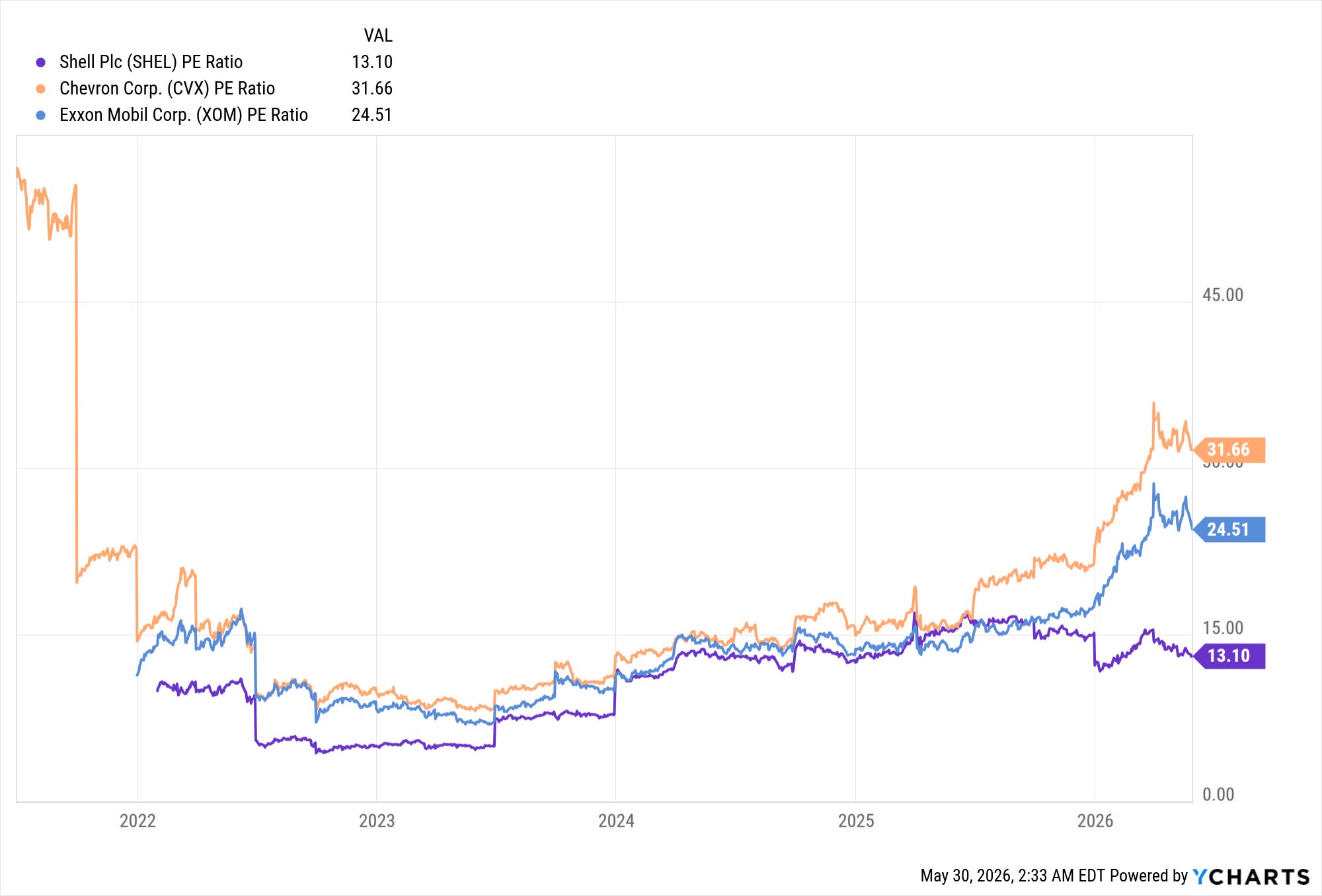

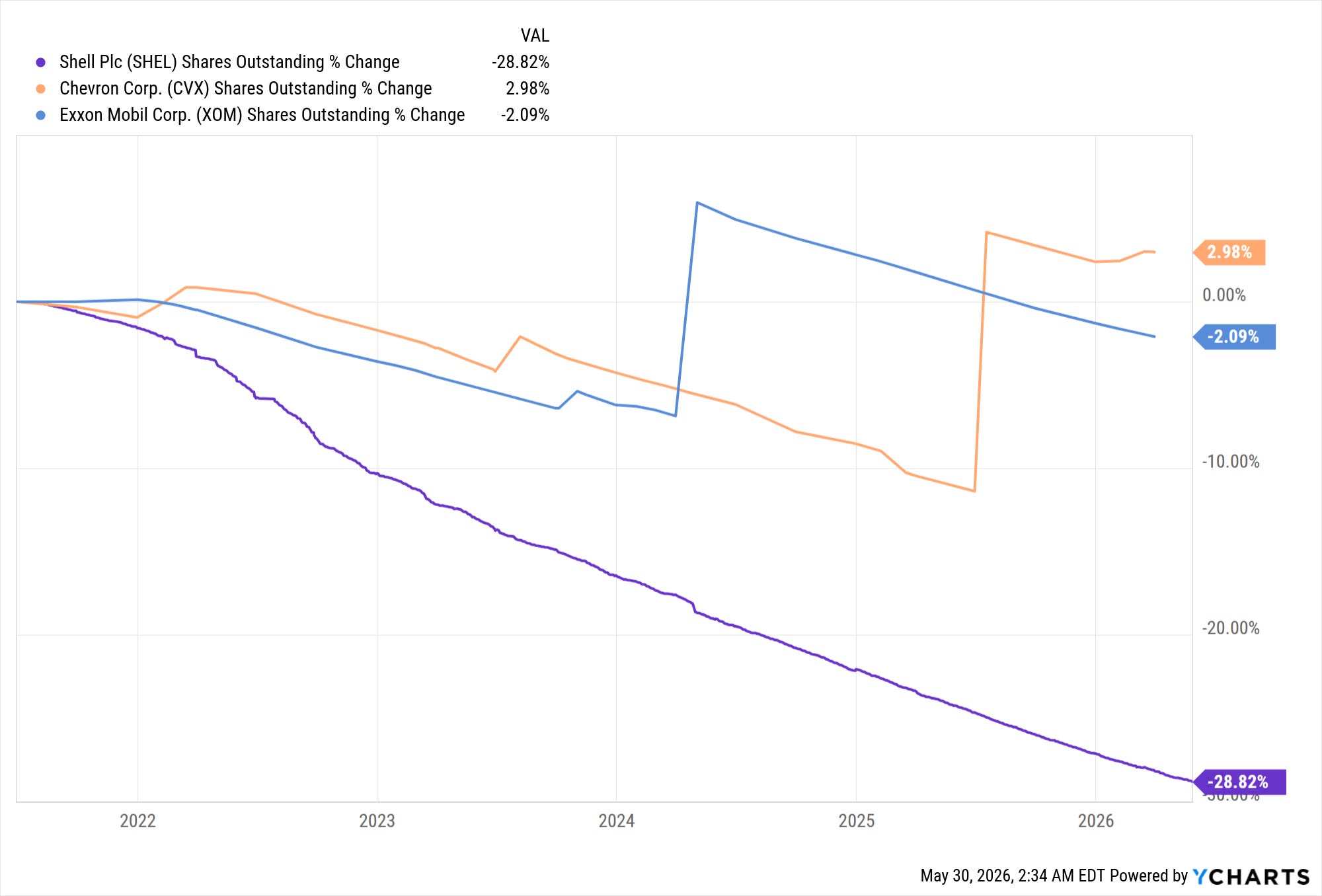

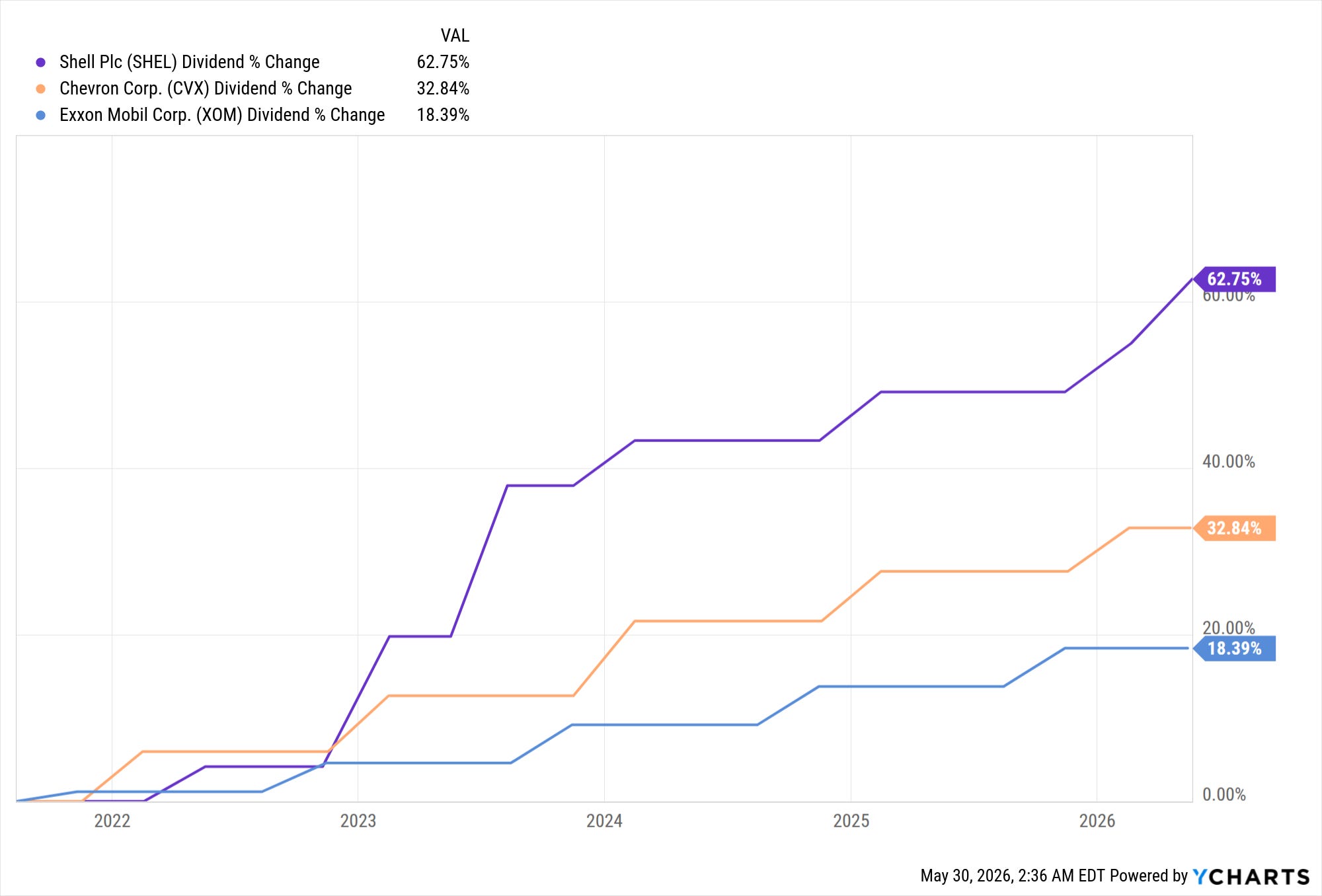

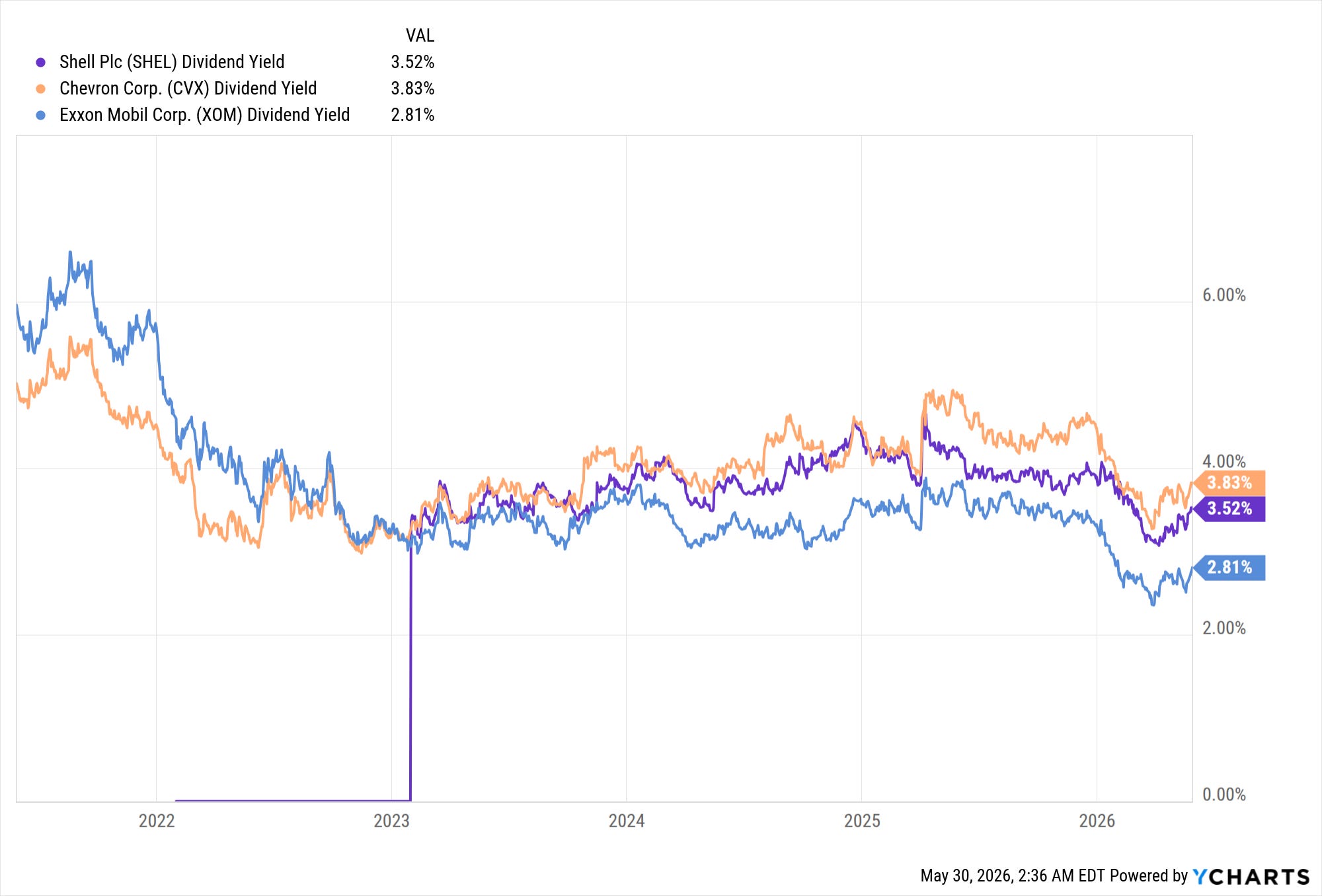

For some reason, I haven’t been doing more of this, but I am going to compare Shell to its competitors with some charts. I am only comparing it to vertically integrated competitors, such as Exxon and Chevron. Some other energy companies, like Valero, might pull ahead in profitability, but there is a risk there since they don’t control all parts of the production process. That being said, I have recommended Valero in the past. Each type of energy company has its merits, but I don’t compare them to each other in an apples-to-apples kind of way.

Looking at these charts, it’s pretty clear why I’ve moved away from Chevron as an investment. I have owned it in the past, but it clearly lags in every single category. The next question would be: why not Exxon? Well, we have Exxon at a P/E of 24.5, and Chevron is at a P/E of 31.6. Both are far more expensive than Shell, which is sitting at a P/E of 13. Also, Shell is doing far more share buybacks, and they are growing their dividend the fastest. As I showed above, they are doing all of this without skipping out on necessary capex and expansions of the company. As I mentioned in the beginning, there aren’t many energy companies in the world that are capable of doing what Shell does, and the bar is high for new entry.

I haven’t done an Easter egg in a while, but I’ve got one for you. I often get annoying people asking me why I think I’m smarter than everyone else, why I think I can be successful investing when others are not, or why I think I can beat those with a formal education in this field. There are many responses to this, but I did just pick up a new one. It’s not that I’m smarter than other people; it’s more that I lack stupid. Most people can’t be bothered to learn basic things about life, even ones that are very important to them, and I don’t think that changes with level of education.

Here’s one example: you don’t know this, but I am covered in tattoos. A completely solid sleeve on my left arm, and the back of my left hand, soon to be the same deal on my right arm, and about half a dozen more scattered all over the place. I don’t have many small tattoos, only twice have I sat for less than three hours for a tattoo Anyway, I’ve noticed people getting tattoos related to Greek mythology that are entirely incorrect.

Ever heard of Pandora’s Box? Yeah, it’s actually a jar, not a box. Ten seconds on Wikipedia will tell you that, and yet there is no shortage of Pandora’s Box tattoos out there. Ever seen an image of Atlas holding up the world? Yeah, that’s wrong too. He was cursed to hold up the sky or the cosmos, not the earth. When the exploration of the earth by sea travel started, people saw Atlas holding an orb and assumed it was the globe. Guess how many incorrect Atlas tattoos there are out there? Spoiler alert: it’s a lot.

People can’t even be bothered to do ten seconds of searching before inking themselves for life. You think this human penchant for laziness disappears just because someone has a master’s degree and is buying stock? I highly doubt it.

If you can be bothered to learn basic things, winning becomes a lot easier.

Anyway, for everything I have said, I plan on holding Shell for the foreseeable future, although I would say I am somewhere between a long-term and mid-term investor. I don’t do the blind buy-and-hold-forever game. Shell is on par with its peers in terms of financial strength and position. It is currently returning much more to shareholders and is trading for a lot less. I see Shell as a long-term winner. Something to keep in mind is that earnings bounce around with the price of oil for energy companies, and declining earnings can be out of the control of the company in the sector.

I’m a bit slower to write these days since it is ultramarathon time of year again and the mountains are thawing. Not even sanctioned races; you can see cool shit if you can run 50 miles between dawn and dusk, backpacking not needed.

Okay bye bye now.

My Portfolio:

HMENF, JPM, TOTZF, T, COF, UBER, SHEL

*I think it is worth stating that just because I hold a stock doesn’t mean I think it’s a good idea to buy it right now.

*Disclaimer*

You can and will lose money in the stock market. You can lose all of your money. I can and will be wrong. I have been wrong in the past. I have lost money in the past. Investing in stocks is risky and should never be considered safe. Invest at your own risk.

I was a bit disappointed when ARC was bought over by Shell and rotated out to Advantage Energy. Canadian names are getting bought out for one time premiums.