ONEOK (OKE)

Pipes and things that are both flammable and inflammable.

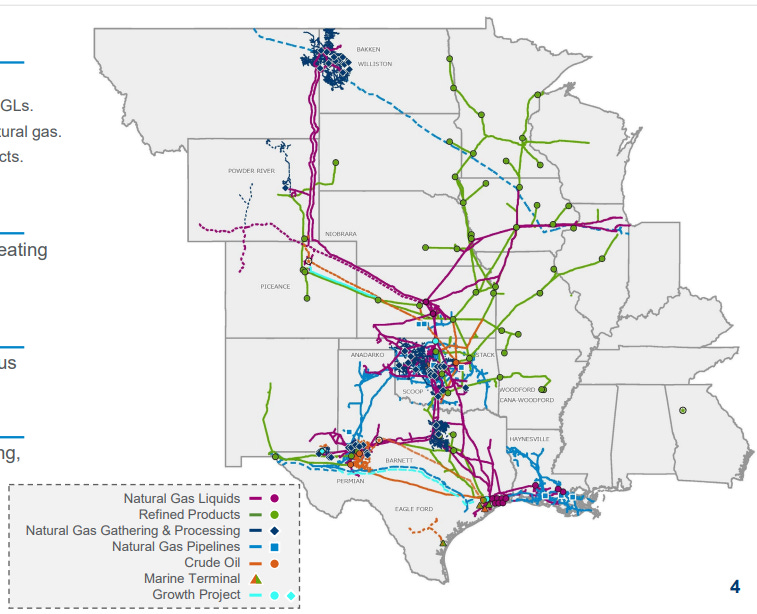

Oneok (OKE) is a U.S.-based midstream energy company that gathers, processes, transports, stores, and markets natural gas, natural gas liquids (NGLs), crude oil, and refined products. The company serves as a key intermediary between energy producers and end users, including refiners, chemical manufacturers, utilities, and exporters. Its business model relies on long-term, fixed-fee contracts that provide predictable cash flows and limit exposure to commodity price fluctuations. This is what is meant by the term “midstream.” OKE doesn’t drill or extract fossil fuels, nor does it sell them directly to the general public. Midstream companies operate between upstream drillers and downstream sellers within the energy supply chain.

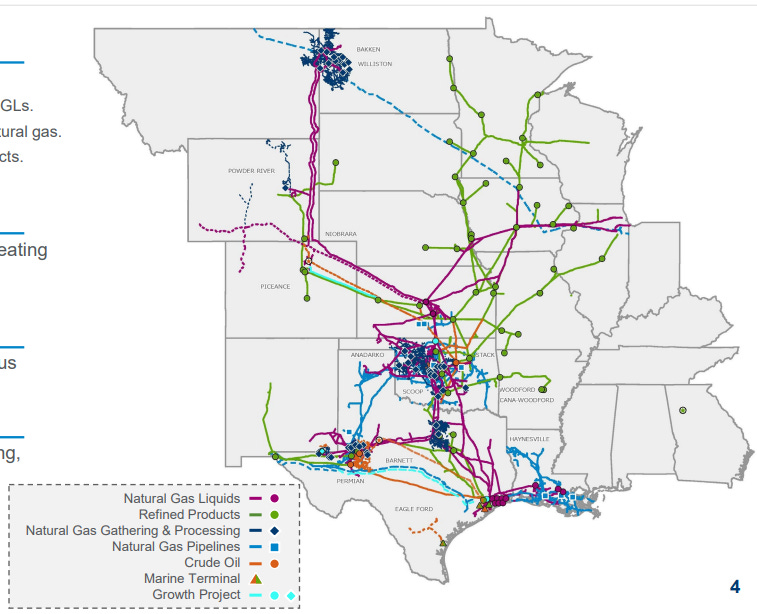

Oneok’s largest business is its natural gas liquids (NGL) segment, which gathers and processes raw NGL mixtures into refined components such as ethane, propane, and butane. It then transports and sells these products to industrial customers. This segment is geographically limited to the U.S. midcontinent, which restricts access to higher-value international markets. To address this, the company has partnered with MPLX to build a pipeline and export terminal on the Gulf of Mexico. Despite its importance, the NGL segment carries the firm’s lowest operating margin,around 18%, due to higher input costs and domestic pricing constraints.

The refined products and crude oil segment, established through Oneok’s acquisition of Magellan Midstream Partners, includes pipelines and terminals that transport and store crude oil, gasoline, diesel, and other fuels. These assets connect key production areas, including the Permian basin, to end markets in the Great Lakes and Gulf Coast. Because the assets are interstate and maritime, they are heavily regulated and costly to duplicate, giving this segment a profit margin of around 40%.

Oneok also integrated assets from EnLink and Medallion into its network. EnLink’s systems in Louisiana and East Texas supply natural gas to LNG export facilities. Ensuring consistent demand, while Medallion’s Permian Basin operations gather and process crude and gas that feed into Oneok’s broader infrastructure. Also, the company’s natural gas gathering and processing operations involve connecting production wells to processing facilities that clean and prepare gas for transport.

Oneok is a diversified midstream company with a balanced portfolio across NGLs, natural gas, and crude oil. Its strength lies in efficient scale and capital-intensive infrastructure that deter competition. While most of its operations are rated as having a narrow moat, the refined products and crude oil business stands out with a wide moat and exceptional margins. Future growth is expected to come from export-oriented projects, integration of recent acquisitions, and ongoing investments that enhance capacity and stability across its network.

Given the prolonged bull market, I’ve changed my view a bit on stock performance. If a non-tech stock is tracking with the overall stock market during a tech-fueled cocaine frenzy, that’s extremely impressive. These days, I’m more willing to accept on-par performance with the stock market from stocks that are unrelated to the select few continuing to drive the S&P 500 higher and higher.

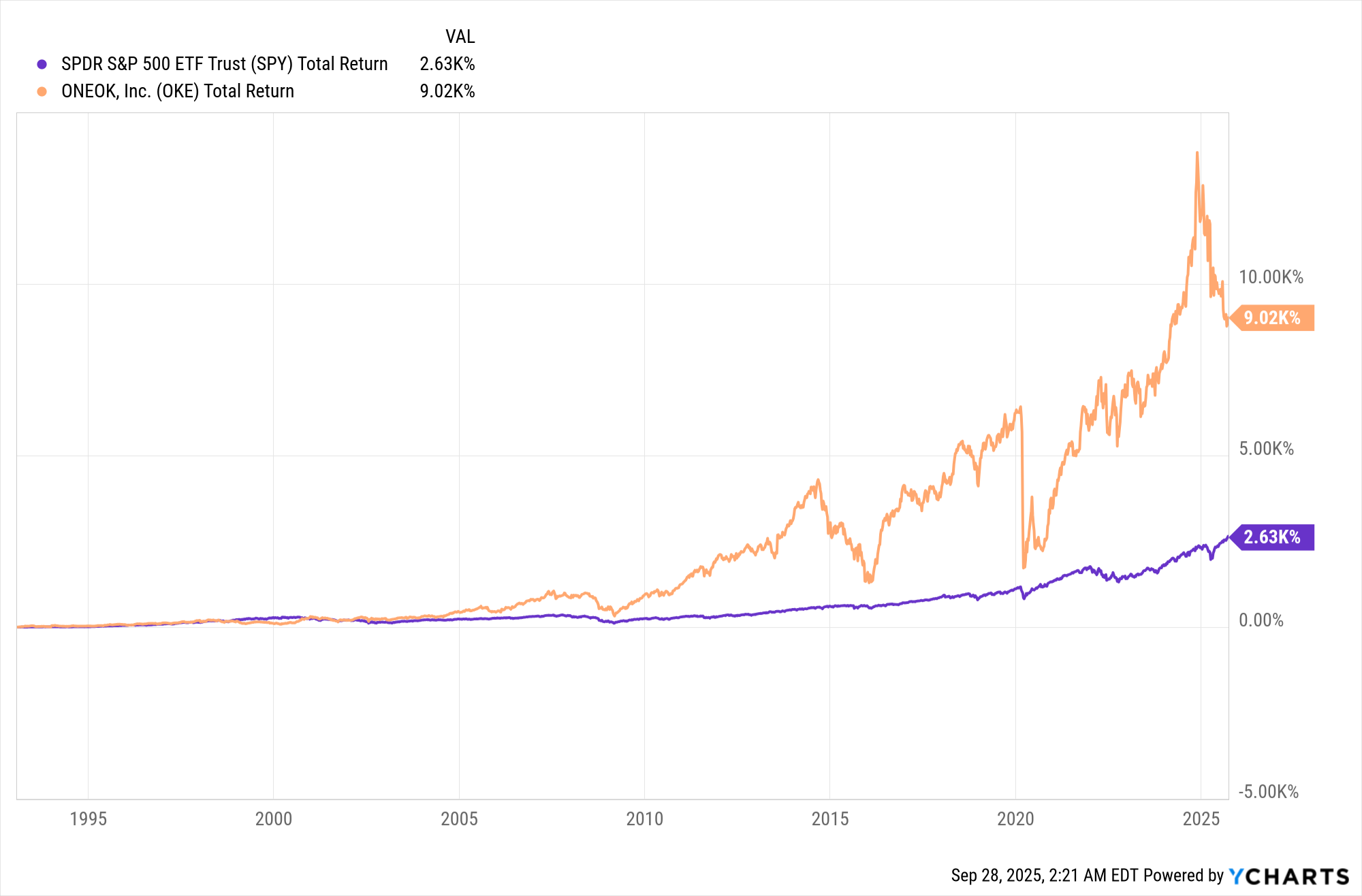

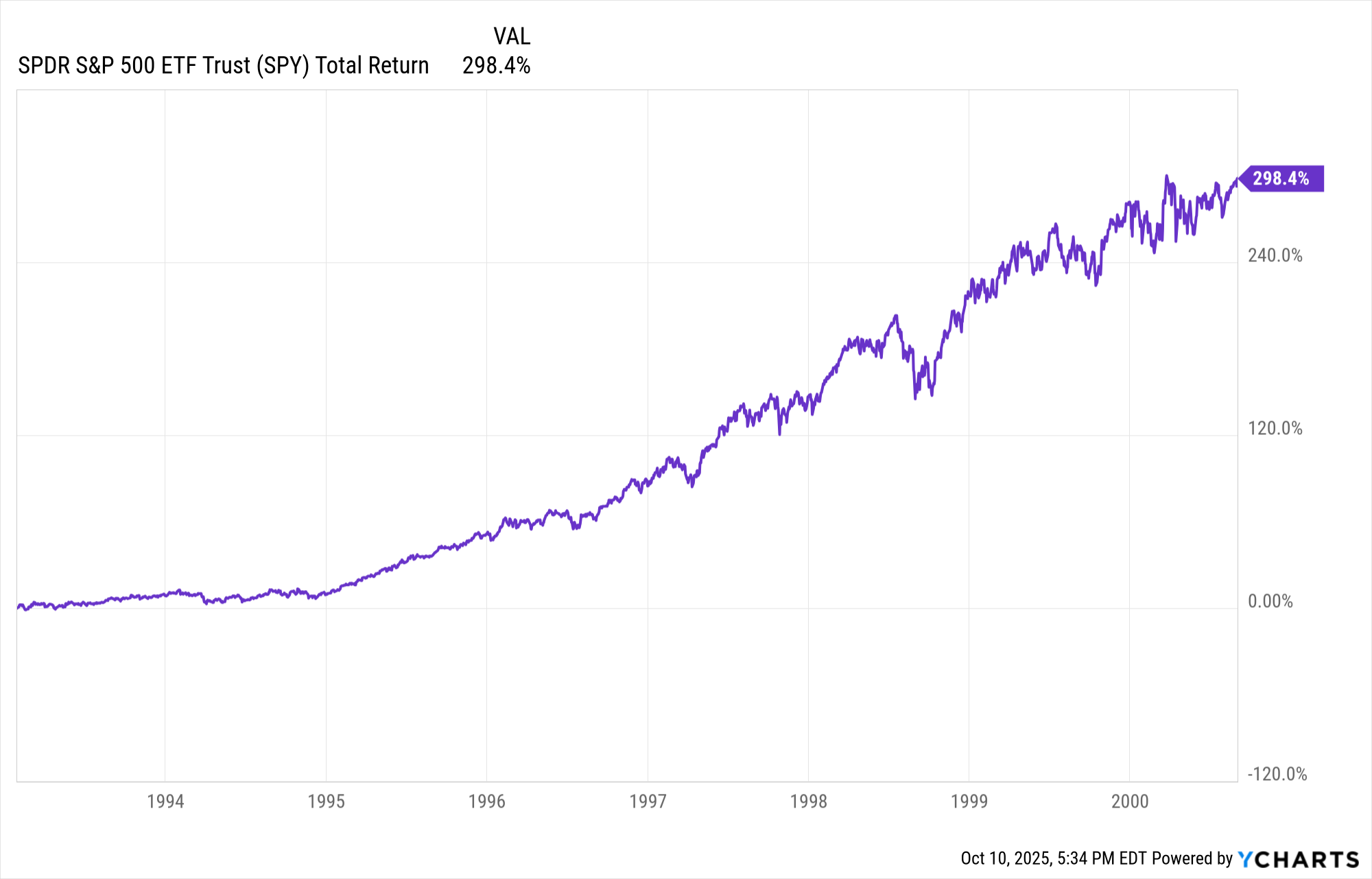

OKE vs. S&P 500 far back as I have data:

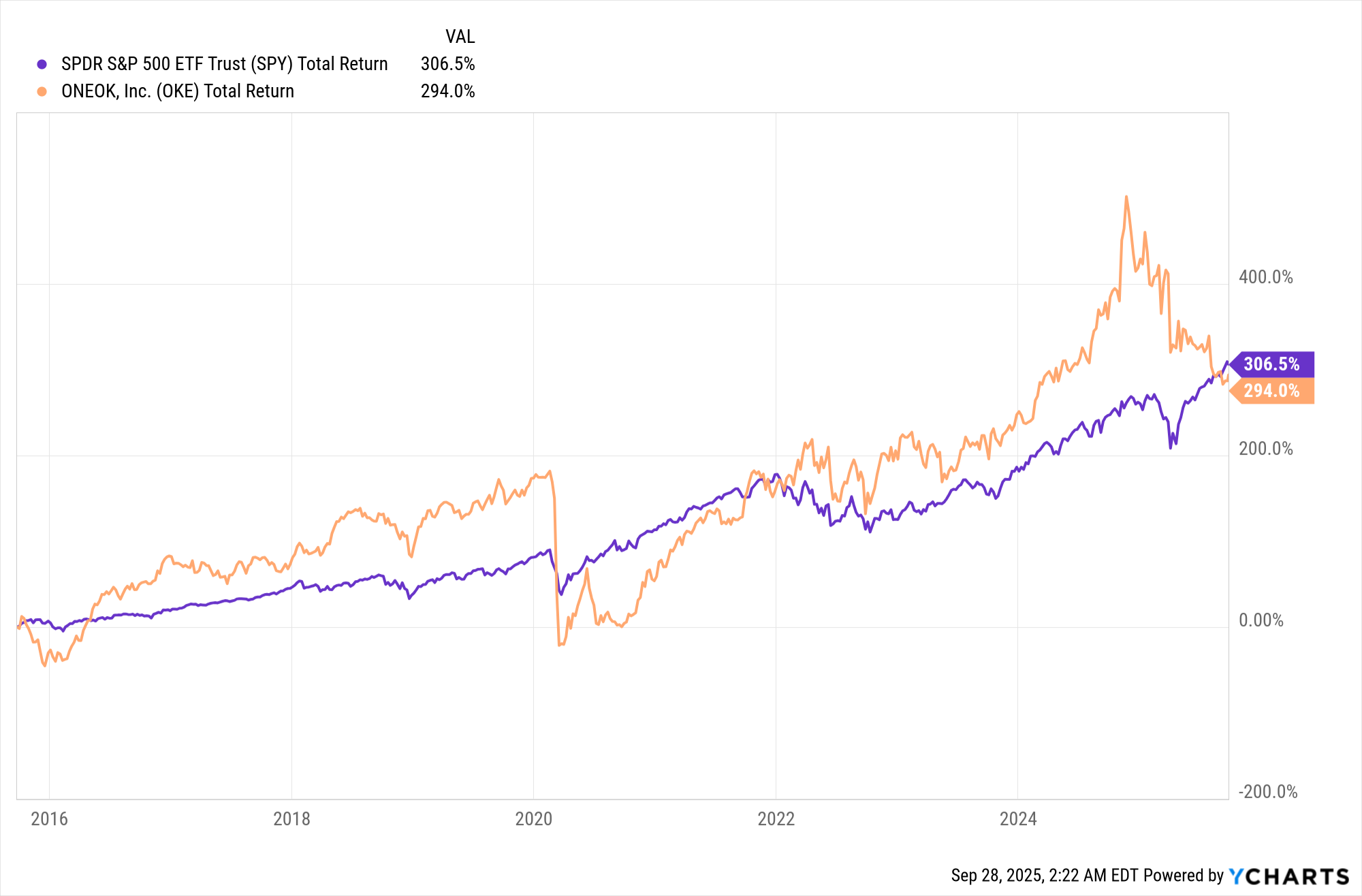

OKE vs. S&P 500 over the last 10 years:

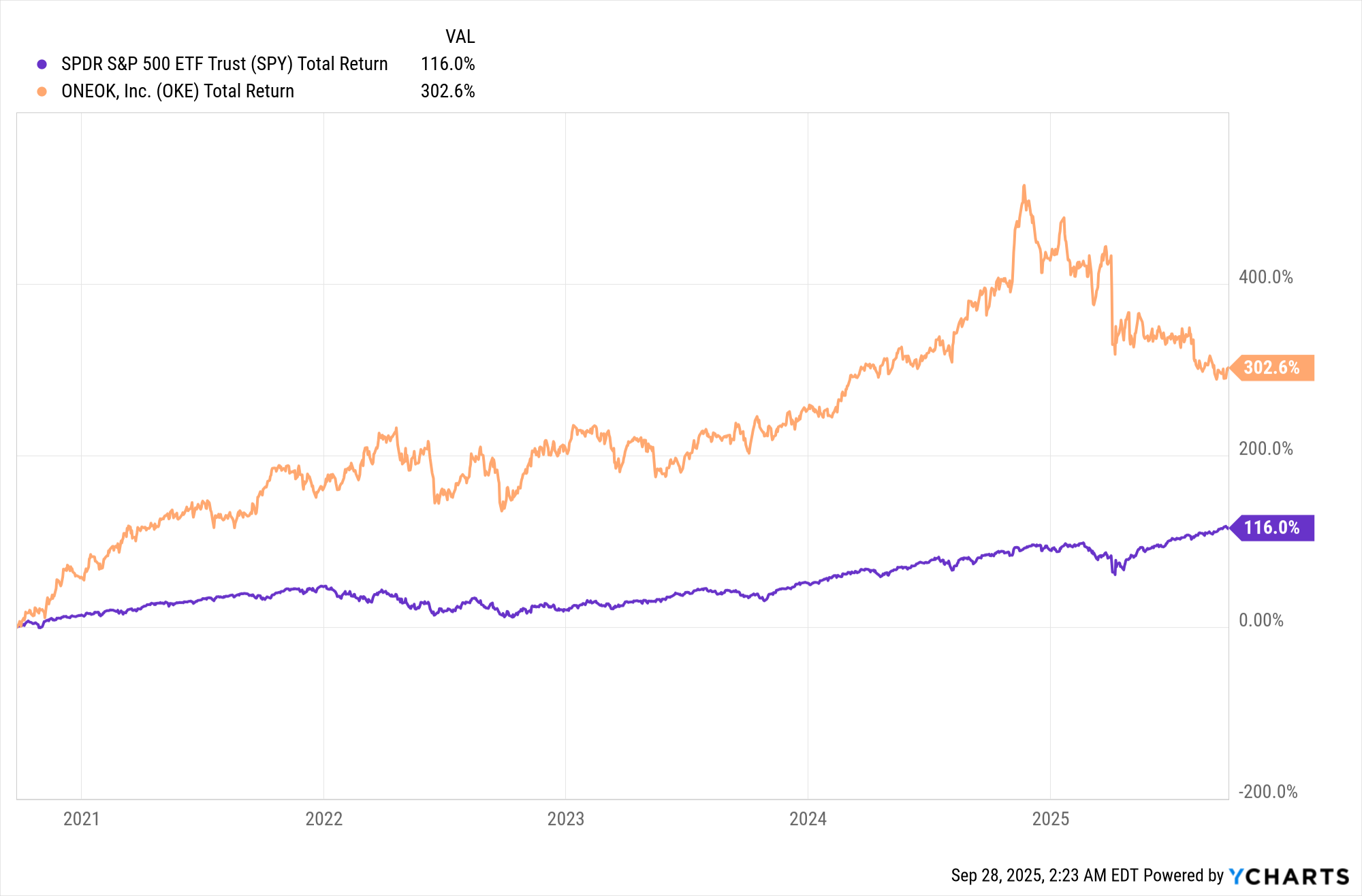

OKE vs. S&P 500 over the last 5 years:

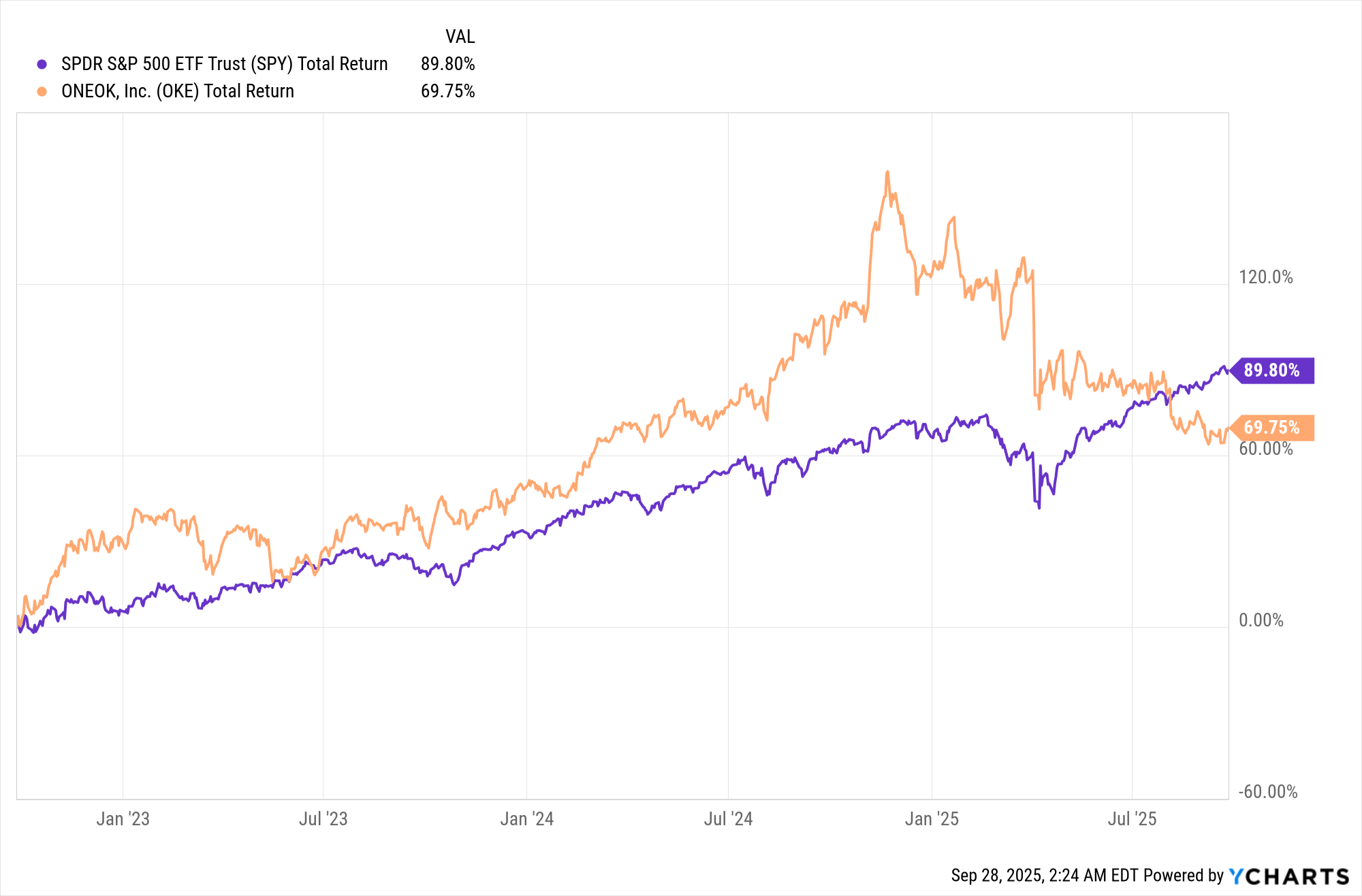

OKE vs. S&P 500 over the last 3 years:

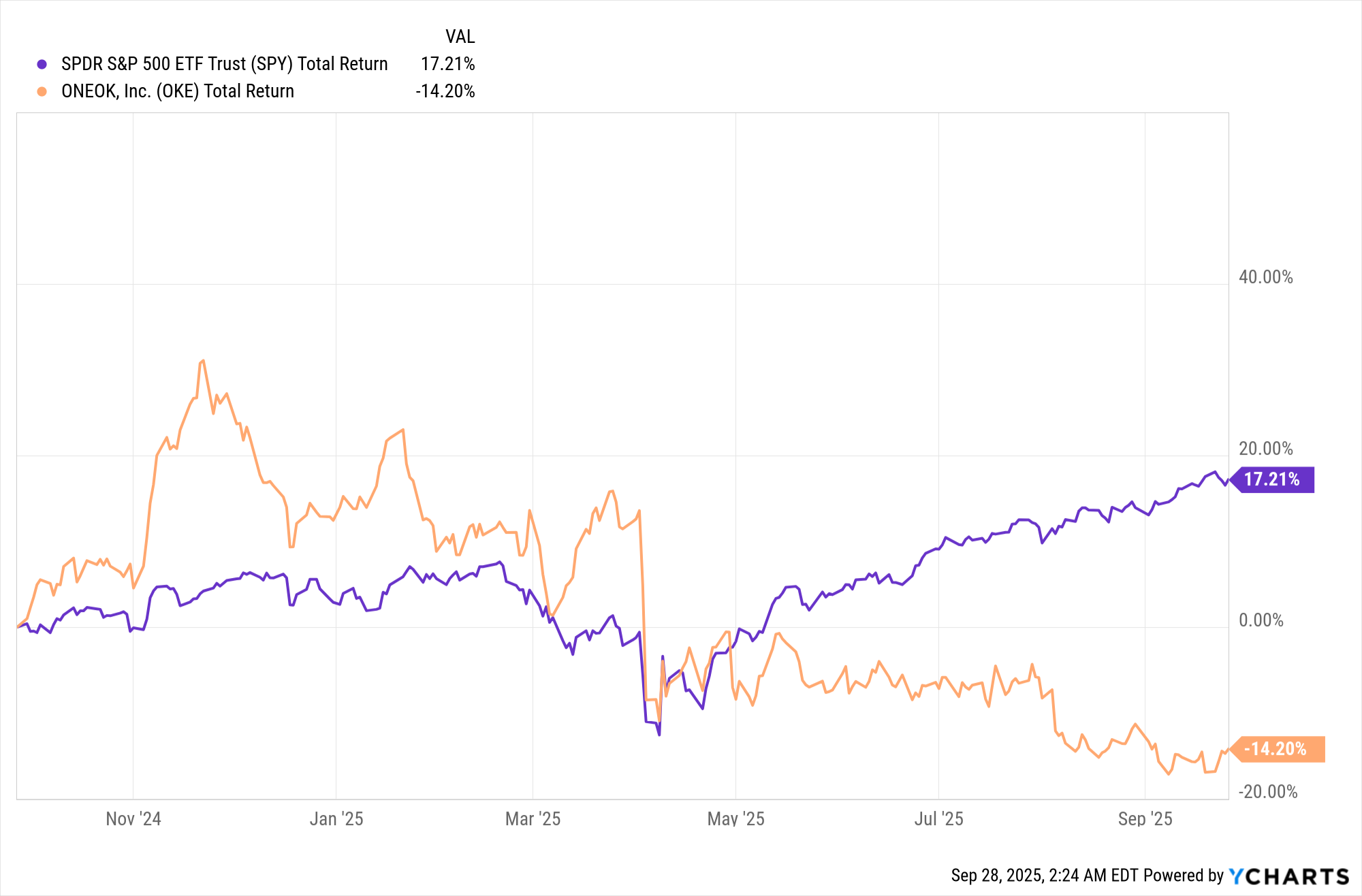

OKE vs. S&P 500 over the last year:

This is a great example of what I like about OKE: they don’t have the booms and busts that are common in the energy sector. I can handle volatility, but who doesn’t prefer stability, especially with their investments? OKE has been relatively steady, both on the way up and on the way down. Also, OKE, an energy company, has outperformed during a time when tech stocks have been going bonkers, driving the market higher and higher. That is very impressive and music to my ears.

You’ll notice that OKE has been trending downward for about a year, and even at its current P/E of 14, there’s nothing to stop it from sinking further.

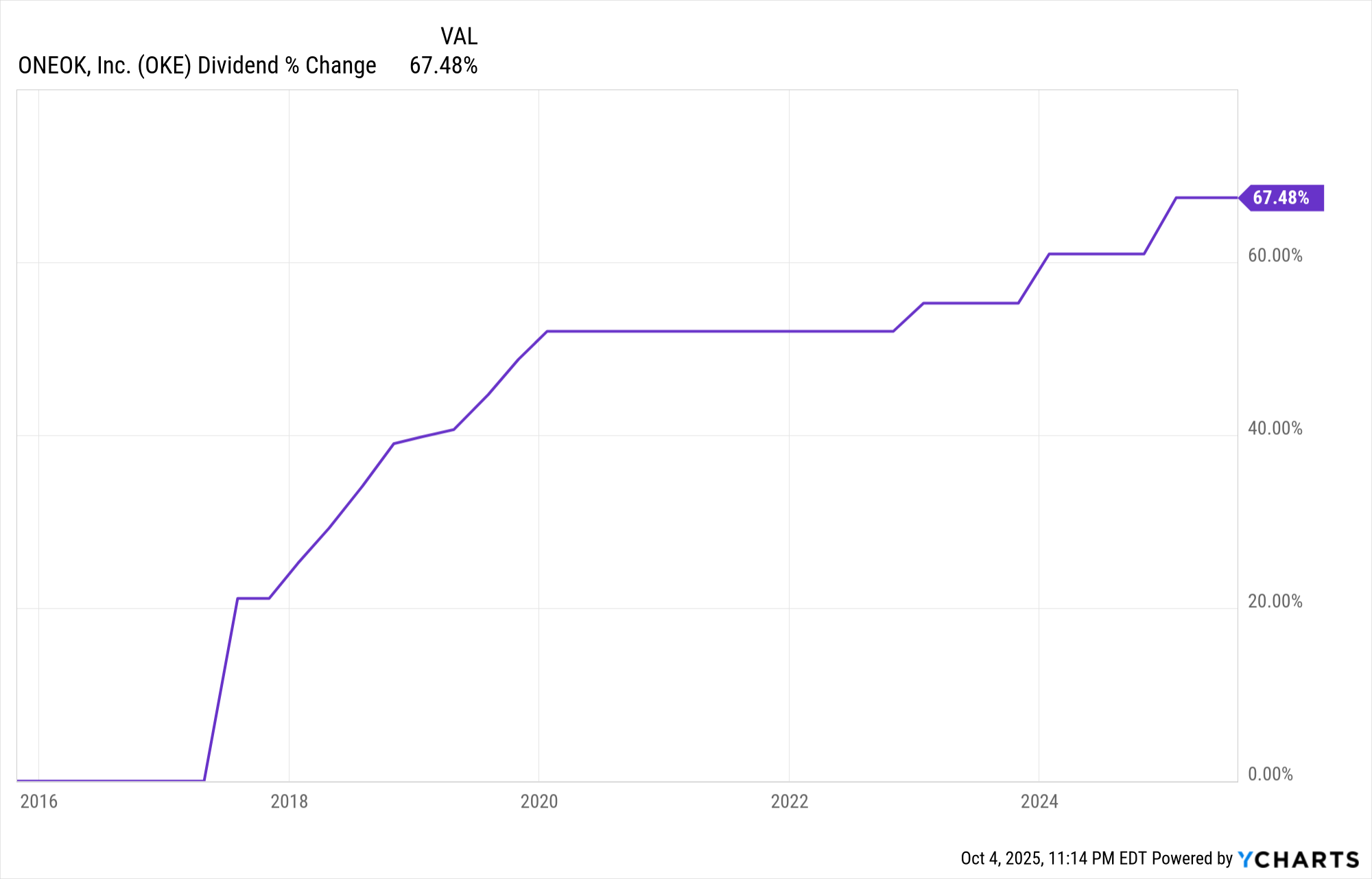

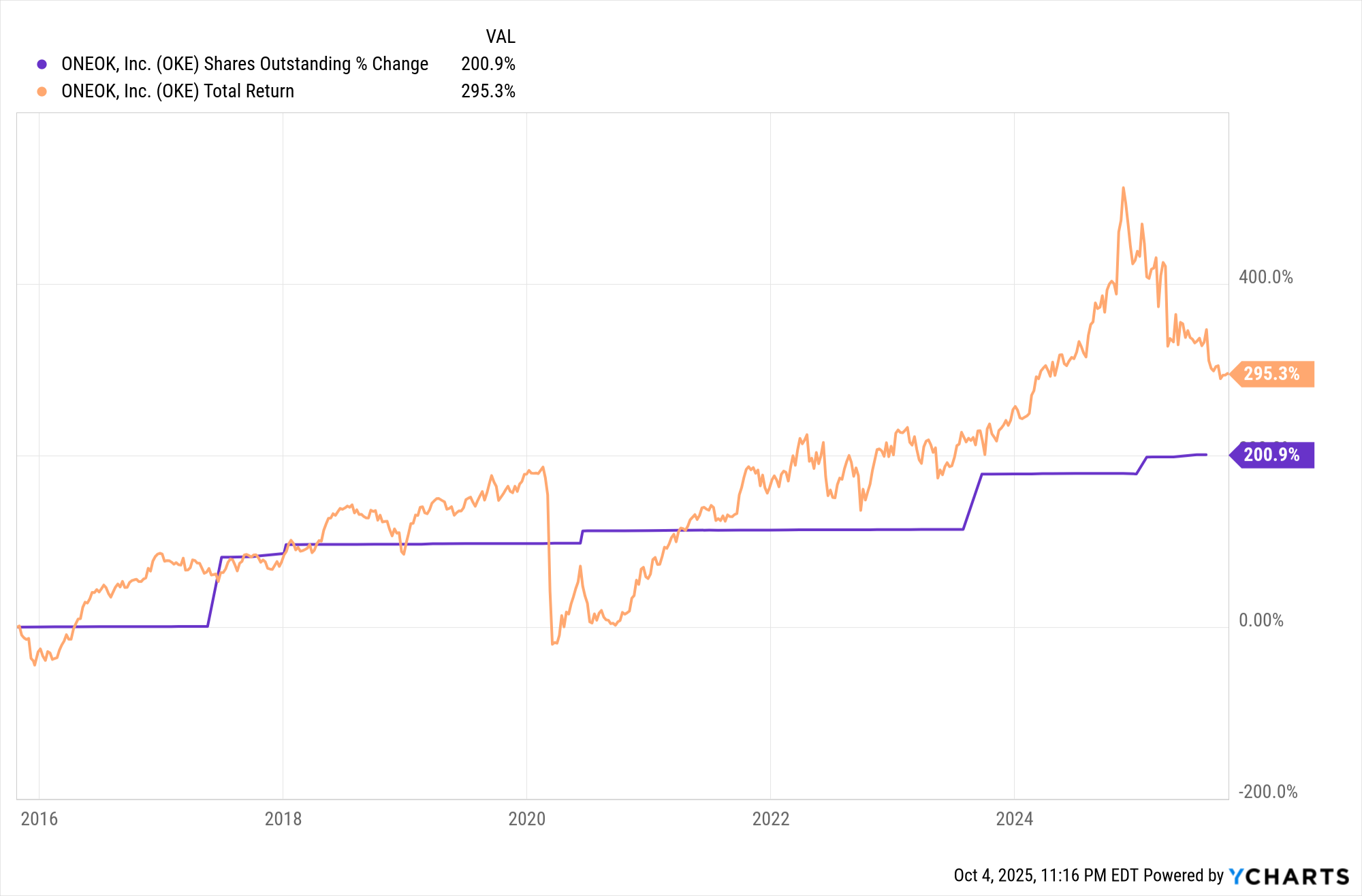

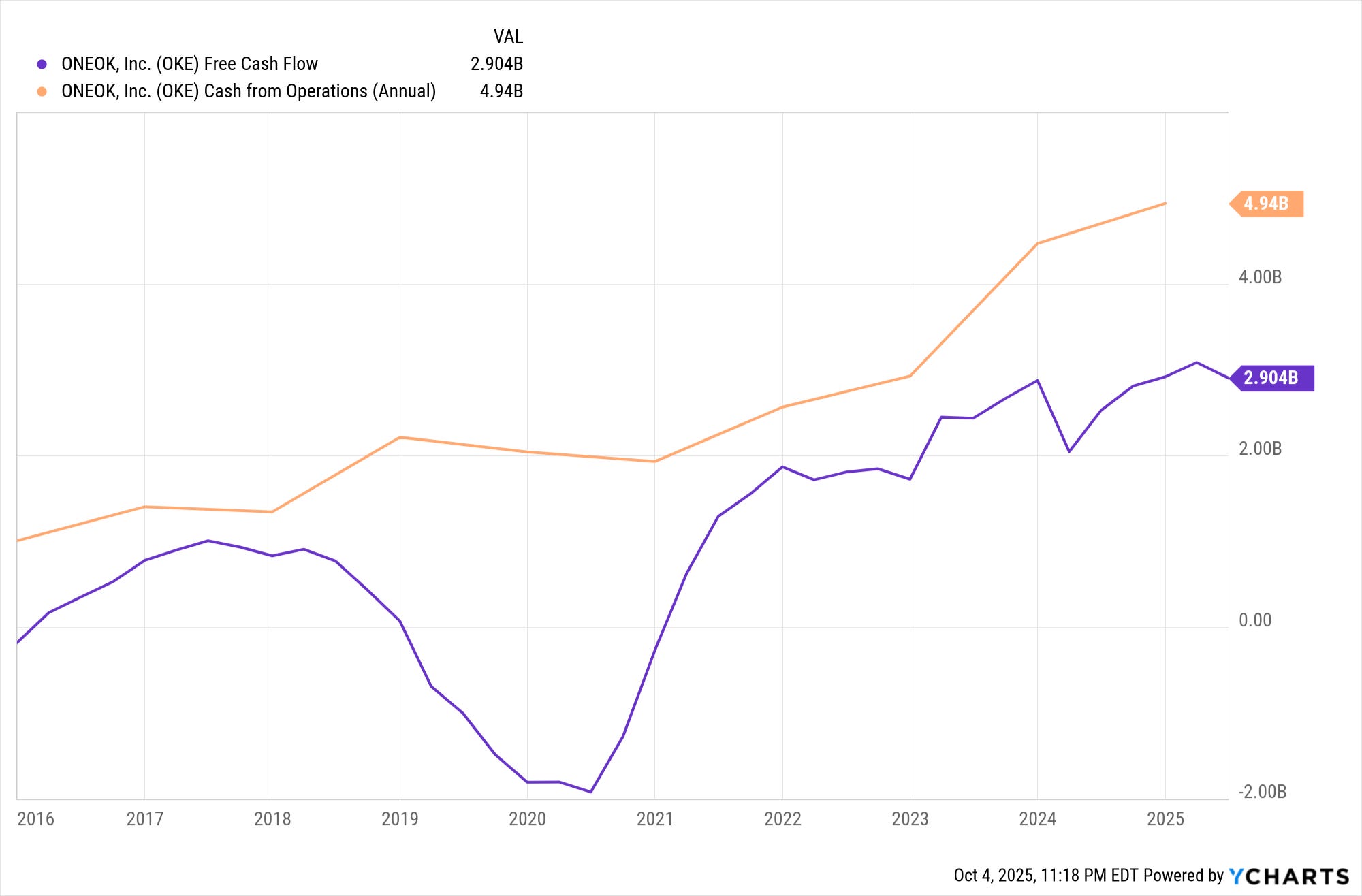

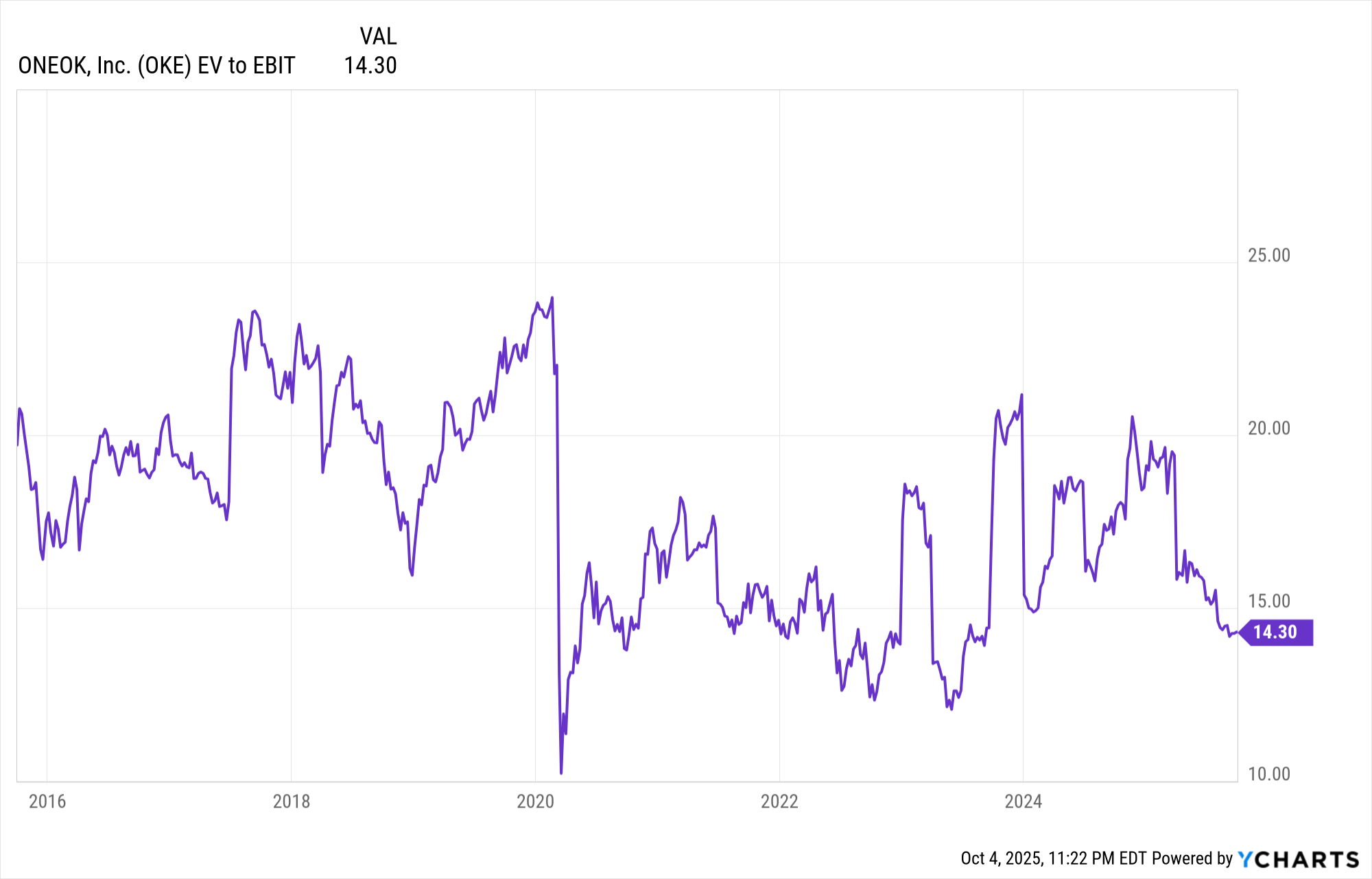

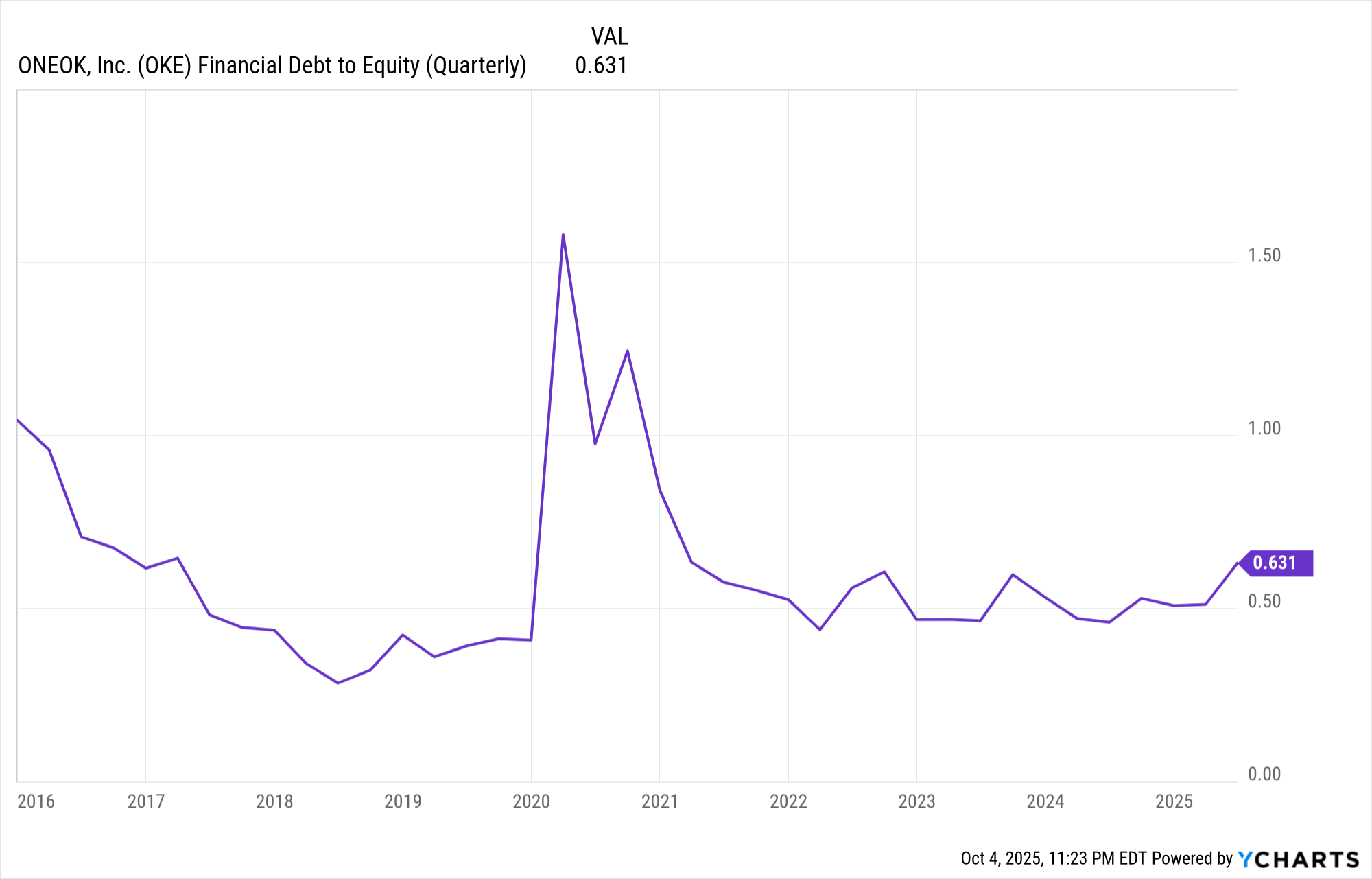

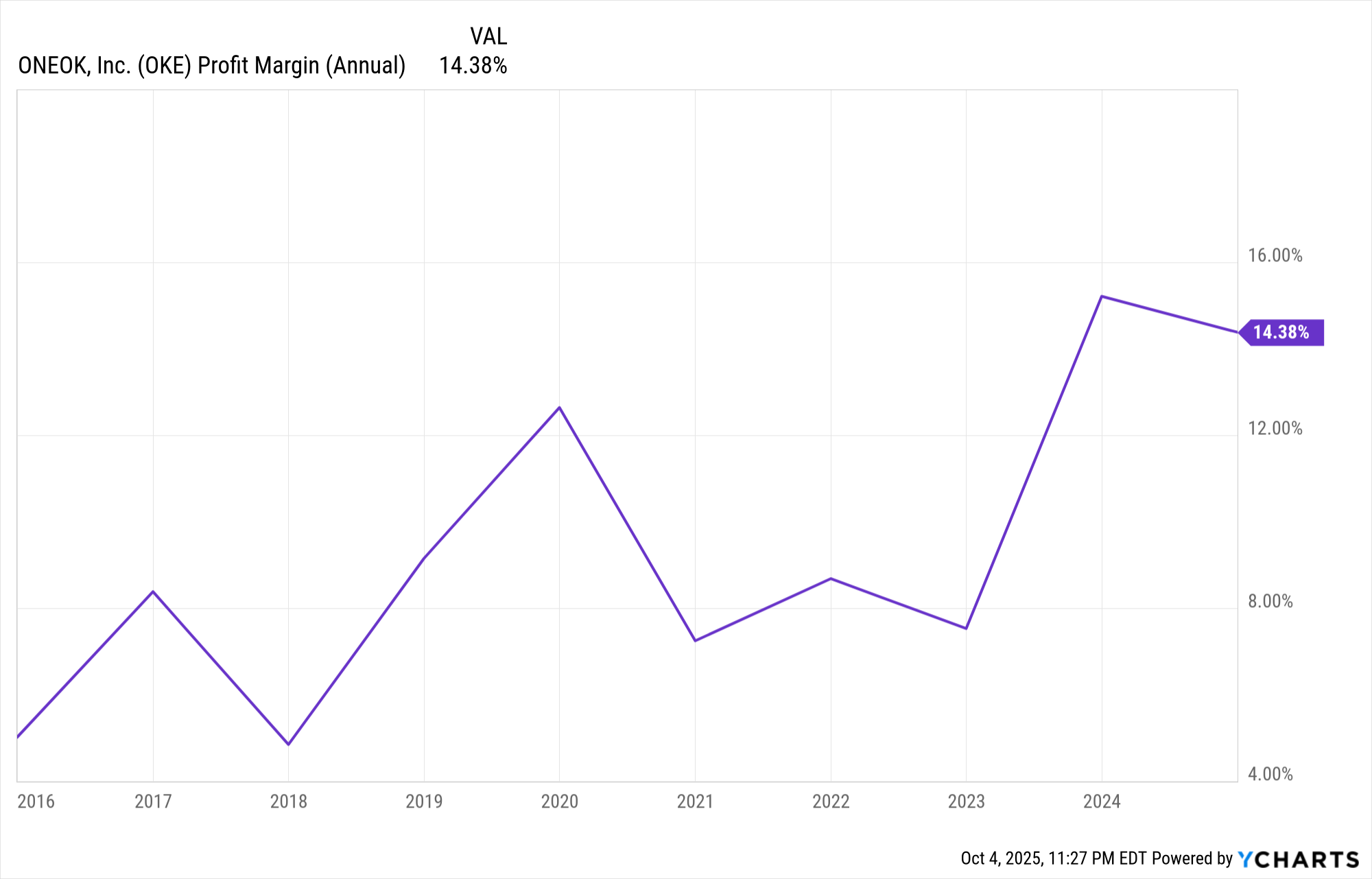

Running through these charts, there’s a long history of the dividend increasing, which is music to my ears. OKE has steadily issued more stock over time, but in keeping with my new perspective on this, as long as the shareholder dilution is effective and delivering value, I’m okay with it. OKE has a long track record of outperformance that satisfies this requirement. For a business in a capital-intensive industry, the amount of free cash flow relative to cash from operations is also quite nice. The last few charts are very strange when considered together: EV to EBIT is 14 (a high number), P/E is 14 (a reasonable number), debt-to-equity is low at 0.6, and profit margin is 14%.

The calculation for EV to EBIT is (market cap + debt - cash) / EBIT. This is what makes these combinations of numbers odd. Market cap is low, debt is low, and there isn’t much cash on hand. Thus, the high EV to EBIT is odd at face value. If market cap is reasonable relative to debt, that shouldn’t be driving up the ratio. But debt-to-equity is low, so that shouldn’t be the culprit either. EBIT is the logical choice—it’s abnormally low and responsible for the high ratio. But that’s a bit contradictory to the notion of a 14% profit margin.

The culprit, as it turns out, is some oddly categorized debt. Total current liabilities are $6.6 billion, and total long-term liabilities are $6.3 billion. This explains the debt-to-equity ratio. Yet total liabilities are $42.62 billion, which is what’s jacking up the EV. Which begs the question: what is all this debt that isn’t categorized in the usual way?

Page 68: I think it’s safe to say their balance sheet doesn’t offer any clean answers.

Page 92: The seemingly missing debt is the commercial paper program. The commercial paper program is odd since that generally refers to very short-term debt, but that isn’t the case here. It includes debt due under a year and debt due in 2064, so the label doesn’t make much sense. My guess is that because it includes both long- and short-term debt, YCharts didn’t have a clean place to put it. But it is actual debt, so it’s on the balance sheet and included in the EV calculation, yet inadvertently excluded from the debt-to-equity ratio since it isn’t listed as either long-term or short-term. Thus, these charts present a very confusing set of data because of an oddity in how OKE records some of its debt. The actual debt-to-equity ratio is 1.9, not 0.6.

After sorting all of this out, the picture is clear: OKE is a profitable business with strong free cash flow and a long history of outperformance. It is, however, a bit debt-heavy and has a history of issuing new stock to raise capital, but it has always been value-added. The debt doesn’t concern me, given the amount of capex needed for the industry OKE operates in. Maintaining a vast network of pipelines and other energy infrastructure requires a lot more money than, let’s say, a software company would have to spend to maintain its property and equipment.

The dividend yield is also about 6% currently, so one is compensated while they wait for the share price to rise once more.

Hamilton Helmer’s 7 Powers:

Scale Economies – Cost per unit decreases as output increases, giving large players a cost advantage (e.g., Amazon, Costco).

I think there’s a scale economy here. OKE has over 60,000 miles of pipeline covering some of the most fossil fuel–rich parts of the United States. Building and maintaining a pipeline network is extremely difficult and expensive. This is 100% a situation where cost per unit decreases with higher volume. It’s also a significant source of moat, especially given the legal opposition to building new pipelines from environmental groups.

Network Economies – The value of a product or service increases as more people use it (e.g., Facebook, Visa).

No, more volume doesn’t make the pipeline better.

Counter-Positioning – A new entrant adopts a superior business model that incumbents can’t easily copy without hurting themselves (e.g., Netflix vs. Blockbuster).

I don’t see how OKE could be counter-positioned against anyone. They are the incumbent in this field.

Switching Costs – Customers face significant costs (time, money, effort, data loss, retraining) to switch providers (e.g., Salesforce, Microsoft Office).

I’m not sure if this applies because I’m not sure many of OKE’s customers have anyone else to switch to. There aren’t many companies with massive pipeline networks.

Branding – Durable consumer trust and preference that allows premium pricing and sustained demand (e.g., Apple, Nike).

I am always skeptical of branding for industrial, business-facing corporations. Reputations do matter, but ultimately we’re talking about fossil fuels, not Rolexes.

Cornered Resource – Exclusive control of a valuable resource or asset others cannot easily obtain (e.g., Pixar’s creative talent early on, or pharmaceutical patents).

Perhaps this could refer to their pipeline network. Aside from the immense cost of building one, there are also regulatory problems. There are some notable examples of environmental lawsuits grinding pipeline construction to a halt.

Process Power – Embedded organizational capabilities and culture that continuously improve operations or product quality, hard for competitors to replicate (e.g., Toyota Production System).

I don’t see how OKE’s facilities and pipelines are more effective than their rivals.

I actually sold my shares in OKE while writing this otherwise positive report. I only held the shares for a few days. I’ve been trying to fix my habit of being as jumpy as I am. It occurred to me that the reason this has been happening is because I’ve been operating outside of my circle of competence. When I don’t feel I fully understand a company, even if on paper it looks great, I hesitate. Although sometimes I do understand the company perfectly, and I just don’t like what I see anymore. In this case, I realized I don’t understand this business well enough to buy in with a lot of conviction. Perhaps you do, I’m sure plenty of people understand midstream energy companies better than I do. So, I thought this was still worth sharing as an idea.

The question anyone should always keep in mind when buying a stock is: what do I know or understand that everyone else doesn’t? I just don’t know enough about midstream energy companies to say that everyone else is wrong and the share price will bounce back soon. It’s interesting how angry many self-proclaimed value investors get on Reddit when this concept is mentioned. For example: Why would someone invest in a pharmaceutical company if they haven’t the slightest idea which drugs in clinical trials hold real promise? Perhaps some extra knowledge of pharmacology or chemistry is called for? Yeah, people don’t like hearing that stuff.

If you have read this far I thought I would throw out some unrelated Easter Eggs.

Easter Eggs:

The value of Berkshire’s stock portfolio is less than its cash and short-term investments. Berkshire has about $295 billion in stocks and $344 billion in cash and short-term investments. Interesting isn’t it? Berkshire is awfully light on stocks right now.

https://www.cnbc.com/berkshire-hathaway-portfolio/

Also, this is what the S&P 500 looked like running up to the dot com bubble:

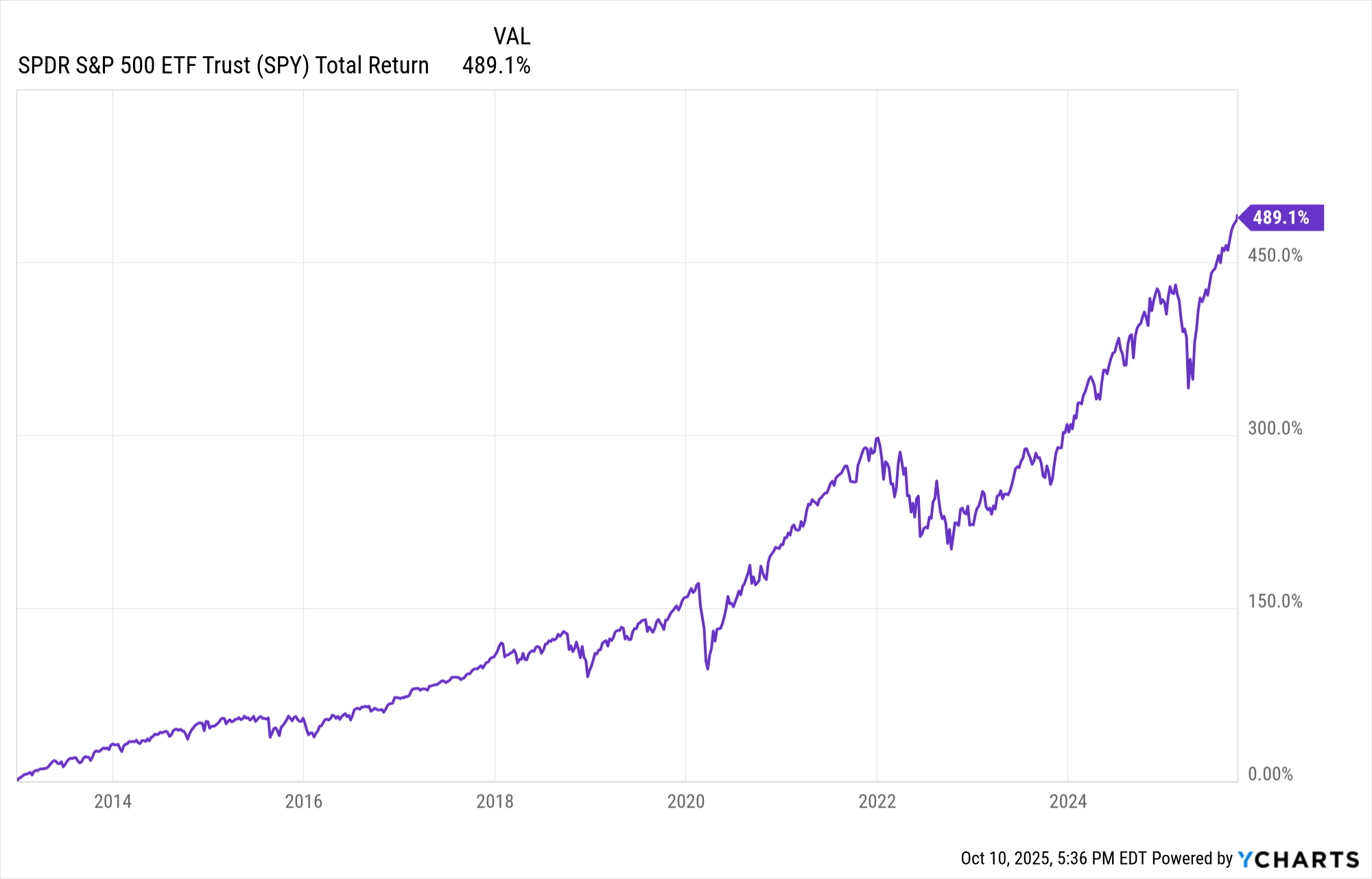

What it has looked like since 2013:

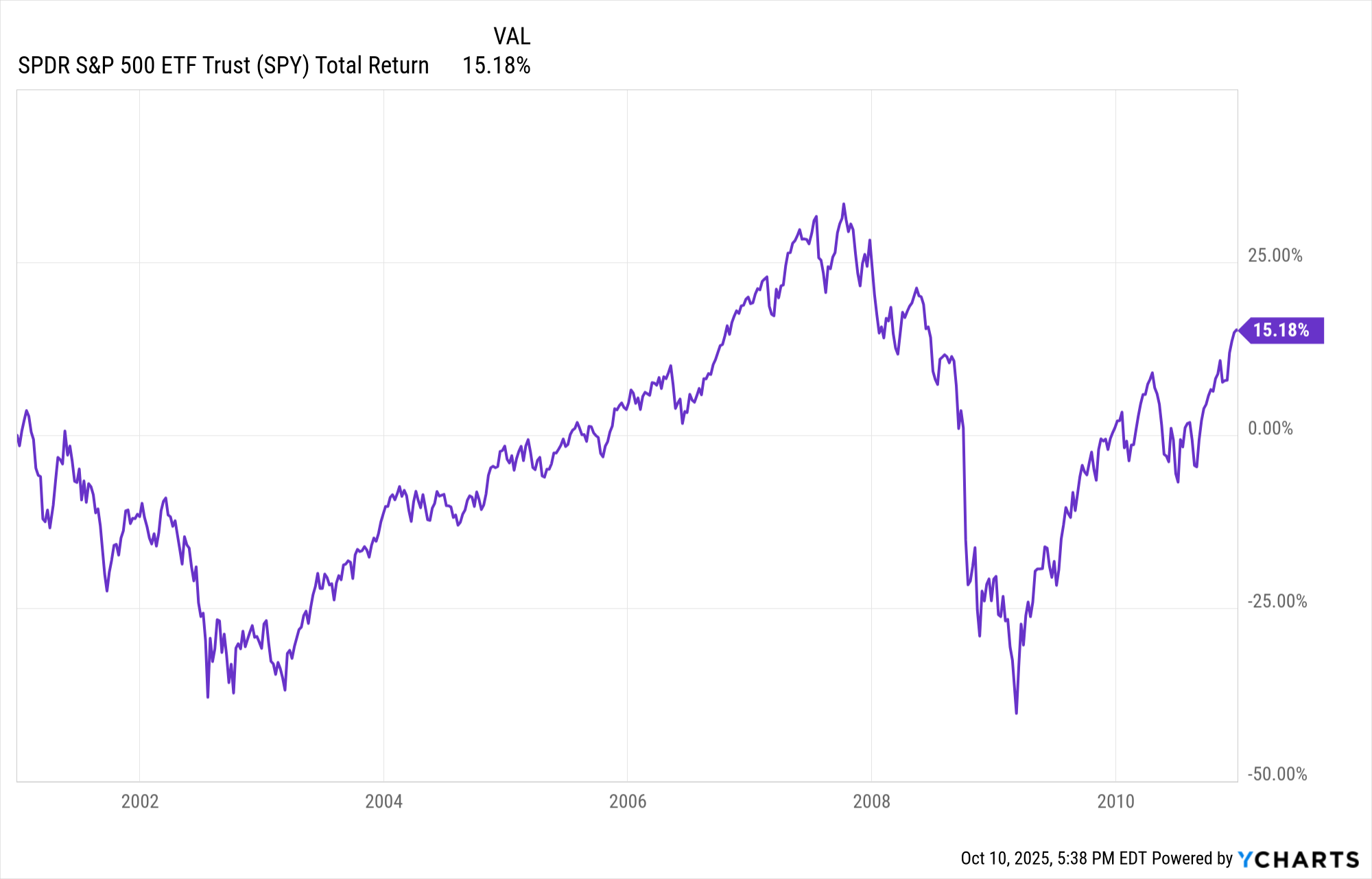

This is from the end of the Dot Com Bubble to just before the start of the current bull market, just to challenge the “stocks only go up” thinking:

Stocks traded sideways for nine years after the Dot Com Bubble popped.

Some of the growing stock market bubble chatter:

https://www.cnbc.com/2025/09/23/fed-powell-stock-prices-appear-fairly-highly-valued.html

https://www.cnn.com/2025/10/09/investing/us-stock-market-ai-bubble-concerns

https://finance.yahoo.com/news/theres-bubble-forming-stock-market-091500806.html

I’ve thought the market has been overheated for a long time. It has taken multiple dives since 2019, but it has always bounced back like a rubber ball. Now, however, the idea that there is danger on the horizon seems to be gaining traction. Will there be a sudden pop? I hope so, since that’s always profitable for me. It could also be a slow burn, since so much growth is already priced in, we might see stock market stagnation for the next decade. That would probably drive people insane in a way that a sudden, drastic crash would not. As usual, I think the end is nigh and won’t shut up about it.

Before I forget, I have yet to reinvest the money from selling off the OKE stock. I currently have a list of 350 stocks that are within my circle of competence, and I’m digging through them one by one.

I’ve been a little slow to write these, I had a marathon in September. I have another one coming up soon and then a 100 kilometer race the spring. Basically, I read shit about stocks and run, that is what I do for fun.

Okay, bye bye now.

My Portfolio:

MITSY, JPM, COF, VICI, PFBC

Wells Fargo bond CUSIP: 94974BGU8

Ford bonds CUSIP: 345370BS8, 34540TN57

*I think it is worth stating that just because I hold a stock doesn’t mean I think it’s a good idea to buy it right now. Also, this only includes the stocks I own.

*Disclaimer*

You can and will lose money in the stock market. You can lose all of your money. I can and will be wrong. I have been wrong in the past. I have lost money in the past. Investing in stocks is risky and should never be considered safe. Invest at your own risk.