JPMorgan Chase & Co. (JPM)

Perhaps the widest moat.

While I’m sitting here, fingers crossed that the market meltdown continues, I have taken small bites at Meta and now JPMorgan Chase (JPM). But here’s the sticking point—JPM’s 2024 10-K is 436 pages long.

I was a JPM shareholder for a while before, but I sold a while back. I never wrote about it because the task of boiling all that information down into a concise post is daunting—and that’s not even counting their earnings calls and investor presentations. But that is my current task.

In the meantime, I can share information on JPM with charts.

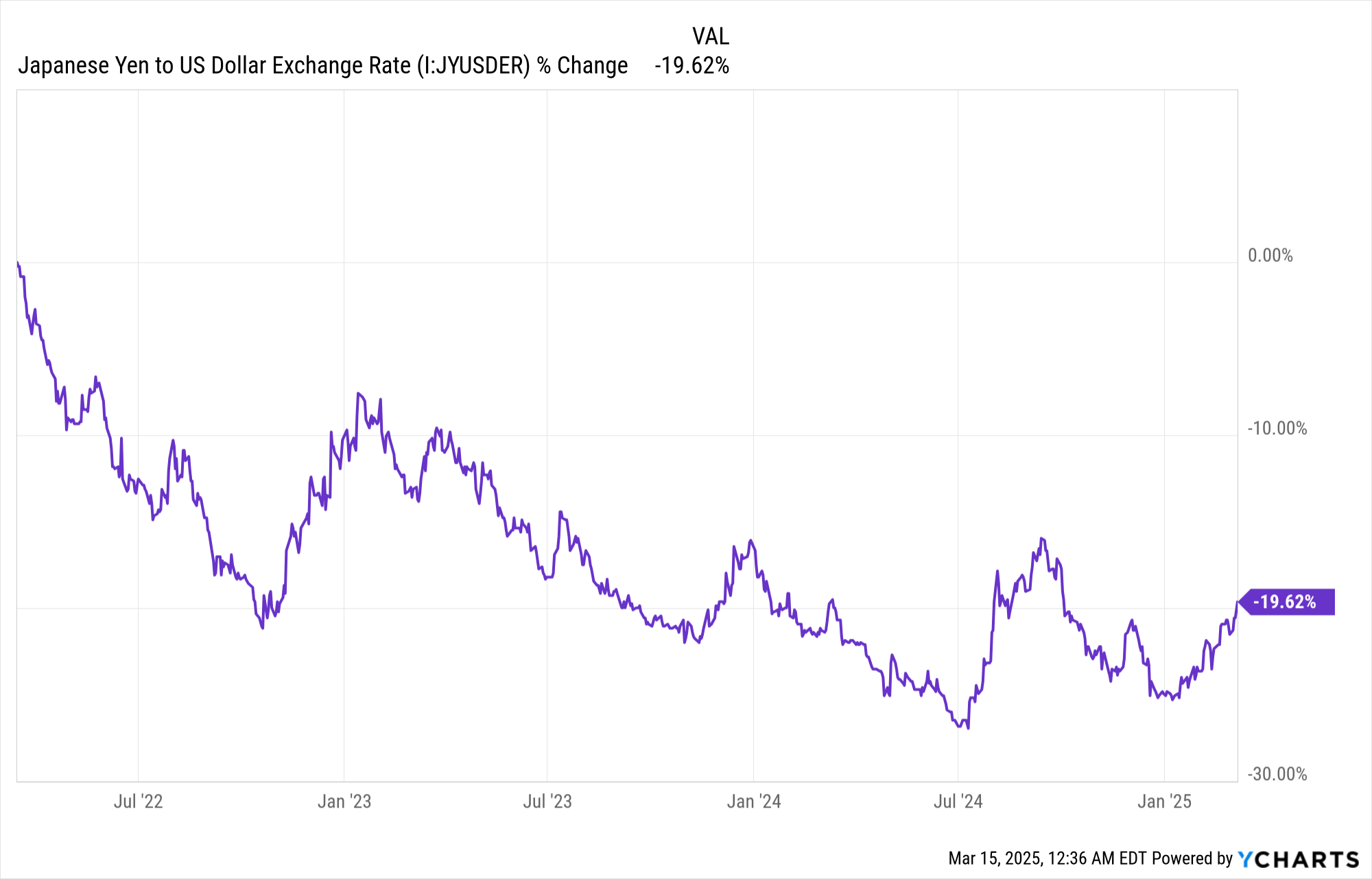

Also, it’s worth an honorable mention that the yen is rising against the dollar, although it’s still down 19.62% over the last three years:

For someone who has a chunk of money in Japan this is great news. Hopefully the trend continues. Aflac does about 70% of their business in Japan and Mitsui is a Japanese Trading Company.

Now onto JPM:

Negative correlation is not causation but it certainly is awesome that JPM has bought back 24.7% of their common stock in the last ten years.

Normally, I show cash from operations and free cash flow, but those metrics are misleading for banks. A significant part of a bank’s business is lending money, which means cash is constantly leaving the institution. However, for a bank, this is a positive sign, whereas for most businesses, negative cash flow is a red flag. For banks, negative cash flow indicates strong loan origination—a sign of a healthy business.

Debt and assets also work differently for banks since customer deposits count as liabilities. Deposits are considered liabilities because they are technically money the bank owes to depositors. However, unlike a traditional loan, little to no interest is paid on most deposits, and there isn't a fixed due date as there is with a typical debt obligation. In essence, deposits function as an interest-free loan to banks. The exception is certificates of deposit (CDs), which pay interest, though the rates are generally low compared to what banks earn on loans.

JPMorgan Chase holds $2.4 trillion in total deposits, yet it only has $866 billion in cash and short-term equivalents. This is why bank runs—when depositors panic and try to withdraw their cash all at once—can be catastrophic. At any given moment, banks do not have enough cash on hand to cover all deposits simultaneously. If a bank collapses, credit cards may stop working, people could permanently lose their savings if in excess of the $250,000 insured by the FDIC, and borrowers might suddenly be unsure where to send their loan payments—at least until another institution acquires the loans.

I’m not sure why I went on the tangent about bank runs… However, I mention all of this because it highlights what makes banking so lucrative. Banks receive deposits at little to no cost, then use them to originate loans—creating a snowball effect that fuels their profitability.

Banks are a unique beast. Cash flow has a different meaning, and a massive amount of liabilities can actually be a very good thing. I’ll save further specifics for the full report.

JPM vs. S&P 500 as far back as I have data:

JPM vs. S&P 500 last ten years:

JPM vs. S&P 500 last five years:

JPM vs. S&P 500 last three years:

JPM vs. S&P 500 last 12 months:

Banks issue credit cards and originate loans, and rising income from collecting interest is a sign of a healthy business.

As I said in the beginning, the 10-K for JPM alone is 436 pages. Oh yes, I have read it before, and I am reading it again now so I can write about it. But the market is moving very rapidly right now, and I wanted to share some information on JPM.

I keep saying it because it’s true—the thought of conveying everything that JPM does is daunting. But I would rate JPM as a safe investment in the sense that it is a massive juggernaut and a cornerstone of the financial system.

During the Global Financial Crisis, the federal government turned to JPM to save the day. The collapse of Washington Mutual remains the largest bank failure in American history. And who stepped up to buy out Washington Mutual? That’s right—JPM. They also acquired Bear Stearns when it collapsed. CEO Jamie Dimon later stated that JPM took on these deals largely due to government pressure and in the interest of financial stability. When I say cornerstone of the financial system, I mean it. I can’t imagine how they could ever be displaced.

All of my bullish statements aside, the future is uncertain, and when Washington Mutual failed, it certainly caught people by surprise. But I have high conviction in JPM as a winning investment when purchased at an attractive price. One final point, here is a video explaining what banks were doing that caused the global financial crisis. JPM had the wisdom not to engage in this nonsense:

Happy hunting.

My Portfolio:

MCD, MITSY, AFL, META, JPM

METC $17 Call 6/20/2025

FedEx Bond CUSIP: 313309AP1

43% of my portfolio is cash right now.

*Disclaimer*

You can and will lose money in the stock market. You can lose all of your money. I can and will be wrong. I have been wrong in the past. I have lost money in the past. Investing in stocks is risky and should never be considered safe. Invest at your own risk.