Capital One Financial Corp (COF)

Big news

American Express (AXP) has a competitor in a way that has never existed before. The Capital One (COF) acquisition of Discover Financial Services is creating a new massive force to be reckoned with. This is, quite frankly, a huge development, and it is a bit surprising that it isn’t being discussed more in the investment community. I’m not going to assume that everyone is intimately familiar with how corporations, banks, and payment processing networks all merge together to create rewards credit cards. If you are aware of how all of this works, then most of what I’m about to say will be repetitive.

Essentially, credit cards are an extortion scheme against the merchant. Example: You have a rewards credit card for your favorite airline that gets you free frequent flier miles when you use the card. In this situation, there is you, the cardholder. Then there is the issuing bank that you got the credit card from. Then there is the credit card network that processes the payment, and finally, of course, the corporation, which in this case is your favorite airline.

The credit card network—Visa, MasterCard, American Express, or Discover—makes money off of the interchange fee. The interchange fee is usually somewhere between 1% and 3% of the transaction. Typically, the merchant is forced to absorb the cost of the interchange fee. The interchange fee goes directly to the issuing bank of the credit card. A small cut of the interchange fee is called the assessment fee which goes to the payment processing network. Another small portion goes to the merchant’s bank, called the acquirer’s fee. Then, of course, there is some degree of profit sharing that exists between the issuing bank and the business with which the rewards card is associated.

This is where the money for credit card rewards comes from. The issuing bank is essentially giving you part of the interchange fee. It’s not entirely inaccurate to say that credit cards are sort of like an extortion scheme against the merchant by the customer, the issuing bank, and the corporation associated with the rewards card. If you never use a credit card, ironically, you’re paying higher prices because of those that do use credit cards except that your not getting anything out of it. Since merchants respond to this interchange fee by raising the cost of the goods and services they provide.

What makes American Express and Discover unique is that they are both the payment processing network and the issuing bank. Visa and MasterCard are only payment processing networks. American Express is able to leverage its brand and extract a higher interchange fee from merchants. This is because American Express has done a good job getting high-net-worth people to use their credit cards. Thus, businesses will accept the higher interchange fee in expectation that American Express cardholders are big spenders.

Discover has not pursued the same strategy as American Express. Discover has typically aimed for wide acceptance as opposed to high fees. In that sense, Discover is a bit more like Visa and MasterCard than American Express. If you have an American Express card, you might have to ask if the merchant accepts American Express, whereas I have never gone to a business and been told they don’t accept Visa. Discover falls somewhere between American Express and Visa at least in the United States.

Now getting into what has me so excited about the acquisition of Discover. Unlike Discover, Capital One is a direct competitor with American Express. Capital One offers auto loans, checking and savings accounts, and the high-fee, perk-loaded type of credit cards that American Express is famous for. The American Express Platinum Card and the Capital One Venture X card are direct competitors. Now, when you consider that many of the perks that come with credit cards are a function of the issuing bank returning part of the interchange fee to you. A business like American Express commands a higher interchange fee and gets to keep more of it being the network and the issuing bank.

Capital One has now become an issuing bank and a credit card network. Thus, their ability to compete with American Express has just greatly increased. I don’t know if Capital One plans on acting like American Express, accepting the trade-off of narrower network acceptance but gaining a higher interchange fee, or if Capital One will stick with the mass appeal approach. Based on the most recent earnings call its sounds like Capital One is seeking mass appeal. Either way, Capital One has just gained a sizable chunk of a very wide-moat industry. They will become more profitable and have an easier time stealing market share from their competitors.

It is also important to consider how hard it is to create a credit/debit card processing network. Think about the intense degree of network stability and security that is required. If a cyberattack ever took down Visa’s network, tens of millions of people in the United States would suddenly have no access to their money—unless they physically went to a branch location of a bank and withdrew cash. Many ATMs wouldn’t work because, again, they rely on the credit card networks to process and settle transactions. Then there’s the ability to handle surges in demand and have 100% network uptime 24/7/365.

When I refer to surges in demand, you’ll notice that you never swipe a credit or debit card and then have to sit there for 10 minutes waiting for the transaction to process. It’s always instant, no matter the holiday, event, or anything else that could possibly create a huge surge in people swiping their cards. So, there is the challenge of creating such a massive and reliable computer network. Then there is the second challenge of getting merchants to accept your payment network. If Capital One didn’t buy out Discover and instead tried to create its own network from scratch, it would be extremely costly, and the network would be useless until you got nearly all businesses in the country to adopt it. It doesn’t do much good to have a debit card or credit card that is refused by merchants 90% of the time.

I feel like I can’t stress enough what a big deal Capital One’s acquisition of Discover is. I think Capital One just moved from a narrow-moat business to one with a very wide moat. There is also an entirely new line of business that opens up for Capital One now as well. Since Capital One can now help corporations issue their own unique rewards credit cards in a way they couldn’t before.

Now, Capital One is funding this transaction with an all-stock offer. If you have been reading this Substack for a while, you will have heard me say that if corporations dilute my ownership stake, they better have a damn good reason for doing so. In this case, Capital One does have a damn good reason, and I don’t care about the dilution. This was an excellent acquisition, and on top of that, Capital One has a long-established track record of share buybacks. Also, as I will show you in the charts, Capital One has often outperformed American Express even before this acquisition happened.

To perhaps sum all of that up succinctly:

American Express and Capital One compete for customers.

American Express is fairly unique given that they are the issuing bank, the payment processing network, and offer customers a premium experience.

Capital One is now an issuing bank and a payment processing network that also offers customers a premium experience.

This business model is extremely difficult to duplicate from scratch and is inherently wide moat.

Capital One vs. American Express vs. S&P 500 as far back as I have data:

Capital One vs. American Express vs. S&P 500 over the last ten years:

Capital One vs. American Express vs. S&P 500 over the last five years:

Capital One vs. American Express vs. S&P 500 over the last three years:

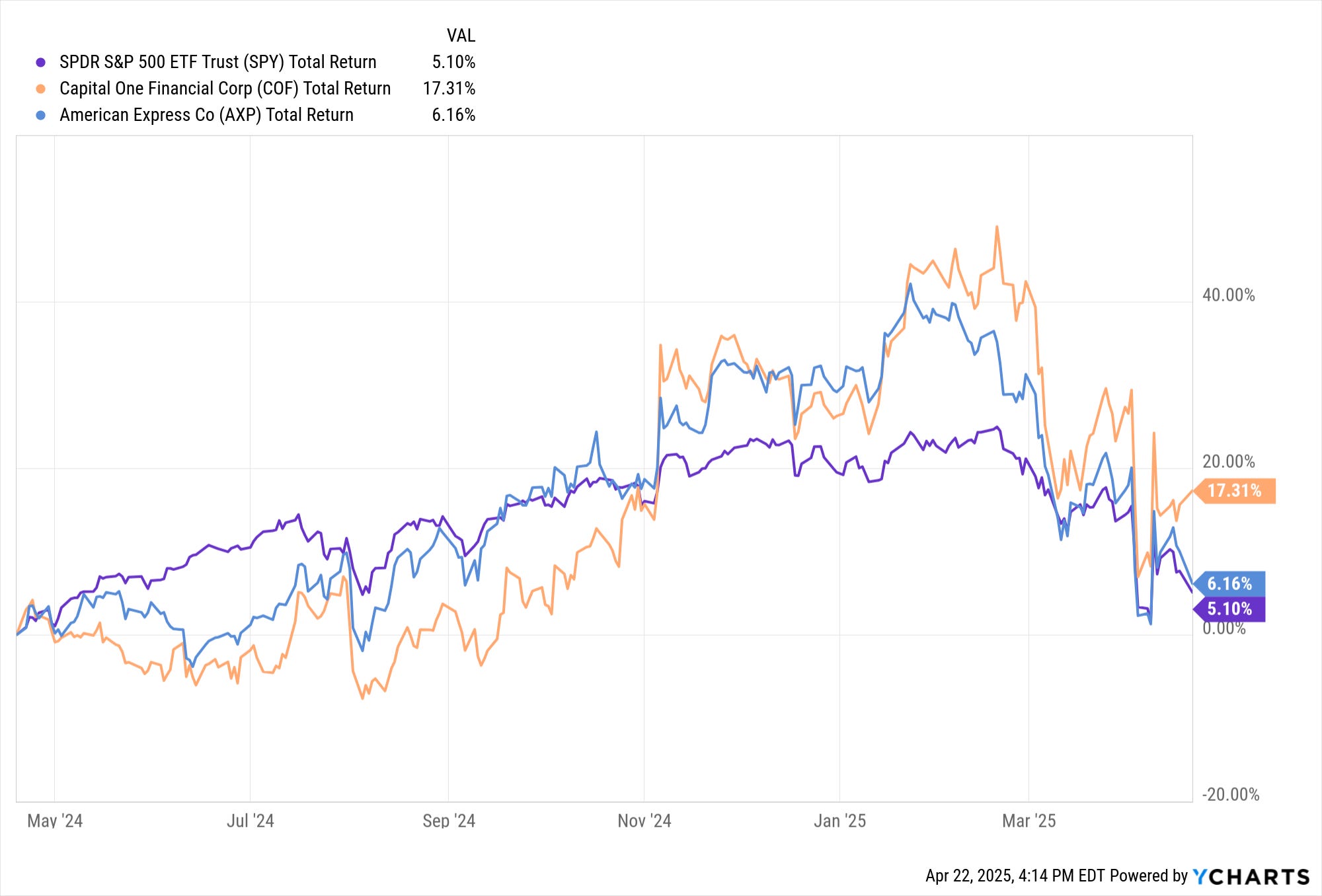

Capital One vs. American Express vs. S&P 500 over the last 12 months:

As you can see, Capital One, up until this point, has performed well against the S&P 500 and American Express prior to the acquisition of Discover.

I’m not going to do a deep dive into Capital One’s most recent 10-K because, with the acquisition of Discover, we are now looking at a business that is substantially different. However, I will go over some key points from Capital One’s most recent earnings release.

2025 Q1 earnings call transcript

I often hear people make uninformed remarks to the effect of, "Owning financial stocks is bad because in tough economic times people won’t pay their credit cards."

If you have ever read the financial reports of a bank, you know how absurd this fear is. Capital One has a total of $16.26 billion set aside to cover credit losses. Focusing on credit cards specifically, there were $2.4 billion in net charge-offs, with a total of $12.9 billion set aside to cover losses. There would have to be more than a 500% increase in net charge-offs from credit cards for Capital One to max out its allowance for credit losses. Even then, it doesn’t mean the bank fails. It would simply mean that Capital One would need to use liquidity from outside the provision for credit losses to cover it. A 500% increase in credit card defaults is fairly unprecedented. You would probably have to go all the way back to the Great Depression to find an economic collapse on that kind of scale. My guess would be that if credit card defaults jumped by 500% in a year, your stock portfolio taking a hit would be the least of your concerns. As the country would likely be in some kind of economic meltdown.

This is an important point I want to make. Capital One does a variety of things aside from issuing credit cards, which is what they are best known for. Their slogan, "What’s in your wallet?" specifically refers to their credit card business. Capital One earned $1.22 billion in the first quarter of 2025 from credit cards alone. That is 86% of their total earnings. Prior to the acquisition of Discover, Capital One was very much a credit card company.

Now, all of this has changed. As previously stated, Capital One now owns a credit card network. No longer are they merely the issuing bank. This creates an entirely new source of income for the business, as well as strengthening their position as an issuing bank. It is an absolute game changer for this business. When considering the performance charts above, that is how well Capital One was doing before the Discover acquisition. My view is that Capital One is going to do even better from this point forward.

There’s a lot to like here: a high amount of free cash flow and a long history of share buybacks. The buybacks have slowed in the last few years, and the acquisition of Discover was funded by issuing new stock. Discover shareholders will receive 1.0192 Capital One shares for each Discover share they own. After the deal, Capital One shareholders will own 60% and Discover shareholders 40% of the combined company. I am confident that after the dust settles, Capital One will resume its habit of buying back shares. The Discover acquisition is set to close on May 18.

Quote from the transcript of the most recent earnings call:

Richard Fairbank, Chairman and Chief Executive Officer, Capital One: Yeah. So, it’s a real blessing to have the opportunity in this acquisition to bring on board a company with a rare, well recognized, very strong brand. And so, we now have two companies with very strong brands. So, what we plan to do is we plan to continue, of course I shouldn’t say of course because all of this you know, we’ve done a lot of thinking about, but we are very strong in our views that the Discover brand is absolutely the right brand for the network and we will continue to invest in that brand and especially build the credibility and the capabilities globally with respect to the brand. We will also continue the Discover brand on the credit card side.

It will be more of a really powerful product brand. Obviously, it’s not going to be a corporation brand anymore, but we intend to have it as a strong product brand and it goes back to what I think is the collective, you know, the combination of the business model they’ve created that has generated such amazing results over the year, which the brand plays an important role there. So, we will continue to invest in that. Now, are some savings around the edges that we can do in our collective marketing campaigns, I am sure. So, there’s some benefit there.

And I want to make one other comment about investing in the network brand. That is something that we don’t plan to come roaring out of this acquisition on national TV really leaning into the network brand. What we much more plan to do is we believe that the synergies and the whole moves that we have talked about at the time we announced our deal of moving our entire debit business and a portion of our credit card business onto the network, we believe that can be done within the context of the current brand and the acceptance and the capabilities that Discover has built so skillfully. What we need to do in order to generate longer term opportunity is to build the acceptance internationally up to a sort of you know it when you see it point when it’s the right time to lean into brand development of a global brand, a global acceptance brand. So, in terms of the brand spend there, that’s more of a delayed thing.

It is something that we certainly plan to lean into over time, but that would come as we see it today. That would come sort of after we have gotten the international acceptance to a sort of, you know, when you see it point that it’s ready to really take this story on TV.

and

Richard Fairbank, Chairman and Chief Executive Officer, Capital One: Yeah, so, well, I’m glad you asked that question. We aren’t on a quest to replicate Visa and MasterCard’s model. It’s an extraordinary model they have on behalf of really all the banks in The United States, almost all of them. They are the intermediary between all the banks and the merchants. And, of course, they get paid a few basis points here and there times the trillions of dollars of transactions.

It’s an amazing business model. By the way, just with respect to that, it is the case that Discover does have on the debit side, they are a network provider for several thousand banks. So, I don’t want to diminish that particular business model. It’s a great thing. It came from their acquisition in 02/2005 of the Pulse Network and it’s a very nice business model and we would love to grow that.

So, I do think that being a network for other financial institutions would be part of the business model over the years. That, like most other things, the road to significantly change the game there probably again goes through that same path of building greater global network. Acceptance and the brand credibility sort of for the network that goes along with that. But anyway, the biggest opportunity for Capital One beyond the sort of direct opportunity that we identified with the amount of volume that we moved is to be able put more of our volume on the network. And it is our view that as we look to do more of that, we, again, those roads lead to because lots of people, so many of our customers are international travelers.

And again, they did discover for a company of their size, I marvel at what they’ve built globally. Now, The United States, it’s basically accepted everywhere in The United States. Internationally, no one is accepted everywhere, but they’ve gotten a great head start on that. But we believe that in order to really capitalize on the network and to give the network the scale that in this profoundly scale driven business, the scale that would really help it and sort of getting the flywheel of scale in this network effect business, all roads lead through building more international acceptance and then really leaning into the global brand associated with that network. But as we look at it, the primary payoff of that would be just putting more volume on the business in a very scale driven business.

And then, over time, we could also look at other opportunities such as being a network for other financial institutions.

I wanted to hear directly from the horse's mouth what their plan is for the Discover network. Also, perhaps a history lesson about credit card networks is in order. You’ll notice the CEO of Capital One stating that Visa and MasterCard have done amazing things for banks.

Well, it all started with the Fresno Drop in 1958, where Bank of America, unsolicited, mailed out 60,000 credit cards to customers. It is important to note that these were the first-ever general-purpose credit cards. Needless to say, chaos ensued. Merchants had no idea what these cards were, and it led to widespread confusion. However, as Bank of America refined the process, credit cards began to catch on. The reason this worked for Bank of America early on was that they had such a strong presence in California that Bank of America was often the bank for both the customer and the merchant. That made it very easy for Bank of America to handle these transactions since it was all internal.

Now, banks from around the country learned about these new credit cards and wanted to add them into their own businesses. But this created a lot of problems when the customer and the merchant didn’t bank with the same financial institution. This was also occurring prior to the invention of the internet. Let’s say a customer wanted to buy a new refrigerator. The cashier at the appliance store would have to call the bank and verify that the customer had a big enough line of credit to cover the purchase. Then the merchant's bank would have to contact the customer’s bank in order to transfer funds. This becomes a problem when you are handling thousands of transactions. There is this slow process of confirming the customer has the available credit to purchase the item, followed by the complete headache of all these different banks invoicing each other for each individual transaction.

Many banks around the country looked to Bank of America for a solution to this problem, since Bank of America was the creator of the modern credit card and was licensing out its credit system to them. Ultimately, Bank of America wasn’t very helpful. Their BankAmericard program was spun off into a separate business that eventually became what we now know as Visa. That is what Visa, MasterCard, American Express, and Discover do. They handle the very complex process of verifying transactions and moving money between financial institutions. Thus, the credit card network has to have a relationship with the merchant, the customer, the merchant's bank, and the customer's bank.

This is why it is so hard to create a credit card network and why simply possessing one is a huge source of moat. It is also why credit card networks can make money all day on interchange fees. If a bank were to try and cut out Visa, MasterCard, American Express, or Discover, then that bank would have to establish its own relationship with hundreds of thousands of merchants and create its own process for invoicing every other bank that a merchant or a customer could possibly use.

I think this demonstrates the importance of understanding history for an investor. If one doesn’t know all of this and how the current system came to be, then it might be hard to understand how these credit card networks are so profitable and so well entrenched against new competitors. Capital One just added this into their already very profitable credit card and banking business.

Hamilton Helmer’s 7 Powers:

Scale Economies – Cost advantages gained as production increases, making it hard for smaller competitors to match pricing or margins.

Capital One isn’t producing anything in the traditional sense. So, no.

Network Economies – Increased value of a product or service as more people use it (e.g., social networks, marketplaces).

100%, with the acquisition of Discover, which operates a payment processing network, its impossible to say there isn’t a network effect.

Counter-Positioning – A newcomer adopts a superior business model that incumbents can’t replicate without self-damage.

I think this one depends on what Capital One ends up pursuing as their strategy. My opinion is that their business has more in common with American Express than with Visa or JPMorgan Chase. Capital One has stated that they are going to maintain the Discover brand. That does give them a unique opportunity to target two different types of consumers with their two different brands.

Switching Costs – Friction or loss a customer experiences when changing from one product/service to another, locking them in.

I don’t have any data on how common it is for people to cancel credit cards and pick up a new one. I will say that it is certainly inconvenient to do so. There is some degree of stickiness with credit card holders, but it is debatable how large that effect is.

Branding – Perception-based value created by customer affinity and trust, often through repeated high-quality experiences.

This is another maybe. Capital One certainly has name recognition. A lot of people have heard the phrase "What’s in your wallet?" But what the association is with the brand, I can’t say. I would be comfortable stating that American Express has a strong brand, but I think it’s debatable for Capital One.

Cornered Resource – Exclusive access to a valuable asset or talent (e.g., IP, talent, or favorable contracts) that others can’t replicate.

No.

Process Power – Unique internal processes developed over time that lead to superior execution and can’t be easily copied.

No.

Capital One is a wide moat business that is extremely well positioned to snatch market share from its competitors.

Okay, Bye bye now.

My Portfolio:

MCD, MITSY, AFL, META, JPM, MGM, SPG, COF

METC $17 Call 6/20/2025

*I think it is worth stating that just because I hold a stock doesn’t mean I think it’s a good idea to buy it right now.

*Disclaimer*

You can and will lose money in the stock market. You can lose all of your money. I can and will be wrong. I have been wrong in the past. I have lost money in the past. Investing in stocks is risky and should never be considered safe. Invest at your own risk.