Adobe Inc (ADBE)

Imagine that I said something catchy about PDF files.

Adobe’s share price is completely out of step with the reality of what is happening in the company. It’s a bit bizarre—I think it is one of the biggest disconnects I have seen in a long time. As far as I can tell, the disconnect is entirely narrative-driven. The narrative is that AI is ultimately bad for Adobe’s business, no matter how well things are going right now. The irony is that the fear of automation putting people out of work and damaging corporations isn’t new. In fact, it’s a very old fear.

In Robert Shiller’s book Narrative Economics, he documents this exact discussion taking place during the Industrial Revolution. Prior to that era, about 80% of the country worked in agriculture. The rise of labor-saving machines sparked the same fear that AI is generating today—that large numbers of people would be put out of work. Currently, only about 1.5% of people in the United States work in agriculture. Yet the country did not collapse. Instead, people were freed to engage in different kinds of work. I believe today’s pessimism reflects a similar failure of imagination.

But more importantly, how did the companies fare that should have been impacted by this labor shift? One narrative I’ve heard about Adobe’s supposed negative future is that AI will reduce the workforce in graphic design, leading to fewer subscriptions. The same could have been said of John Deere, which was founded in 1837. They created many of the labor-saving machines that led to the drastic reduction in the number of people working in agriculture. Yet John Deere is as profitable as it has ever been. Interesting. Perhaps it’s because farmers are now completely reliant on modern machinery to operate their farms. John Deere may have reduced headcount on farms, but their products have gotten more complex and expensive.

I suspect something similar to what happened to John Deere will happen with AI. If new Adobe AI-enhanced products reduce the number of people working in graphic design who use Photoshop. Then all that will have occurred is that businesses will be even more reliant on Adobe products—giving Adobe greater pricing power. Adobe will create increasingly complex products, creating a virtuous cycle for the company.

Now let me show you how disconnected the financial reality of the company is from how the share price has been moving.

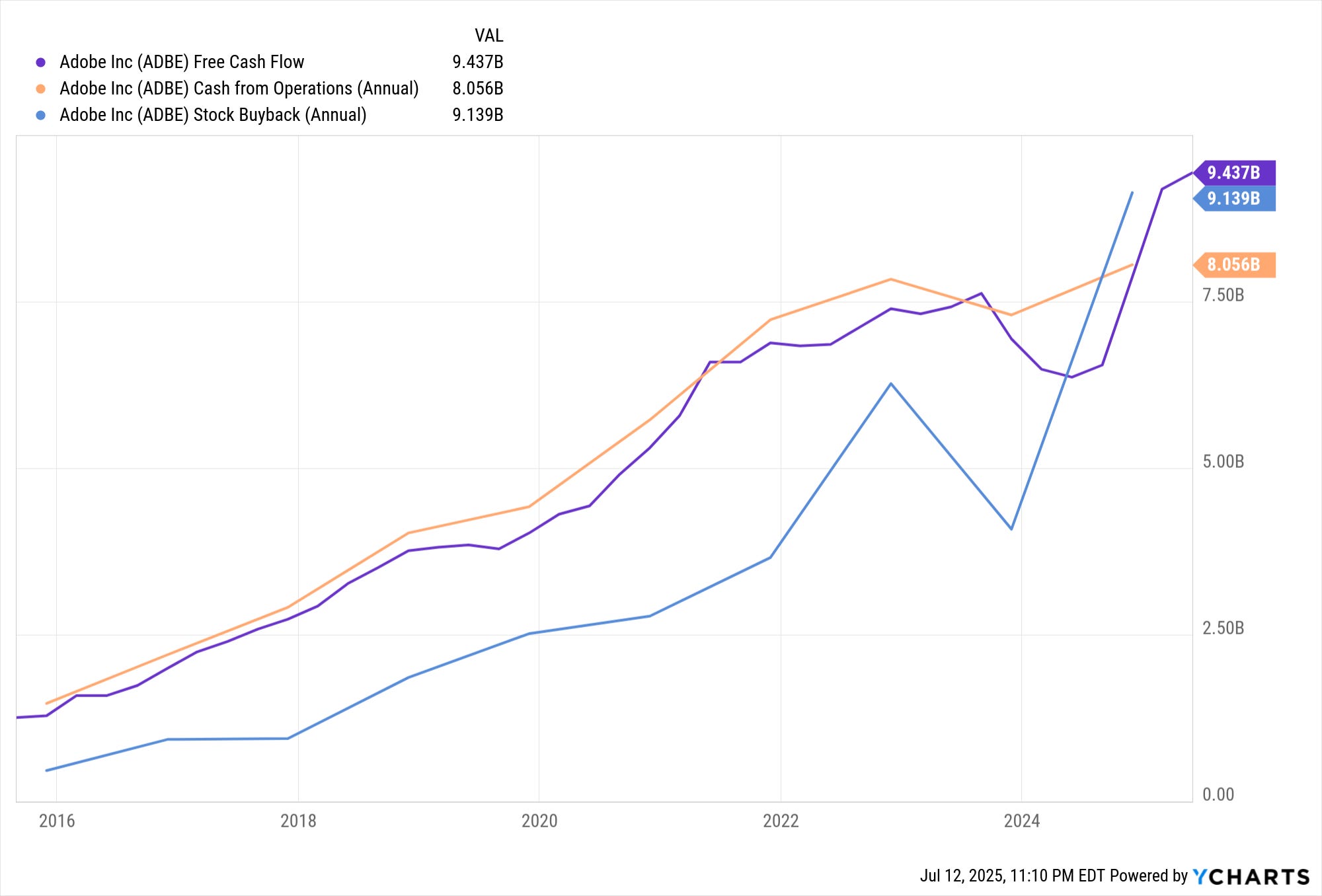

I’ll circle back to all of this again later, but I want to hammer home the point early: the predictions of doom aren’t coming true. Cash flows and revenue are at all-time highs, and Adobe has a strong history of buybacks. One amazing attribute of software companies is the insane amount of free cash flow in relation to their cash from operations.

All that being said, let’s get into what Adobe does as a company.

Adobe has three business segments Digital Media, Digital Experience, Publishing and Advertising.

Digital Media - 74% of total revenue.

Creative Cloud

Adobe Creative Cloud is a subscription-based suite of professional creative applications and services used for design, photography, video, web development, and more.

As of this writing Creative Cloud subscribers get access to all of Adobe’s programs. In addition to 100 GB of cloud storage as well as other perks. All of this for the price of $104.99 a month.

Photoshop

Adobe Photoshop is a powerful piece of software used to enhance, manipulate, and create images. It's widely used by photographers, designers, and artists to retouch photos, create graphics, design layouts, and produce digital art. Even though it's used professionally, many hobbyists and casual users also use it to improve personal photos or create custom visuals for social media. I want to emphasis that last point, that Adobe Photoshop is the industry standard in graphic design

Illustrator

Adobe Illustrator is used to create drawings, logos, and graphics—but instead of using pixels like a photo, it builds images out of lines and shapes called vectors. This means the artwork can be resized to any size without losing quality. This difference between vectors and pixels sounds very subtle, at least to me, as someone who doesn’t work in graphic design. But it is a very important distinction between Photoshop and Illustrator, these are not interchangeable products. Illustrator is also the industry standard.

Lightroom

Adobe Lightroom is a photo editing and organization program designed specifically for photographers. Unlike Photoshop, which is used for deep image manipulation, Lightroom focuses on adjusting things like exposure, color, contrast, and sharpness to improve the overall look of a photo. It also helps users organize thousands of images with tools for sorting, tagging, rating, and creating albums. Lightroom is particularly popular with professional and amateur photographers because it offers powerful editing tools in a faster, more streamlined workflow, allowing photographers to edit entire batches of photos efficiently while keeping the originals intact. Yes, you guessed it, Lightroom is another industry leading piece of softare.

Premiere Pro

Adobe Premiere Pro is a professional video editing program used to cut, arrange, and enhance video clips. It lets you import footage, trim scenes, add transitions, adjust colors, mix audio, insert titles, and export polished videos for platforms like YouTube, film, TV, or social media. It supports everything from simple edits to complex, multi-camera projects. Premiere Pro is popular among filmmakers, content creators, and video editors because it offers powerful tools, high-quality output, and seamless integration with other Adobe apps like After Effects and Photoshop. Premiere Pro does have competition from Final Cut Pro which is exclusive to Mac, and DeVinci Resolve.

Acrobat

Adobe created the PDF (Portable Document Format) in 1993. It was developed as a way to share documents reliably across different computers, operating systems, and software—ensuring that formatting, fonts, and layouts would stay consistent no matter where or how the file was viewed.

PDF quickly became a universal standard for digital documents, and in 2008, Adobe handed over control of the PDF specification to the International Organization for Standardization, where it is now maintained as an open standard. Despite that, Adobe Acrobat remains the most well-known and widely used PDF software.

Express

Adobe Express is a simplified, user-friendly design tool that lets you create social media posts, flyers, logos, videos, and more—even if you have no design experience. It’s a web- and mobile-based app that provides easy drag-and-drop controls, customizable templates, royalty-free Adobe Stock assets, and AI-powered features like text-to-image and background removal. Unlike Photoshop or Illustrator, which are geared toward professionals, Adobe Express is designed for quick, polished content creation by students, marketers, small business owners, and anyone who needs eye-catching visuals fast. It's part of the Adobe ecosystem but much easier to learn and use.

Firefly

Adobe Firefly is Adobe’s suite of generative AI tools designed to help users create images, text effects, and other visual content using simple text prompts. It’s integrated into Adobe products like Photoshop, Illustrator, and Express, and allows users to do things like generate backgrounds, fill in or remove parts of an image, create stylized text, and transform ideas into visuals—all with AI assistance.

Unlike some other AI tools, Firefly is trained on Adobe Stock and public domain content to ensure commercial safety, meaning the results can legally be used in professional work. It’s aimed at both designers and non-designers, making it easy to create high-quality visuals without needing deep technical skills.

Digital Experience - 25% of total revenue.

Experience Platform

Adobe Experience Platform is a powerful enterprise tool that helps businesses collect, unify, and analyze customer data to deliver personalized experiences in real time. It brings together data from multiple sources—like websites, mobile apps, CRM systems, and in-store transactions—into a single, real-time customer profile. This unified data allows companies to better understand their customers and target them with relevant, timely content across different channels. The platform also integrates with Adobe’s AI technology, Adobe Sensei, to automate insights, audience segmentation, and predictive analytics. As the core of Adobe’s Experience Cloud, it supports tools like Adobe Journey Optimizer and Adobe Real-Time CDP, enabling businesses to create consistent, personalized digital experiences at scale.

Gen Studio

Adobe GenStudio is a new, AI-powered content creation and marketing platform designed for large brands and enterprises. It streamlines the process of planning, creating, adapting, and delivering content at scale by combining generative AI tools (like Adobe Firefly) with Adobe’s marketing and data technologies.

GenStudio helps teams quickly generate branded content—such as social posts, ads, and videos—tailored to different audiences, channels, and markets. It integrates with tools like Adobe Express and Experience Manager, allowing users to create assets with AI, personalize them using real-time customer data from Adobe Experience Platform, and distribute them efficiently across digital platforms. GenStudio is meant to solve the growing demand for content by making it faster, more automated, and more consistent with brand standards.

Publishing and Advertising

According to the 10-K, pages 42 and 43, this business segment accounts for about 1% of revenue. As such, I’m not spending time discussing it in detail. Additionally, revenue for this segment is declining.

This is not intended to be an exhaustive list of all Adobe products.

Here is a few points of interest in the 2024 10-K:

Page 41, 95% of revenue comes from subscriptions.

Page 45, 18% of total revenue goes towards R&D.

Page 50:

“In March 2024, our Board of Directors granted additional authority to repurchase up to $25 billion in our common stock through March 14, 2028.”

“During fiscal 2024, we entered into accelerated share repurchase agreements (“ASRs”) with large financial institutions whereupon we provided them with prepayments totaling $9.5 billion. Subsequent to November 29, 2024, as part of the March 2024 stock repurchase authority, we entered into stock repurchase arrangements with a large financial institution which totaled $3.25 billion, including a $2.75 billion ASR and a trading plan under which we may execute up to $500 million in open market repurchases.”

Now for the charts:

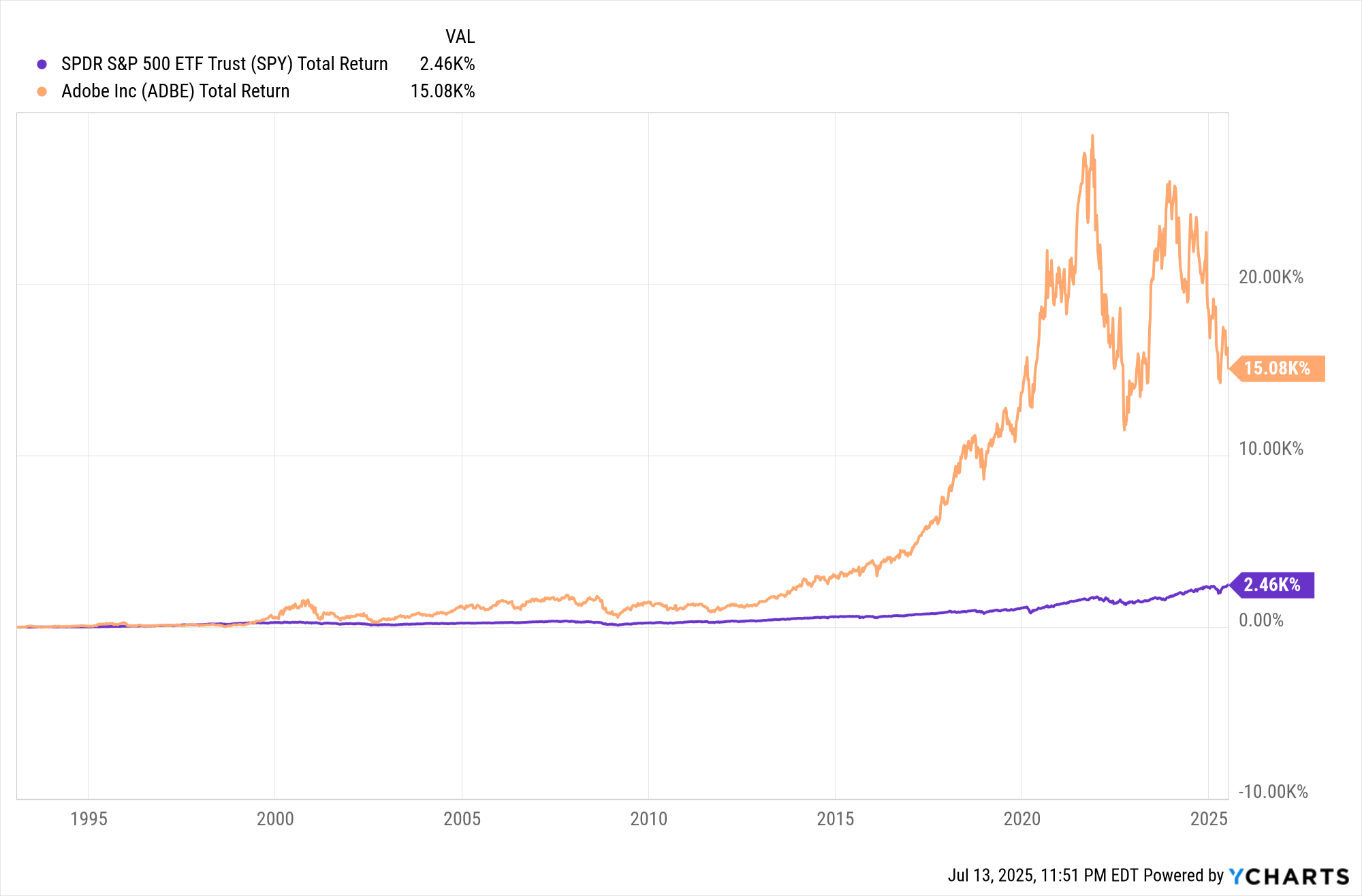

Adobe vs. S&P 500 as far back as I have data:

Adobe vs. S&P 500 over the last ten years:

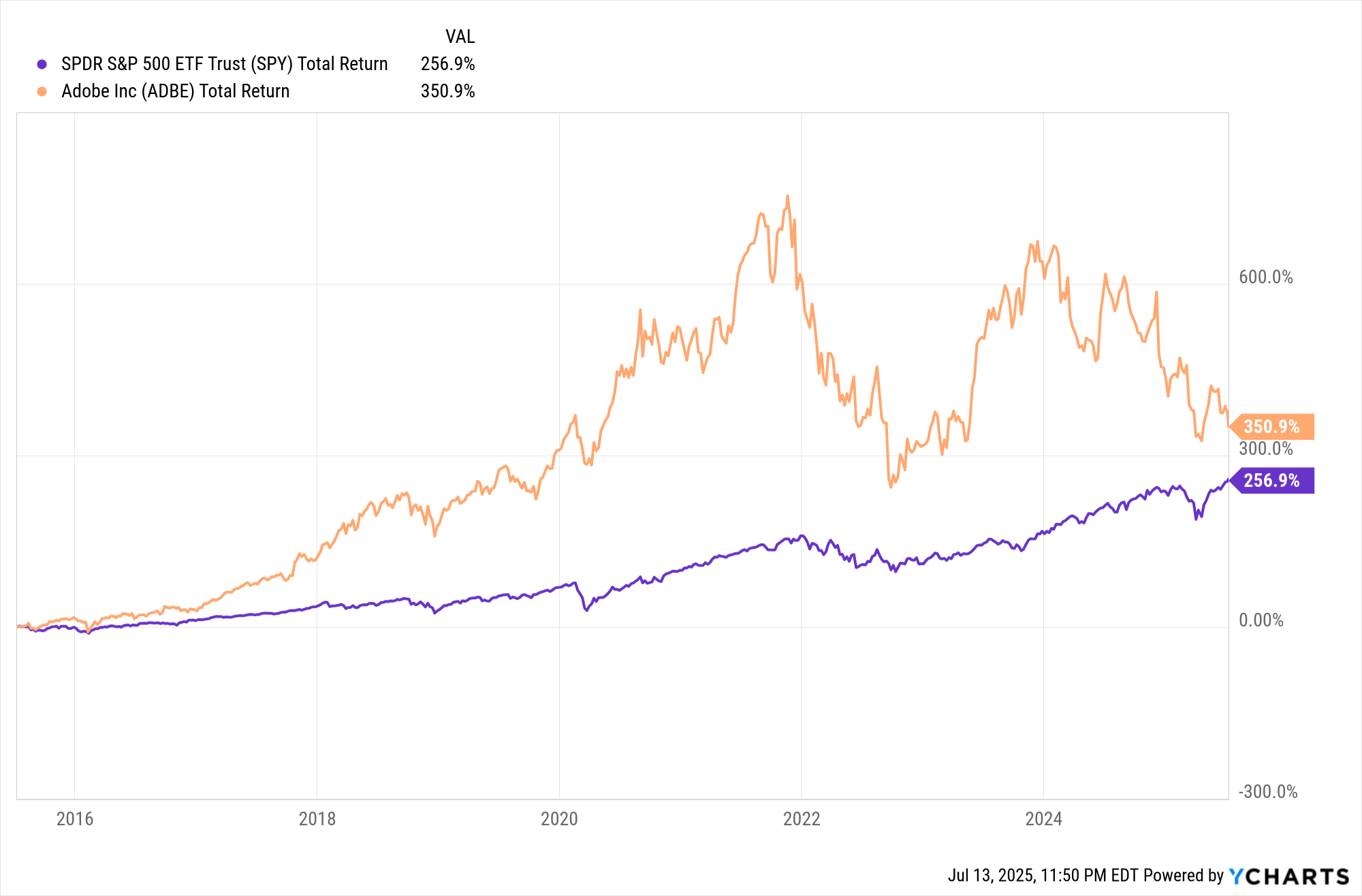

Adobe vs. S&P 500 over the last five years:

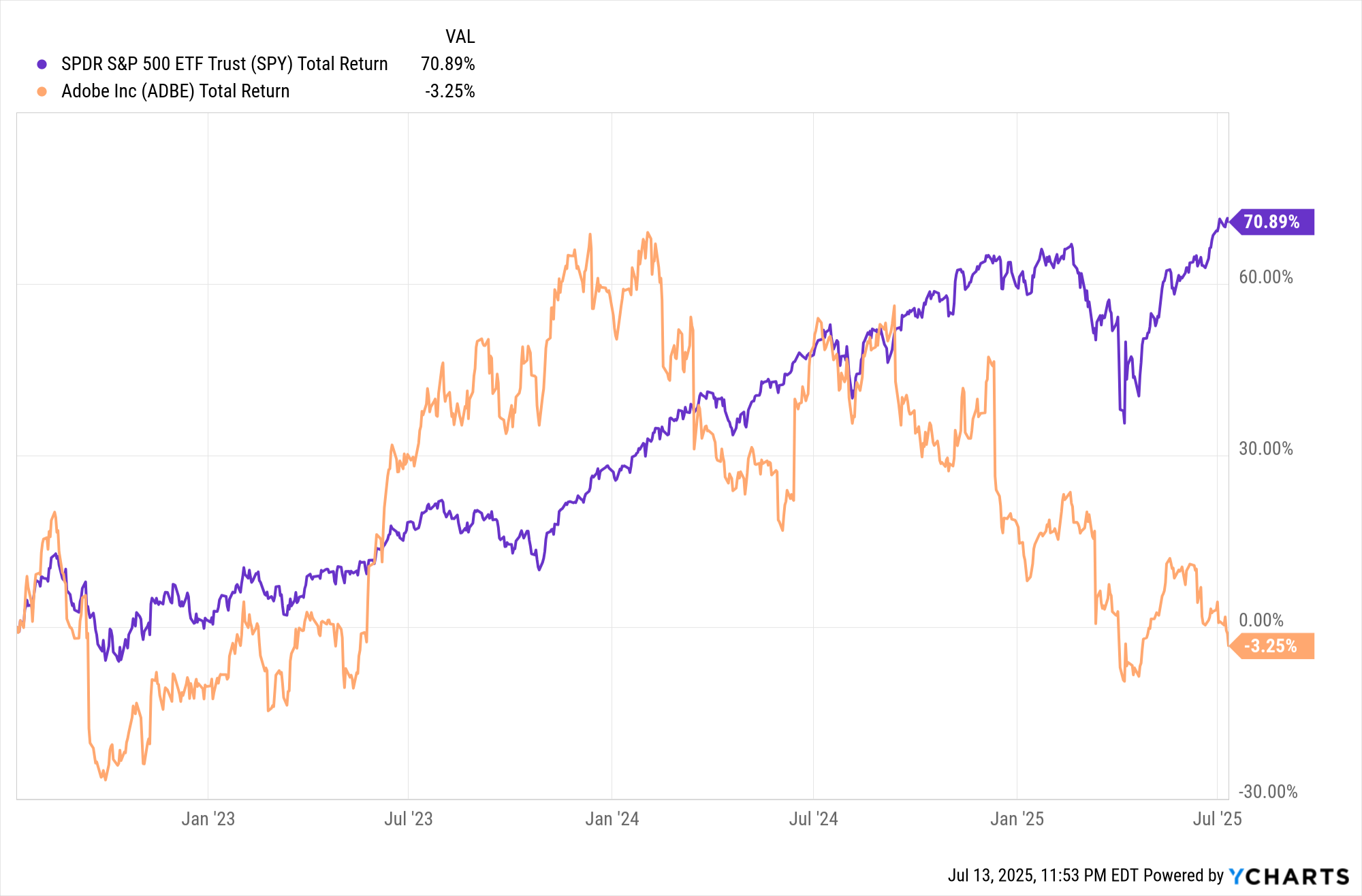

Adobe vs. S&P 500 over the last three years:

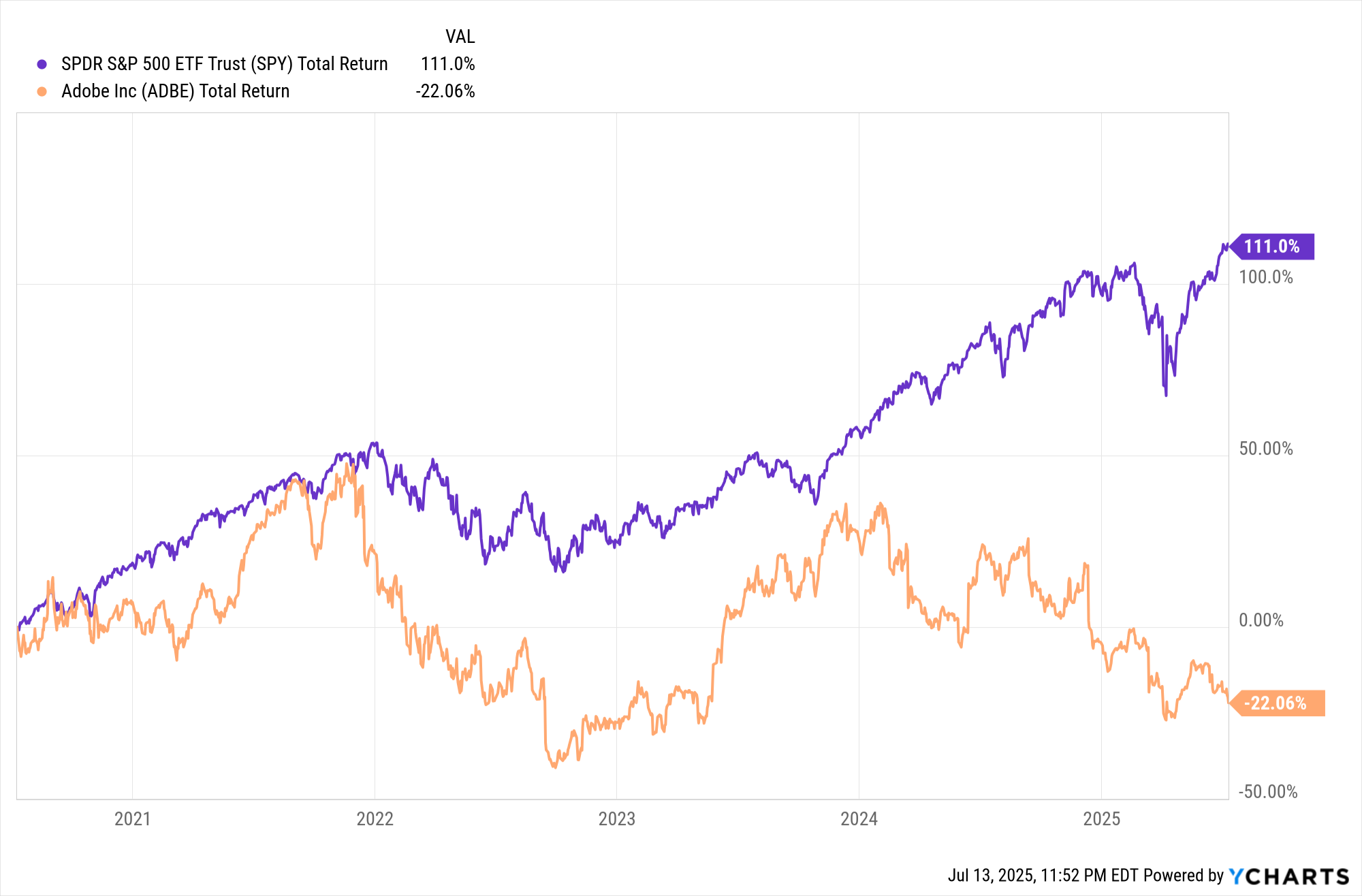

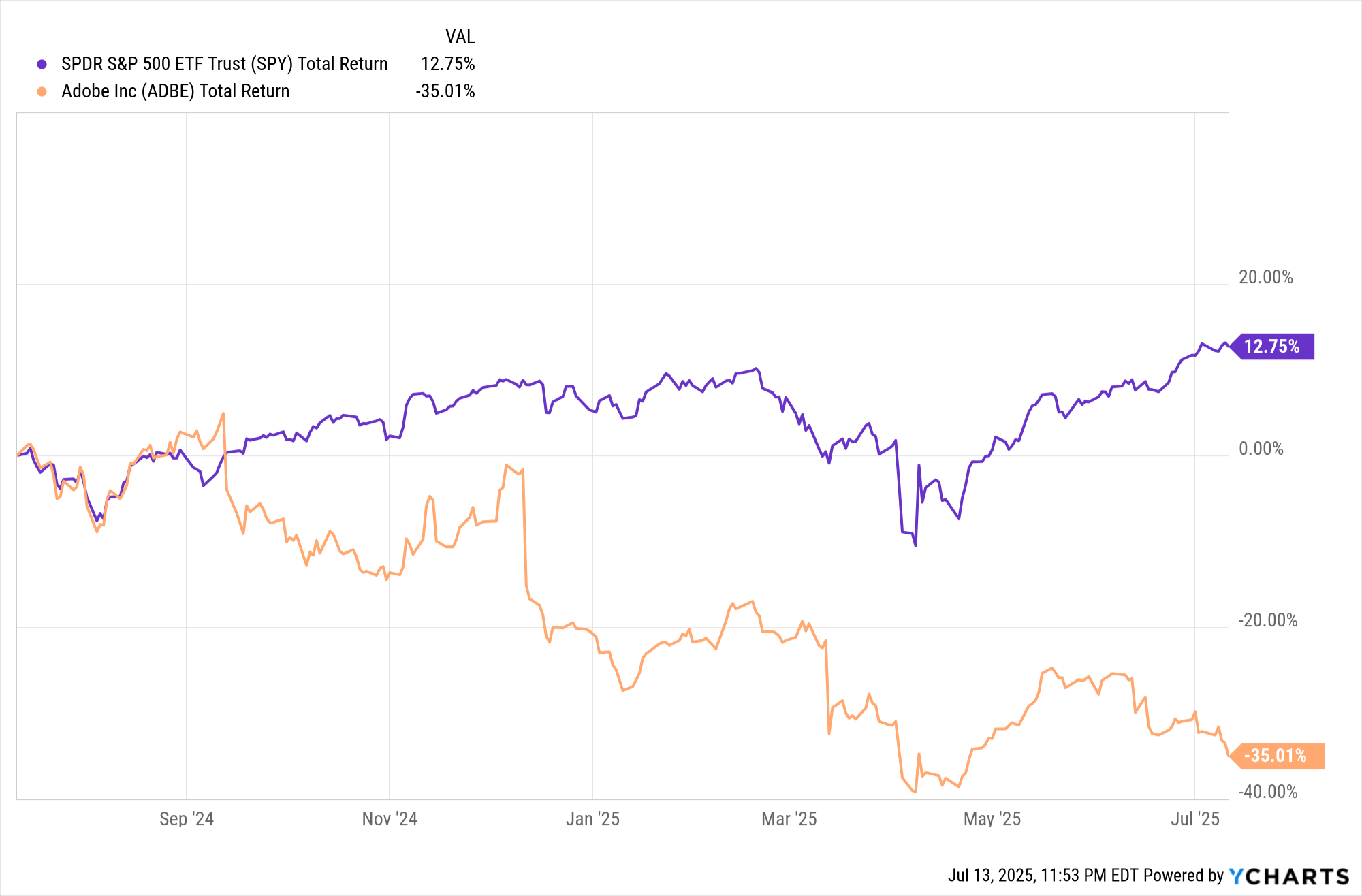

Adobe vs. S&P 500 over the last year:

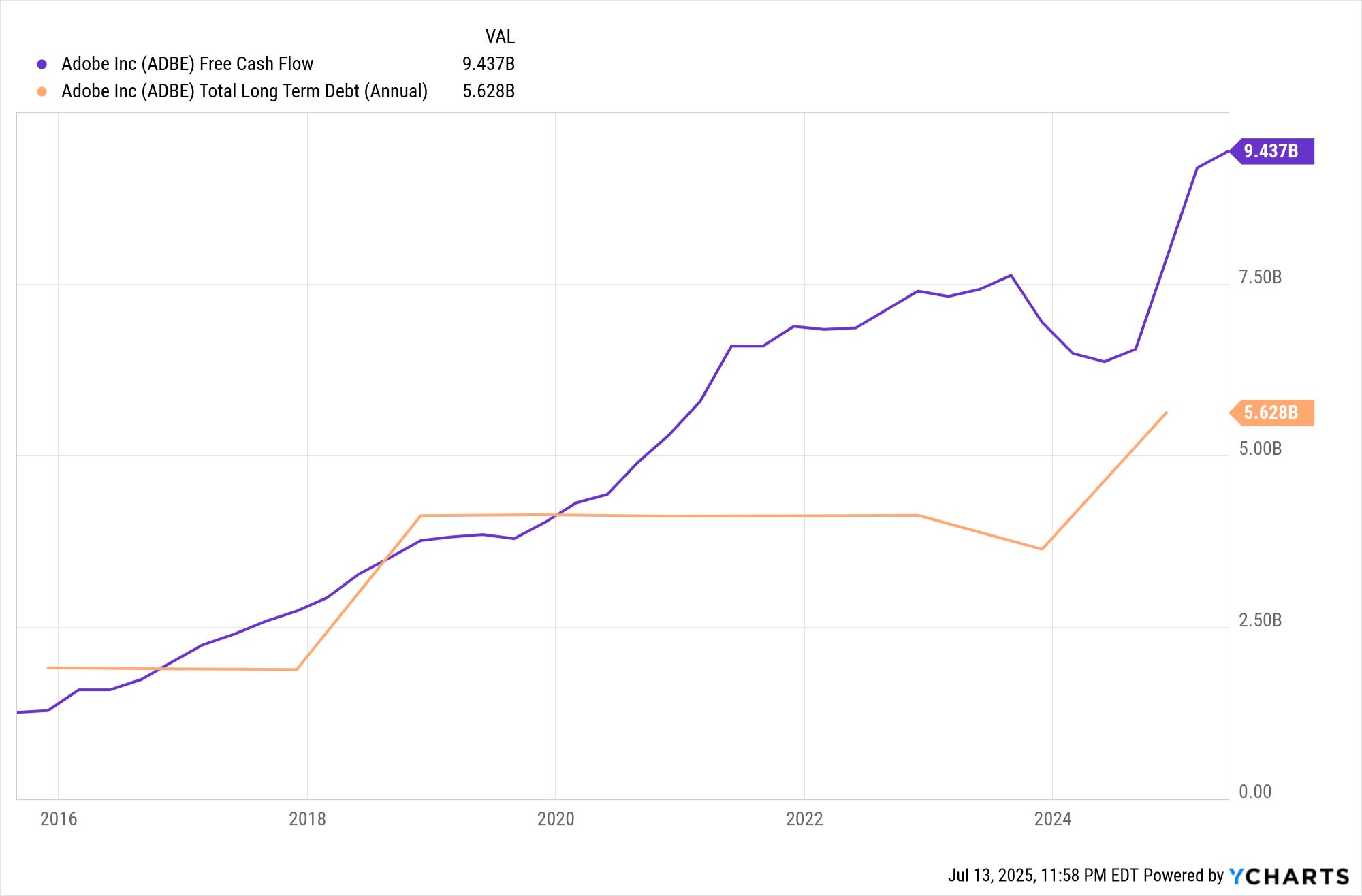

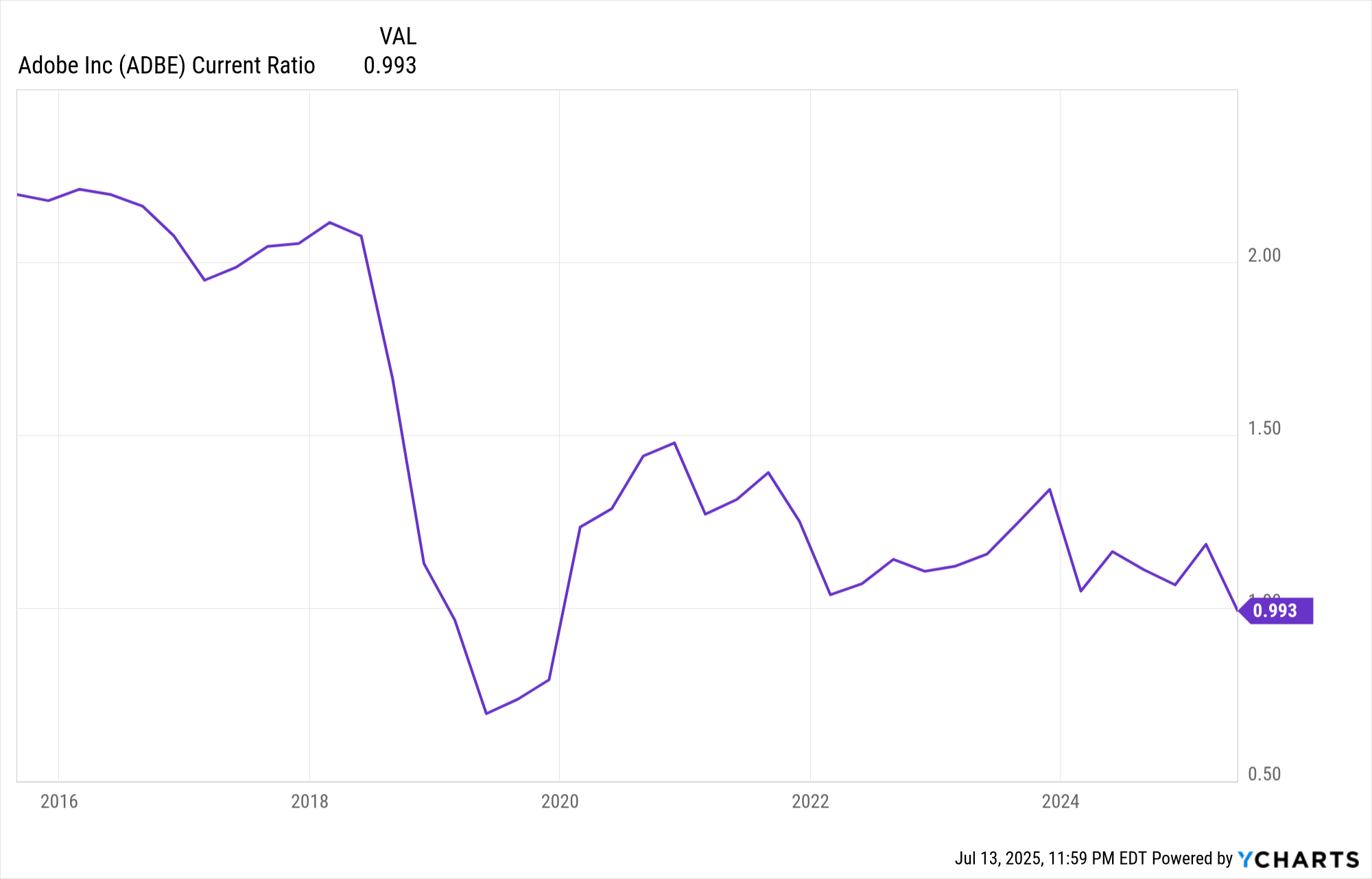

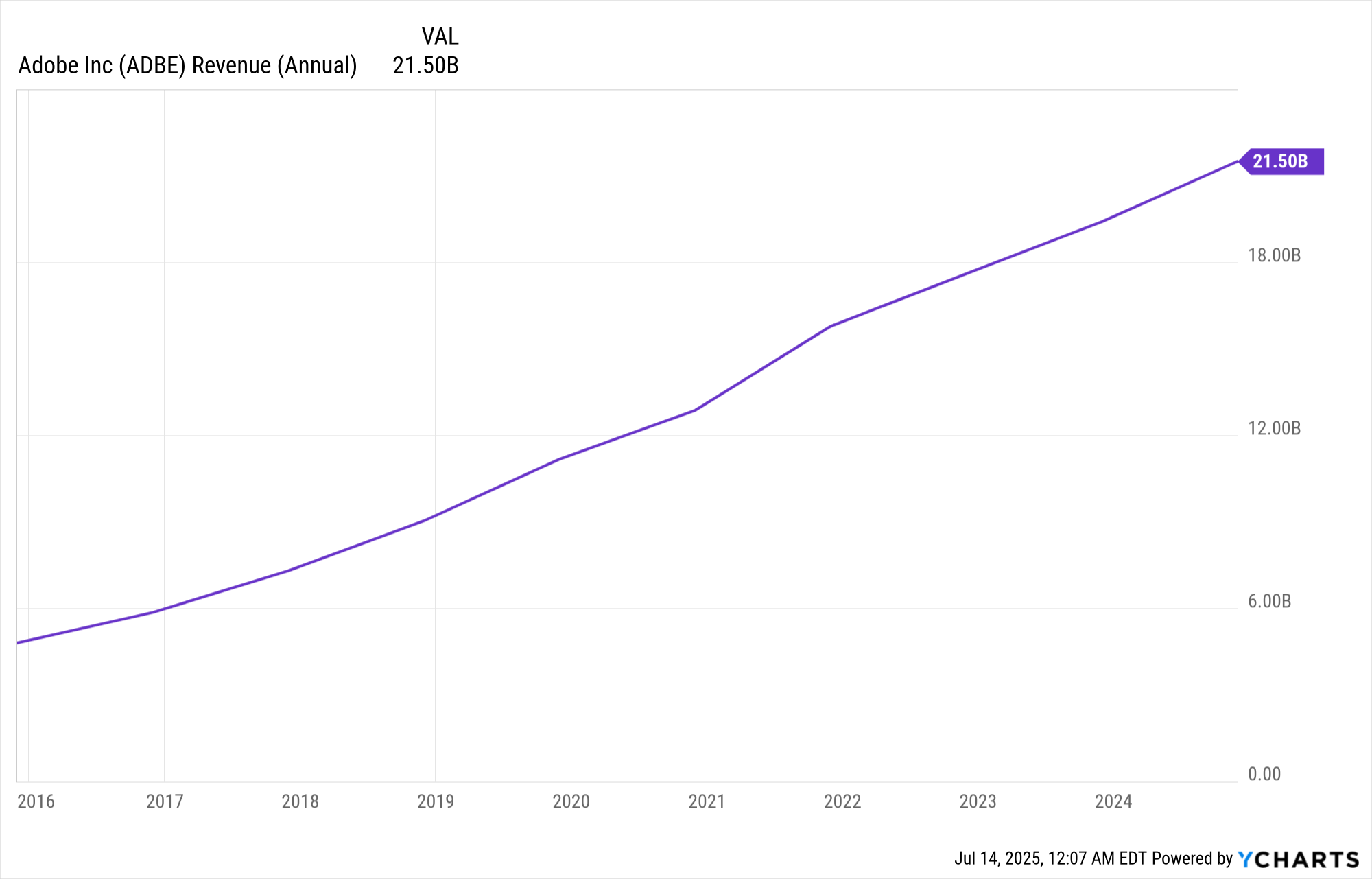

There’s a fair amount to say about what is posted above. I also want to touch on the reason I sold off Aflac and McDonald’s, in part to invest in Adobe. As I said in the beginning, in terms of Adobe’s fundamentals, there is nothing to be concerned about. Revenue continues to rise, the current ratio is 0.993 which I think safe to round up to 1, and free cash flow exceeds their long-term debt. It is pretty wild that Adobe could pay off all of its long-term debt in one year and still have a lot of money to spare. The risk of insolvency is zero. Share buybacks have been accelerating in recent years. It is great that Adobe, while still spending 18% of revenue on R&D, is returning a large amount of money to shareholders. The dollar value of Adobe’s share buybacks in 2024 amounts to 5.9% of Adobe’s current market cap, which is very impressive.

Also, you’ll notice that the market has typically awarded Adobe a very high PE in excess of 40. As of this writing, Adobe’s PE is 23. This is a perfect example of the hazard of paying a high PE for a stock. The business has been—and still is—amazing, but the stock has underperformed because a large amount of future growth was already priced into it. This is the reason for the disconnect between the financial data and the movement of the share price. The market doesn’t expect Adobe’s historical earnings growth rate to continue and thus has removed the premium Adobe used to command.

I honestly have not seen a company with financials this stellar and a sustainable competitive advantage like Adobe’s trading at a PE this low outside of a broader market crash. It’s pretty wild. This gets into why I sold off Aflac and McDonald’s in favor of Adobe and Masco. Aflac and McDonald’s both generate a nice amount of free cash flow and have a strong history of buybacks—it just isn’t to the extreme that it is with Adobe. With Adobe, free cash flow is greater than long-term debt, and nearly all of cash from operations is free cash flow. Those two lines are nearly on top of each other most of the time. The market may have gotten sour and removed the premium Adobe was commanding, lowering its PE to a level where I would take notice. But it’s not as though Adobe’s revenue has stopped growing. It’s kind of an insane opportunity, in my opinion, and McDonald’s and Aflac are two good companies that I had to kick loose to make way for Adobe and Masco.

Hamilton Helmer’s 7 Powers:

1. Scale Economies

Definition: Cost advantages that arise with increased output.

No, I don't think scale economies are a big force with Adobe.

2. Network Economies

Definition: The value of a product or service increases as more people use it.

I 100% believe there is a network economy here. It's not as clear-cut a network effect as social media companies have, but with software products, once they become the industry standard, it becomes very hard to dislodge them. If a large number of people and businesses are using Photoshop, it gets harder and harder for an individual person working in the industry to avoid it. A great example is Windows—everybody is already familiar with it, and it works well enough, so it has never been replaced, even though installing a different operating system is easy to do.

3. Counter-Positioning

Definition: A new entrant adopts a new, superior business model which the incumbent is unwilling to emulate due to self-cannibalization or organizational inertia.

Adobe is the incumbent in the industry.

4. Switching Costs

Definition: Costs (monetary or psychological) that customers incur when changing from one product to another.

I think there is some degree of switching cost. Removing Adobe products from a business may be fairly inconvenient. Retraining staff on an entirely different piece of software, as well as moving everything out of Adobe-specific file formats, isn't impossible to overcome but is a fairly significant barrier.

5. Branding

Definition: Durable emotional or reputational relationships between a company and its customers.

I think it's fair to say that Adobe has name recognition and a decent reputation with its customers.

6. Cornered Resource

Definition: Preferential access to a valuable resource that others cannot easily replicate.

Nope.

7. Process Power

Definition: Embedded company processes that are complex and time-consuming to replicate, leading to superior execution.

Nope.

There’s not much else to say. I don't see the point in repeating myself about how great I think Adobe is and how the concerns about the changes AI will bring are overblown. I haven't gone into more detail about their finances because I didn't find anything interesting—no smoking gun in the YCharts data or in the most recent 10-K. I would encourage you to review the documents I linked to yourself. Ideally, those who read this will layer their own expertise on top of mine.

Okay, bye bye now.

My Portfolio:

MAS, MITSY, META, ADBE, JPM, MGM, SPG, COF

*I think it is worth stating that just because I hold a stock doesn’t mean I think it’s a good idea to buy it right now.

*Disclaimer*

You can and will lose money in the stock market. You can lose all of your money. I can and will be wrong. I have been wrong in the past. I have lost money in the past. Investing in stocks is risky and should never be considered safe. Invest at your own risk.

Back when I was learning about generative models (VAEs and GANs) for images, I saw that Adobe was quite prominent in publishing in that space. I am sure ML is core to their workflows.

But what about their competitors, Figma, OpenAI multimodal models, etc? To be honest, I do think that in some ways the technology is there for everyone to use (eh - I write these myself), but I suppose usability and interface matter. What would it take to take away market share?

Hi David, thanks for the thoughtful writeup. I am pretty familiar with Adobe products having worked in the video games industry where it is the de-facto standard for artists. All the points you mentioned are spot on. I will add one more piece of information - usually games are on a tight schedule and they would not want to add unneeded risk of slippage. There are a whole bunch of tools and pipelines created that work with Adobe products already. My first job out of school was writing a plugin for photoshop...happy memories. Anyways, changing this out for something else that could disrupt workflows is very risky and I have never seen it happen.

Coming to the price drop and recent underperformance, given that P/E was > 100 at one point, do you think the recent underperformance is because P/E is coming back to normal levels?

Also curious to hear your thoughts on paying for ycharts or other similar tools!